- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Wheaton Precious Metals' (TSX:WPM) Streaming Resilience Signal Enduring Strength or Hidden Vulnerabilities?

- In recent days, analysts at Jefferies and UBS have reiterated positive ratings on Wheaton Precious Metals, citing the resilience of its precious-metals streaming model despite lower gold prices and higher diesel costs earlier this year.

- This renewed analyst confidence highlights how Wheaton’s contract-based streaming structure can help cushion profitability even when underlying mining cost pressures rise.

- With that backdrop of sustained analyst conviction in its streaming model, we’ll now assess how this news shapes Wheaton’s investment narrative.

We've uncovered the 6 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Wheaton Precious Metals Investment Narrative Recap

To be a shareholder in Wheaton Precious Metals, you need to believe in the durability of its streaming model and its leverage to long term precious metals demand, even when input costs and gold prices move against it. The recent Jefferies and UBS updates, which kept positive ratings despite lower price targets, do not materially change the core near term catalyst, which is execution on Wheaton’s growth pipeline, or the key risk of rising competition for attractive streaming deals.

The most relevant recent development against this backdrop is Wheaton’s February 2026 guidance, which outlined 2026 production of 860,000 to 940,000 gold equivalent ounces and a path to 1,200,000 GEOs by 2030. This guidance sits at the heart of the growth story analysts are underwriting when they reaffirm confidence in the streaming model, even as they acknowledge margin pressure from weaker gold prices and higher diesel costs.

Yet against that optimism, investors should be aware that competition for new streams and a shrinking pool of large, high quality opportunities could...

Read the full narrative on Wheaton Precious Metals (it's free!)

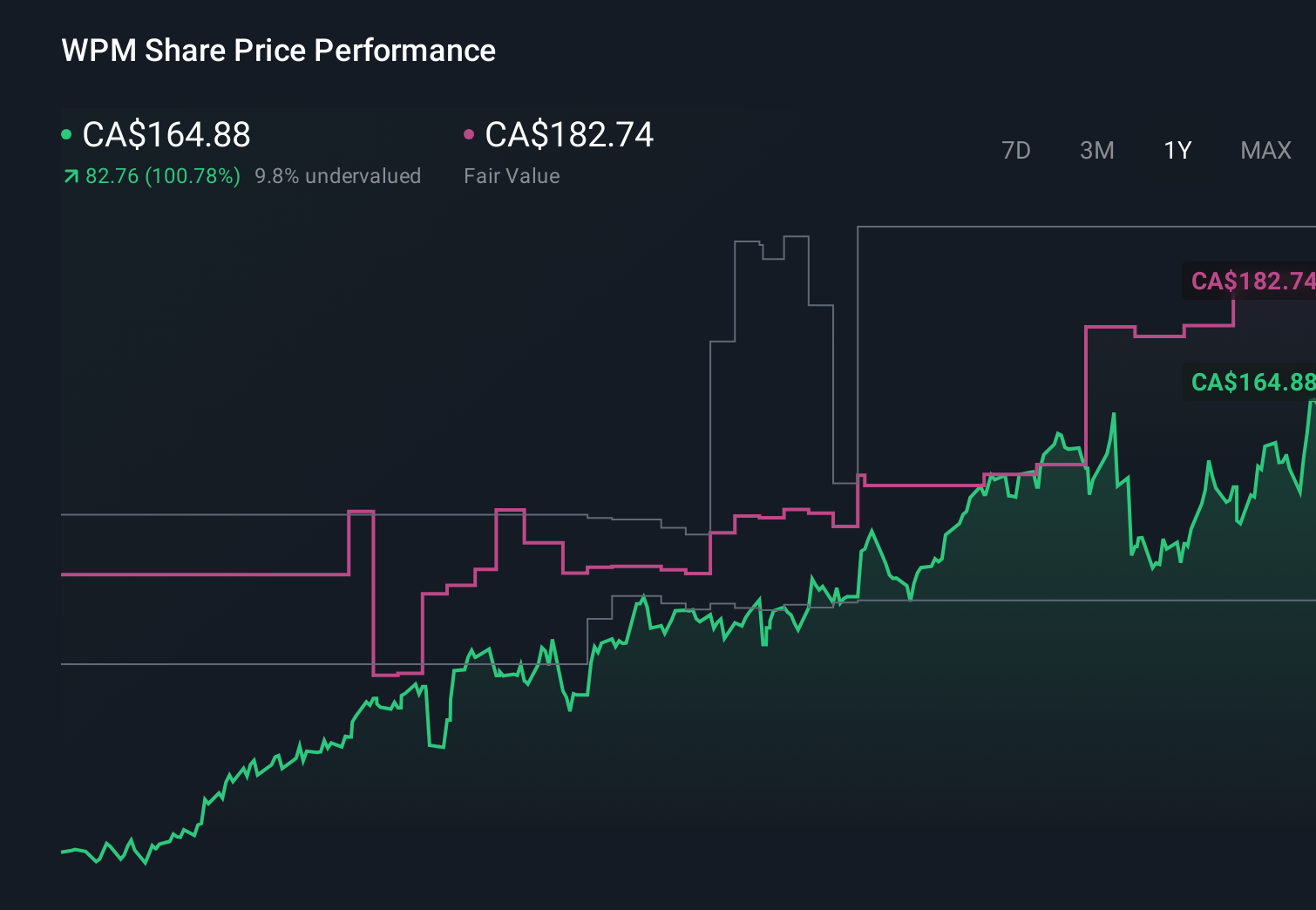

Wheaton Precious Metals' narrative projects $4.3 billion revenue and $2.4 billion earnings by 2029. This requires 15.8% yearly revenue growth and about a $0.6 billion earnings increase from $1.8 billion today.

Uncover how Wheaton Precious Metals' forecasts yield a CA$249.81 fair value, a 71% upside to its current price.

Exploring Other Perspectives

While consensus focuses on steady growth, the most optimistic analysts were penciling in around US$5.2 billion of revenue and US$3.0 billion of earnings by 2029, which is a far more aggressive story than today’s and could look very different once the latest analyst reactions to Wheaton’s streaming resilience and portfolio risks are fully reflected.

Explore 6 other fair value estimates on Wheaton Precious Metals - why the stock might be worth just CA$185.29!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Wheaton Precious Metals research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Wheaton Precious Metals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wheaton Precious Metals' overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Find 5 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com