- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Corporación América Airports (CAAP) Stock Looks Cheap Relative To Its Earnings

Corporación América Airports stock has returned very large gains of roughly 3.7x over the past 5 years, and the broader valuation checks currently lean cheap. This creates a tension for investors between viewing the recent share price of US$24.83 as reflecting an undervalued airport operator or as a business that has already priced in much of its progress.

- Over 5 years, Corporación América Airports has delivered a very large total return of about 367.6%, which puts recent short-term share price moves into a longer-term context.

- Future cash flow and earnings visibility from its portfolio of airport concessions can support the current valuation. At the same time, exposure to traffic volatility and capital-intensive infrastructure needs may limit how much investors are willing to pay for that growth.

- The stock currently screens as undervalued on all of Simply Wall St’s core checks, with a 6 out of 6 value score suggesting the broader metrics lean toward a discount.

The stock’s next move may depend on whether those strong multi-year returns and favorable checks still leave enough upside for new investors at today’s price.

Is Corporación América Airports Still Cheap on Earnings?

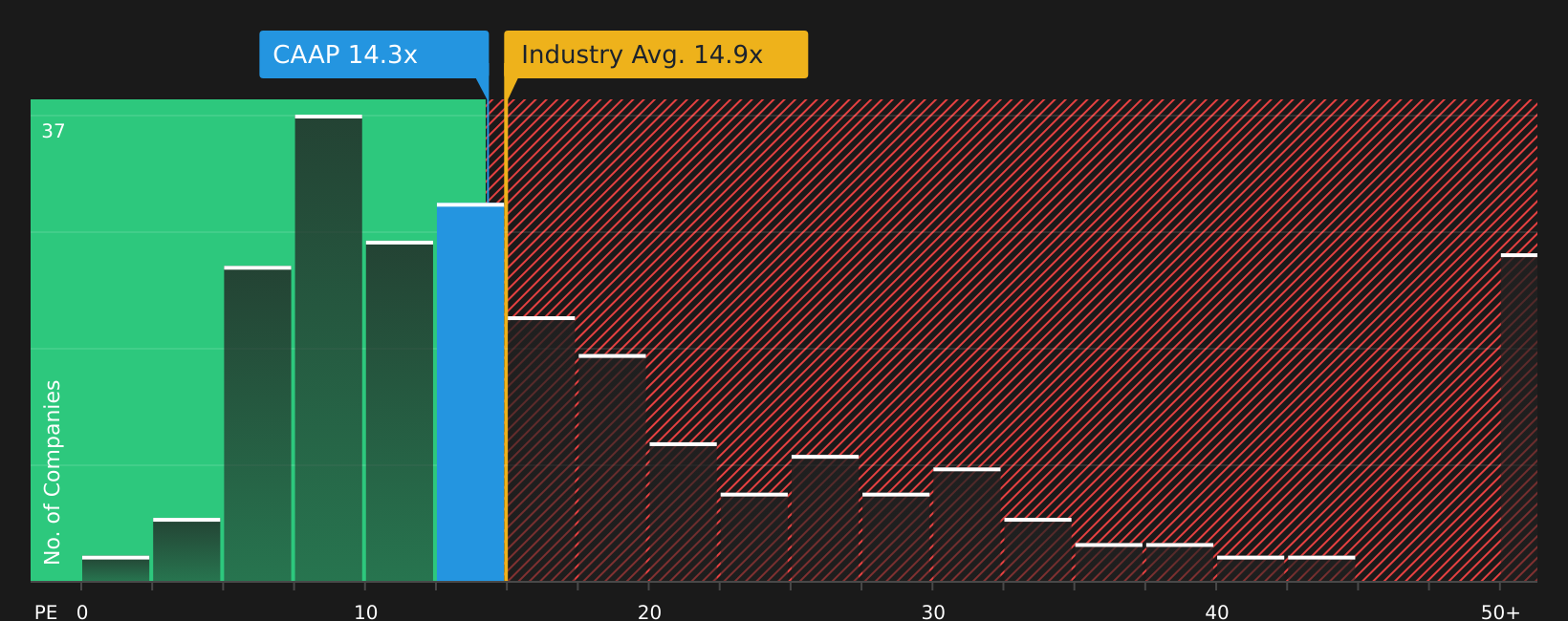

The P/E ratio is a useful cross check for Corporación América Airports because earnings are a key driver for infrastructure assets that rely on long term concessions. On this measure, the stock trades on a P/E of about 14.3x, slightly below the infrastructure industry average of roughly 14.9x and well below the broader peer group average of around 36.0x.

Simply Wall St’s fair P/E for Corporación América Airports is about 17.6x, which reflects what investors might pay when factoring in the company’s business mix, size and risk profile. Compared with the current 14.3x, the gap suggests the market is applying a discount to the company’s earnings, even before comparing it with higher peer multiples.

On the P/E multiple, Corporación América Airports stock currently appears undervalued relative to both its tailored fair ratio and the wider peer group.

See what the numbers say about this price — find out in our valuation breakdown.

The Corporación América Airports Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Corporación América Airports link the current valuation puzzle to specific assumptions about future growth, margins and earnings, so you can see what would need to happen for the stock to be worth materially more or less than today's price. Each narrative ties its figures to a clear view on how Corporación América Airports' growth, profitability and risks could evolve, providing a reference point you can revisit as new information emerges on the Community page.

Share a narrative on Corporación América Airports' stock to put your own number driven view on where its growth, margins and execution go from here, and see how that thesis holds up as new data arrives. Adding your voice can help shape the discussion in the Simply Wall St community for investors who are watching this business closely.

Do you think there's more to the story for Corporación América Airports? Head over to our Community to see what others are saying!

The Bottom Line

For Corporación América Airports, the valuation work so far points to a stock that still screens as undervalued on market multiples, even after a very strong 5 year run. The key question is whether earnings and cash generation from its airport concessions can support that discount without being knocked off course by traffic swings or heavy capital needs. For now, the crux of the debate is whether the current lower P/E simply reflects caution around those risks or whether it is mispricing a business that continues to execute against its long term concessions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com