- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Marsh & McLennan Companies (MRSH) Following Mercer Launch And Dividend Rise Is The Stock Fully Valued

Marsh & McLennan Companies (MRSH) is in focus after its Mercer unit teamed up with American Beacon Advisors on new model portfolio solutions, alongside a 10% increase in the quarterly dividend.

See our latest analysis for Marsh & McLennan Companies.

Against this backdrop, Marsh & McLennan Companies’ recent moves in wealth and income offerings come as the stock trades at US$182.15, with a 1 month share price return of 9.22% and a 1 year total shareholder return that declined 12.04%. This suggests that short term momentum has picked up while longer term returns have been more muted.

If this kind of news driven move has you thinking about what else is out there, it could be a good moment to broaden your search with 18 top founder-led companies

After a quick 9.22% move in a month, alongside a 12.04% decline in total return over the year and a higher dividend on the table, is most of Marsh & McLennan Companies’ upside now spent, or is valuation still on your side?

Most Popular Narrative: 8.9% Undervalued

The most followed narrative currently places Marsh & McLennan Companies' fair value at $199.86 versus the recent $182.15 share price. This frames the latest dividend move and share price swing against a modest implied discount.

Strategic investments in digital transformation, advanced analytics, and AI (e.g., proprietary data tools for risk modeling, agentic interfaces) are expected to enhance operational efficiency and improve product/service offerings, enabling margin expansion and net earnings growth through improved client retention and lower cost to serve.

Want to see what sits behind that value gap estimate? The narrative focuses on measured revenue growth, firmer margins, and a richer earnings multiple than many peers.

Result: Fair Value of $199.86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the risk of weaker consulting demand and ongoing pressure on property and reinsurance pricing could still challenge the growth story of Marsh & McLennan Companies.

Find out about the key risks to this Marsh & McLennan Companies narrative.

Another View: How Marsh & McLennan Companies Looks On Earnings Multiples

The earlier narrative leans on a discounted cash flow style view that suggests Marsh & McLennan Companies is 35.6% below an estimated fair value of $282.80, which points to upside. On earnings multiples, the picture is less generous and raises different questions.

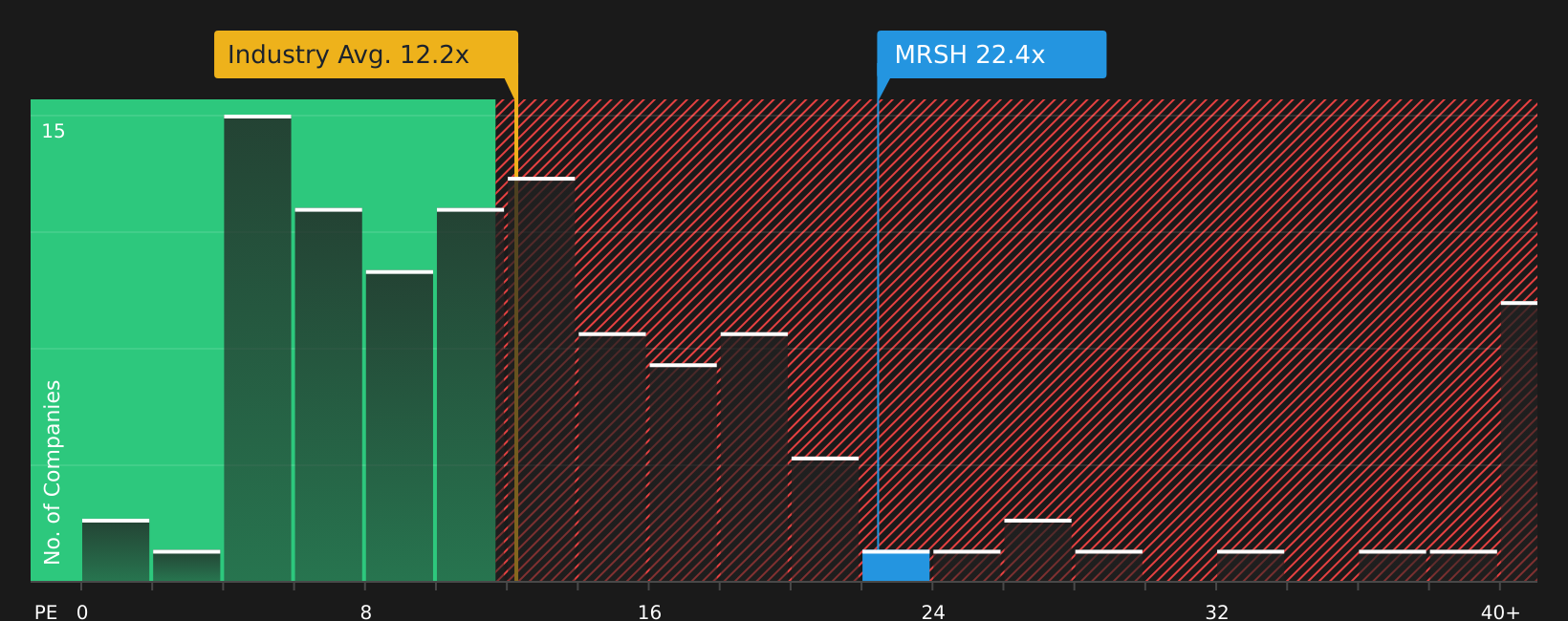

At a P/E of 22.4x, Marsh & McLennan Companies trades well above the US Insurance industry average of 12x and also above an estimated fair ratio of 13.7x, while sitting slightly below a 24.5x peer average. That mix hints at some valuation risk if the market shifts back toward industry type pricing, even if peers currently sit higher.

This kind of split between cash flow based fair value and richer earnings multiples is the sort of tension investors often need to resolve for themselves, especially after a 1 year shareholder return that declined 12.04%.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of signals around Marsh & McLennan Companies, it makes sense to look past the headlines and review the underlying data directly. To consider both the concerns and the potential upside in one place, take a closer look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Marsh & McLennan Companies?

If this Marsh & McLennan Companies update has sharpened your focus, do not stop here. The next strong idea often comes from widening the search thoughtfully.

- Spot potential value early by checking out screener containing 20 high quality undiscovered gems, where smaller companies with solid fundamentals might not yet be on everyone’s radar.

- Strengthen your defence with 81 resilient stocks with low risk scores. This screener focuses on companies that pair resilience with lower risk scores so big surprises are less likely.

- Target quality at a sensible price by reviewing 49 high quality undervalued stocks, which is built to surface stocks that combine healthy cash flows with supportive balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com