- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Sixt (XTRA:SIX2) Cheap As Bond Demand And New Airline Tie Up Raise Value Questions?

Sixt (XTRA:SIX2) is back in focus after placing a €500 million bond that was several times oversubscribed, alongside a new partnership with American Airlines’ AAdvantage loyalty program.

See our latest analysis for Sixt.

Despite the fresh €500 million bond issue and the new AAdvantage partnership bringing Sixt back into the spotlight, the stock’s 1-month share price return is down 6.81% and the 1-year total shareholder return is down 24.55%. This suggests recent momentum has been fading.

If Sixt’s recent moves have you thinking about where else growth stories might emerge, this could be a good moment to broaden your search with the 105 top founder-led companies

Sixt’s bond demand and airline tie up point to confidence in the business, yet the share price has moved the other way. Are investors misreading the fundamentals, or is sentiment adjusting to a fairer valuation?

Price to earnings of 11x for Sixt: Is it justified?

Sixt is trading on a P/E of 11x, and at a last close of €70.45 it screens as cheaper than several benchmarks that investors may look at for context.

The P/E multiple compares the company’s share price with its earnings per share, so for Sixt this 11x figure reflects what the market is currently willing to pay for each euro of earnings. For a mobility services group with established operations across Germany, wider Europe and North America, this is a straightforward way for you to compare what the market is pricing in against other transportation stocks.

According to the data, Sixt is described as trading at good value compared to peers and the broader European Transportation industry, with the current P/E of 11x sitting below both the industry average of 14.7x and a peer average of 15.5x. It is also below an estimated fair P/E level of 15.2x that our analysis suggests the market could gravitate toward if sentiment shifted in line with those fundamentals.

In other words, the P/E of 11x implies the market is assigning a lower earnings multiple to Sixt than it does to comparable transportation companies and than the fair ratio estimate points to, which may indicate expectations that are more cautious than those benchmarks.

Explore the SWS fair ratio for Sixt

Result: Price-to-earnings of 11x (UNDERVALUED).

However, Sixt’s falling 1-year and 3-year total returns, alongside its €4,373.431m revenue tied to cyclical mobility demand, could challenge the idea that the current P/E is attractive.

Find out about the key risks to this Sixt narrative.

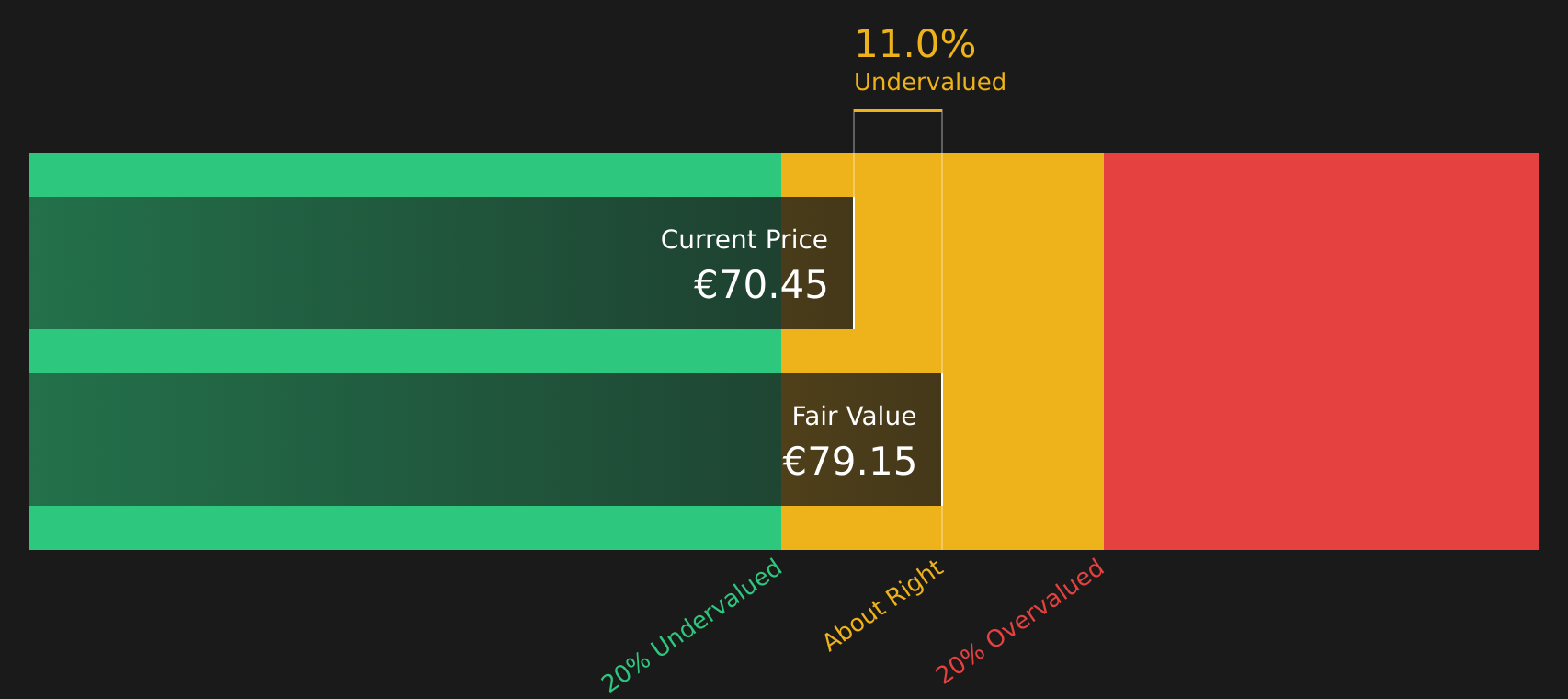

Another view on Sixt: what the DCF model says

While Sixt looks inexpensive on an 11x P/E, the SWS DCF model also points to the shares trading below an estimated future cash flow value of €79.17, with the current price at €70.45. If both earnings and cash flow signals align, is the discount really just about sentiment?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sixt for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 224 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of concerns and optimism around Sixt leaves you unsure, take a closer look at the data now and decide where you stand with the 4 key rewards and 2 important warning signs

Looking for more investment ideas beyond Sixt?

If Sixt has you thinking harder about price, quality and risk, do not stop here. Your next strong idea might be sitting in another corner of the market.

- Spot potential bargains early by focusing on quality businesses trading at appealing valuations through the 224 high quality undervalued stocks

- Prioritise resilience by zeroing in on companies with robust finances using the solid balance sheet and fundamentals stocks screener (417 results)

- Get ahead of the crowd by scanning a screener containing 509 high quality undiscovered gems before they attract wider attention

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com