- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is B2Gold’s (TSX:BTO) ‘Undervalued’ Label Masking Deeper Margin Strains In A Softer Gold Market?

- In early July 2026, financial media coverage highlighted B2Gold Corp. as an undervalued gold producer under US$5, with RBC Capital maintaining a “Sector Perform” rating while flagging margin pressures from softer gold and silver prices and rising costs.

- At the same time, commentators pointed to continued central bank gold buying and B2Gold’s established revenue base and analyst coverage as reasons investors might reassess it against more speculative junior miners.

- Next, we’ll examine how renewed focus on B2Gold’s perceived undervaluation and central bank gold demand influences its existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

B2Gold Investment Narrative Recap

To own B2Gold, you need to be comfortable with a mid tier producer that couples meaningful exposure to gold prices with political and cost risk. The latest coverage highlighting the stock as “undervalued under US$5” does not change the near term focus on Goose Mine ramp up as the key catalyst, or on margin pressure from softer gold and silver prices and rising costs as the main immediate risk.

The recent Goose Mine fire update is the most relevant development here, because Q2 2026 production was trimmed even as full year guidance for Goose remained intact. Against renewed attention on valuation and central bank gold demand, how smoothly Goose returns to planned throughput will matter more to B2Gold’s story than short term share price moves or target changes.

Yet beneath the appeal of a low share price, investors should be aware that concentrated exposure to high risk jurisdictions means...

Read the full narrative on B2Gold (it's free!)

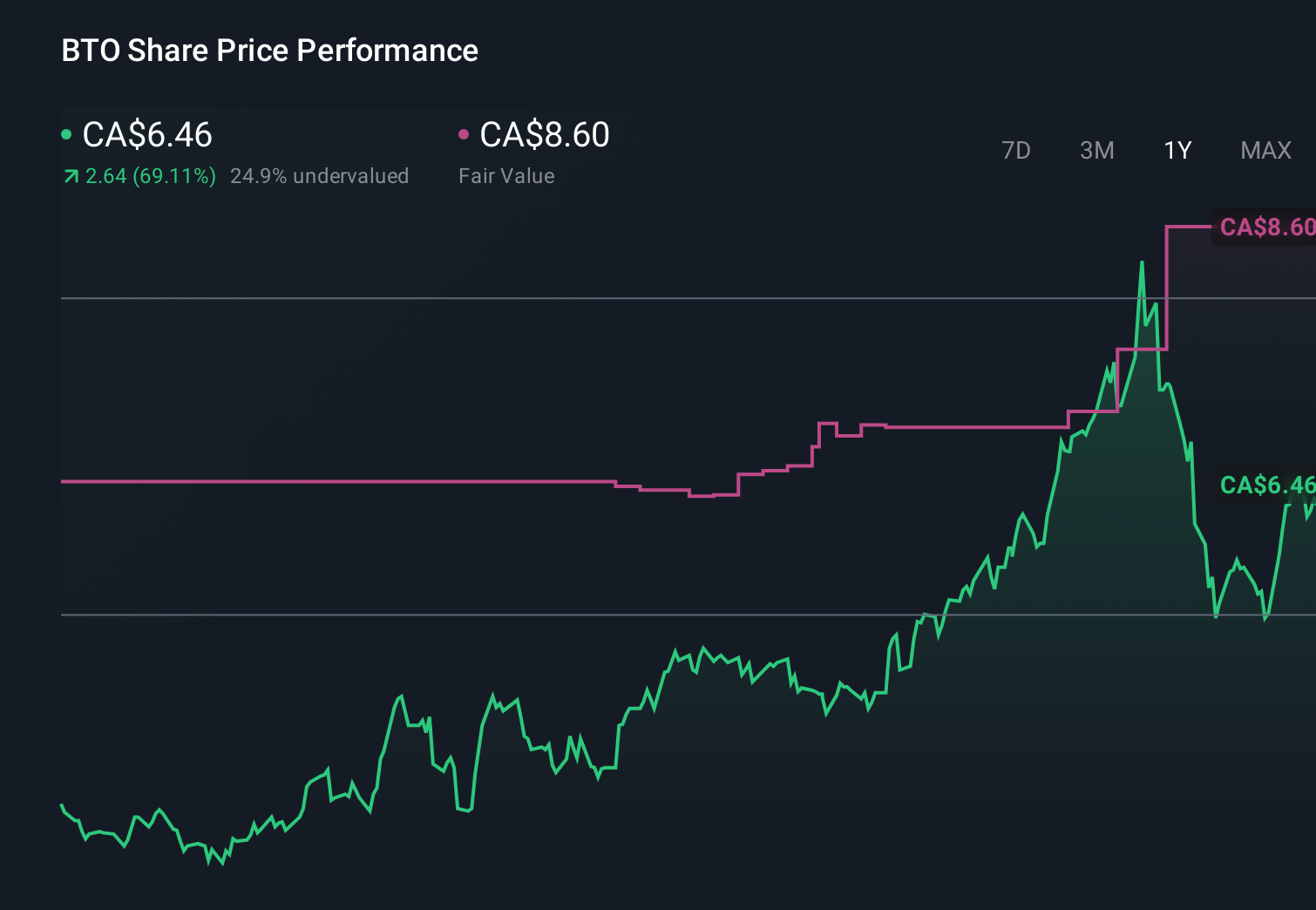

B2Gold's narrative projects $3.7 billion revenue and $1.8 billion earnings by 2028. This requires 19.2% yearly revenue growth and about a $2.2 billion earnings increase from -$433.6 million today.

Uncover how B2Gold's forecasts yield a CA$8.60 fair value, a 67% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts once saw B2Gold’s revenue reaching about US$7.7 billion and earnings near US$4.0 billion, but recent margin concerns and cost pressures show how far opinions can differ and why you should weigh that upbeat view against the risk that rising all in sustaining costs could tell a very different story.

Explore 5 other fair value estimates on B2Gold - why the stock might be worth just CA$6.85!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your B2Gold research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free B2Gold research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate B2Gold's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 10 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 29 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com