- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Upbeat PTEN Earnings Revisions and Steady Rig Activity Change The Bull Case For Patterson-UTI Energy?

- In early July, analysts reiterated generally positive views on Patterson-UTI Energy and recent data showed the company operated an average of 95 U.S. drilling rigs in June, highlighting steady activity levels.

- At the same time, upward revisions to earnings estimates and expectations for an earnings beat have supported a more constructive outlook on the business.

- With analysts increasingly optimistic about Patterson-UTI’s near-term earnings potential, we’ll examine how this shifts the company’s existing investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Patterson-UTI Energy Investment Narrative Recap

To own Patterson-UTI, you need to believe that its high-spec drilling and completion services can stay sufficiently utilized to offset recent losses and heavy capital needs. The near term catalyst is whether firm U.S. activity, reflected in June’s 95-rig average, translates into the earnings beat many analysts expect. The biggest risk is that drilling and completion softness persists, keeping margins under pressure. The latest analyst optimism does not materially change that core trade-off.

The most relevant update here is the recent upward revision in earnings estimates and expectations for an earnings beat, helped by a positive Zacks Earnings ESP and rank. That improving sentiment links directly to the June rig count and reinforces the idea that near term performance will be judged on whether rig utilization and pricing can support a turn in profitability, despite ongoing concerns about capital intensity and customer concentration.

Yet investors should also weigh how elevated capital spending and a structurally higher cost base could affect cash generation over time...

Read the full narrative on Patterson-UTI Energy (it's free!)

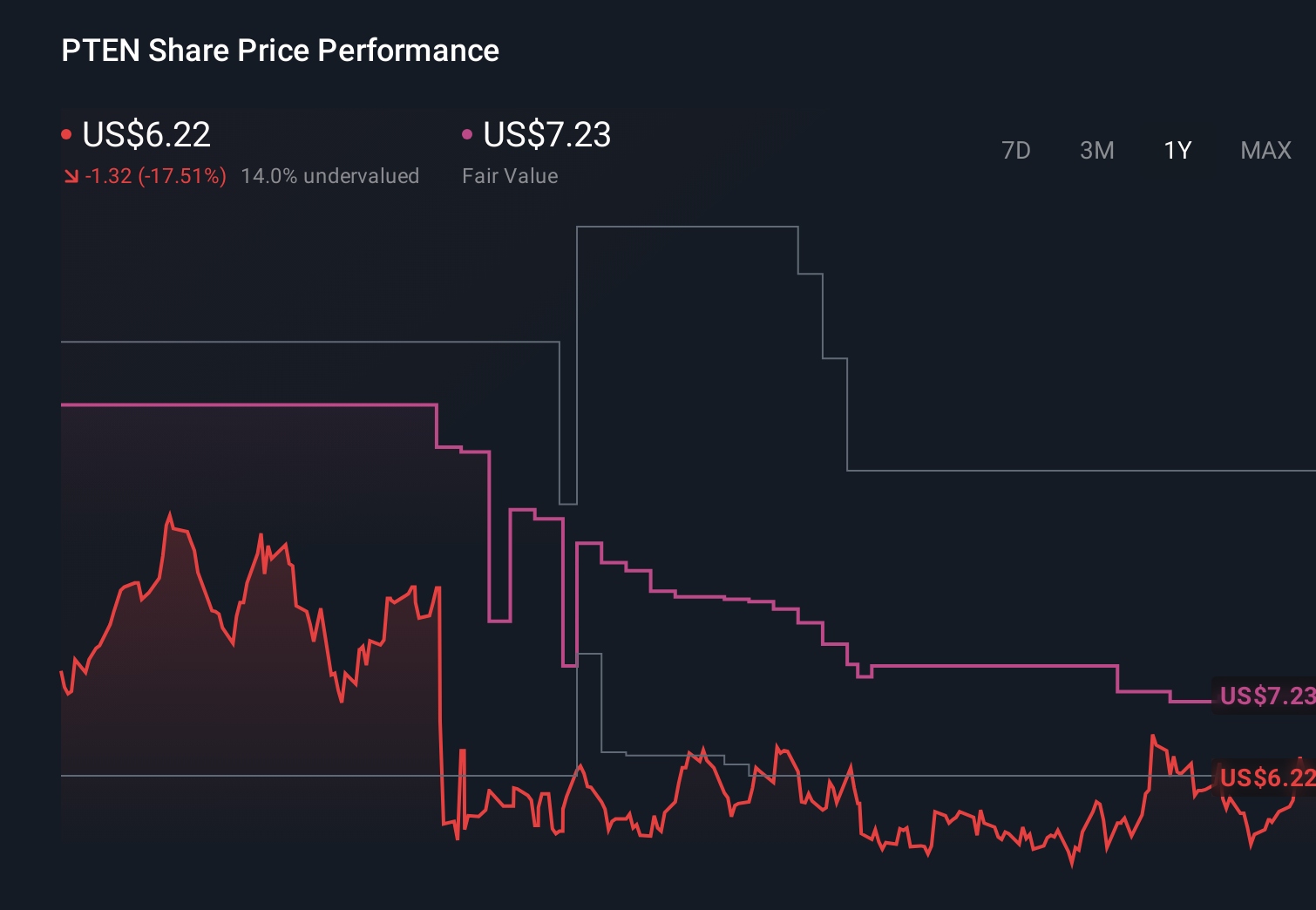

Patterson-UTI Energy's narrative projects $5.1 billion revenue and $252.2 million earnings by 2029. This requires 3.2% yearly revenue growth and a $371.5 million earnings increase from -$119.3 million today.

Uncover how Patterson-UTI Energy's forecasts yield a $13.21 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously assuming revenue of about US$5.3 billion and earnings near US$462 million, which is far more bullish than consensus and could look different once this latest earnings optimism and rig activity data are fully reflected.

Explore 3 other fair value estimates on Patterson-UTI Energy - why the stock might be worth as much as 92% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Patterson-UTI Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Patterson-UTI Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Patterson-UTI Energy's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com