- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

IonQ (IONQ) After Raised Guidance And Backlog Growth Faces A Valuation Test

IonQ (IONQ) has grabbed attention after reporting strong revenue growth, a sharp jump in its customer backlog to about US$470 million, and lifting full year guidance to a range of US$260 million to US$270 million.

See our latest analysis for IonQ.

Despite the upbeat revenue and backlog news, IonQ's recent share price return has been weak, with the stock down 6.42% over one day, 37.39% over 30 days, and 24.95% year to date, while the 5 year total shareholder return of 252.41% still reflects strong long term gains.

If IonQ's swings have your attention, it can be useful to compare it with other quantum computing opportunities through the Simply Wall St screener for 26 quantum computing stocks

IonQ now trades at a large discount to the average analyst price target. However, the latest slide follows fresh revenue guidance and a sizeable customer backlog. Is the market fairly cautious, or has it marked the stock down too far?

Most Popular Narrative: 26.9% Undervalued

The most followed narrative on IonQ currently places fair value at $48.00 per share, compared with a last close of $35.10, which suggests a meaningful valuation gap.

The first driver is still revenue scale. IonQ is increasingly separating itself from peers through actual top-line growth. If it lands in the $260 to $270 million range this year and shows similar momentum into 2027, investors may continue to treat it as the category leader.

Want to see why this narrative treats IonQ as the premier quantum platform? The whole argument rests on aggressive revenue compounding, rich margins, and a premium future earnings multiple. Curious which financial levers do the heavy lifting in that $48.00 fair value? The full story is in the detailed narrative.

Result: Fair Value of $48.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, IonQ’s premium pricing and ongoing losses mean any setback in quantum adoption or doubts about its trapped ion roadmap could quickly challenge this view of the company as an underpriced leader.

Find out about the key risks to this IonQ narrative.

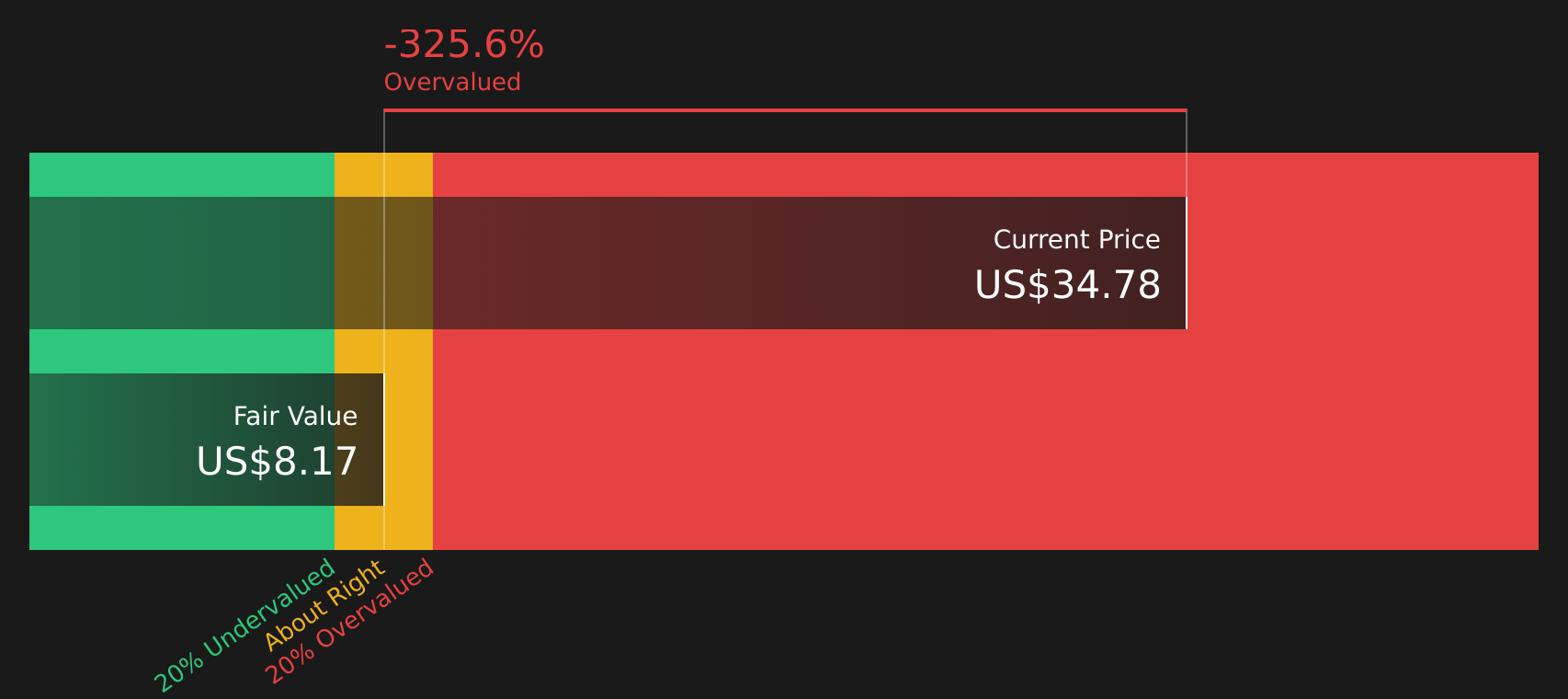

Another View: IonQ Looks Expensive On Earnings

The $48.00 fair value from the leading IonQ narrative sits uneasily next to our SWS DCF model, which places future cash flow value at just $8.12 per share, so on this view the stock looks overvalued. When two methods diverge this far, which one would you lean on?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With IonQ attracting both optimism and concern, this is a moment to move quickly, review the numbers yourself, and weigh the 2 key rewards and 4 important warning signs.

Looking for more ideas beyond IonQ?

If IonQ has sharpened your focus, do not stop here. Broaden your watchlist with other clear opportunities that could suit very different goals and risk levels.

- Target potential mispricing by scanning a focused list of companies that screen as attractively valued using our 49 high quality undervalued stocks.

- Prioritize resilience by reviewing companies that combine healthier balance sheets and fundamentals with the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for tomorrow's stories early by checking the screener containing 20 high quality undiscovered gems before they sit on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com