- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Rogo’s Governed AI Access Deal Quietly Reshaping Snowflake’s (SNOW) Regulated‑Data Advantage?

- Earlier this week, Rogo announced it had integrated Snowflake’s managed Model Context Protocol (MCP) server, allowing AI agents to work directly on governed Snowflake data for financial institutions without that data leaving Snowflake’s existing security and governance perimeter.

- This “connect-once” MCP integration could make Snowflake more attractive to heavily regulated customers by cutting the need for bespoke pipelines when embedding AI into high‑value, sensitive datasets.

- We’ll now examine how this new governed MCP integration with Rogo may influence Snowflake’s broader AI‑driven investment narrative.

Find 49 companies with promising cash flow potential yet trading below their fair value.

Snowflake Investment Narrative Recap

To own Snowflake, you need to believe its AI Data Cloud can keep attracting large enterprises, deepen usage and eventually translate that into profitable growth despite current losses. In the near term, the key catalyst is whether AI driven workloads keep lifting product revenue growth, while the biggest risk remains execution and monetization of its expanding AI stack amid intense competition. The Rogo MCP integration reinforces Snowflake’s AI governance story but does not materially alter those core drivers just yet.

Among recent developments, the performance based stock award of up to 1,000,000 shares for CEO Sridhar Ramaswamy stands out here. It ties a large part of his compensation to ambitious multi year stock price hurdles and long term value creation, which matters if you are weighing Snowflake’s ability to invest heavily in AI offerings like MCP while still pushing toward improved margins and disciplined growth.

Yet while this paints an appealing AI growth story, investors should also be aware that...

Read the full narrative on Snowflake (it's free!)

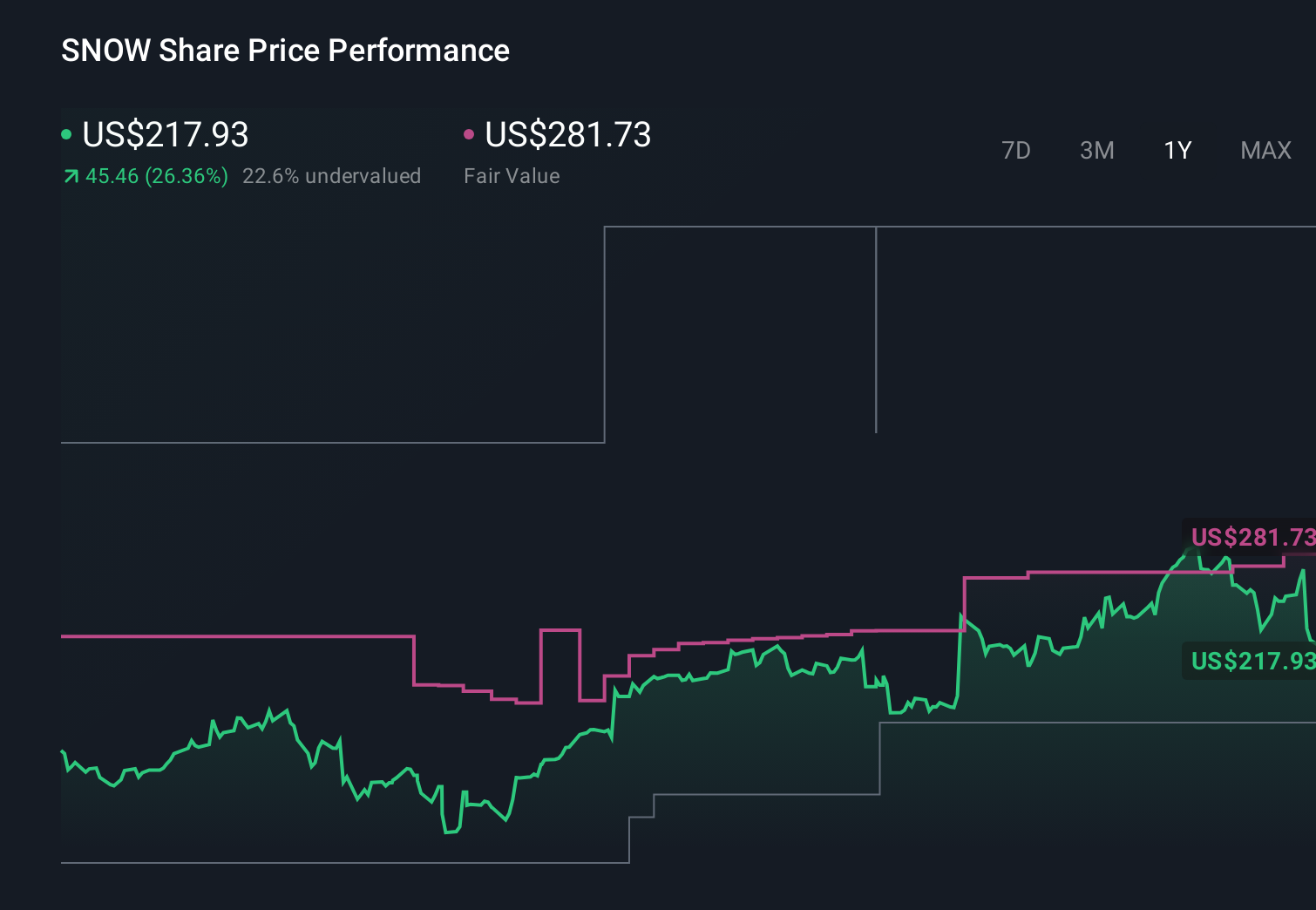

Snowflake's narrative projects $10.1 billion revenue and $792.7 million earnings by 2029. This requires 26.3% yearly revenue growth and about a $2.0 billion earnings increase from -$1.2 billion today.

Uncover how Snowflake's forecasts yield a $292.53 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Compared with consensus, the most optimistic analysts already expected Snowflake to reach about US$11.2 billion in revenue by 2029, and see partnerships like Rogo’s governed MCP use case as evidence that AI centric workloads could justify that faster path, although others worry that heavy hyperscaler dependence could still cap the upside.

Explore 12 other fair value estimates on Snowflake - why the stock might be worth as much as 48% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Snowflake research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Snowflake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Snowflake's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com