- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 Undervalued Small Caps With Insider Action Across Global Markets

In the last week, the United States market has stayed flat, yet it is up 19% over the past year with earnings forecasted to grow by 18% annually. In this context of steady growth and future potential, identifying small-cap stocks that are perceived as undervalued can offer intriguing opportunities for investors seeking to capitalize on insider actions across global markets.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 10.2x | 0.8x | 48.69% | ★★★★★★ |

| Industrial Logistics Properties Trust | NA | 1.3x | 37.85% | ★★★★★☆ |

| Kingstone Companies | 9.2x | 1.3x | 36.92% | ★★★★☆☆ |

| Peoples Bancorp | 12.7x | 3.3x | 37.50% | ★★★★☆☆ |

| Onterris | 178.1x | 1.0x | 24.11% | ★★★★☆☆ |

| Bank of Marin Bancorp | NA | 13.3x | 25.30% | ★★★☆☆☆ |

| Bank of the James Financial Group | 11.1x | 2.4x | 13.94% | ★★★☆☆☆ |

| Similarweb | NA | 2.1x | 17.57% | ★★★☆☆☆ |

| Modiv Industrial | NA | 4.1x | 45.37% | ★★★☆☆☆ |

| Angel Studios | NA | 2.0x | 9.12% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

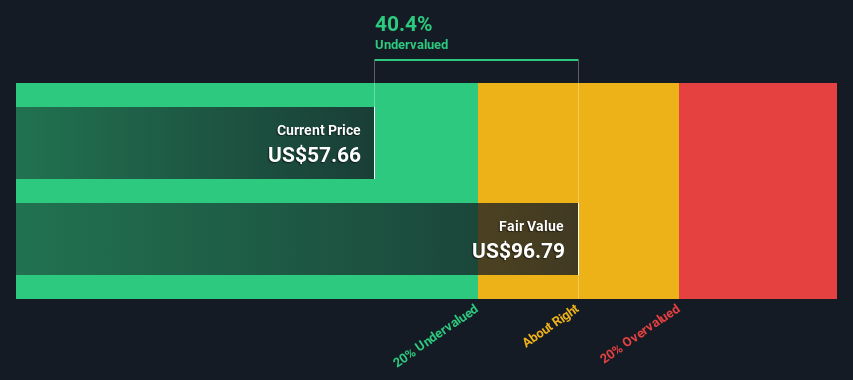

Citizens Financial Services (CZFS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Citizens Financial Services operates as a community banking institution with a focus on providing financial services, and it has a market capitalization of $0.25 billion.

Operations: Community Banking is the primary revenue stream, generating $113.47 million. The gross profit margin consistently stands at 100%, while operating expenses reached $62.50 million in the latest period, with general and administrative expenses accounting for $50.21 million of that total. The net income margin has seen fluctuations, most recently recorded at 34.66%.

PE: 9.1x

Citizens Financial Services, a smaller company in the U.S., recently experienced a drop from the Russell 2000 Dynamic Index as of June 27, 2026. Despite this, they reported strong first-quarter earnings with net interest income rising to US$26.11 million and net income reaching US$10.38 million, indicating potential for growth. Insider confidence is evident with recent share purchases by executives over several months. The company also increased its quarterly dividend to US$0.51 per share in June 2026, suggesting stable cash flow and shareholder commitment amidst industry challenges like low bad loan allowances at 61%.

SNDL (SNDL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: SNDL is a diversified company focused on liquor retail, cannabis retail, and cannabis operations with a market capitalization of CA$1.24 billion.

Operations: SNDL generates revenue primarily from liquor retail, cannabis retail, and cannabis operations. As of the latest data, the gross profit margin stands at 27.18%. The company has experienced fluctuations in its net income margin over time, with a recent figure of -1.17%. Operating expenses include significant allocations to general and administrative costs as well as depreciation and amortization expenses.

PE: -43.0x

SNDL, a smaller player in its industry, recently reported first-quarter sales of CAD 195.91 million, slightly down from the previous year. However, net losses narrowed to CAD 9.91 million from CAD 14.71 million previously. Insider confidence is evident as J. Mills acquired 50,000 shares for US$69,700 between January and March 2026, reflecting significant belief in the company's potential despite current unprofitability and reliance on external borrowing for funding. The company also repurchased over four million shares during this period for CAD 6.95 million under its buyback initiative announced last November.

- Unlock comprehensive insights into our analysis of SNDL stock in this valuation report.

Understand SNDL's track record by examining our Past report.

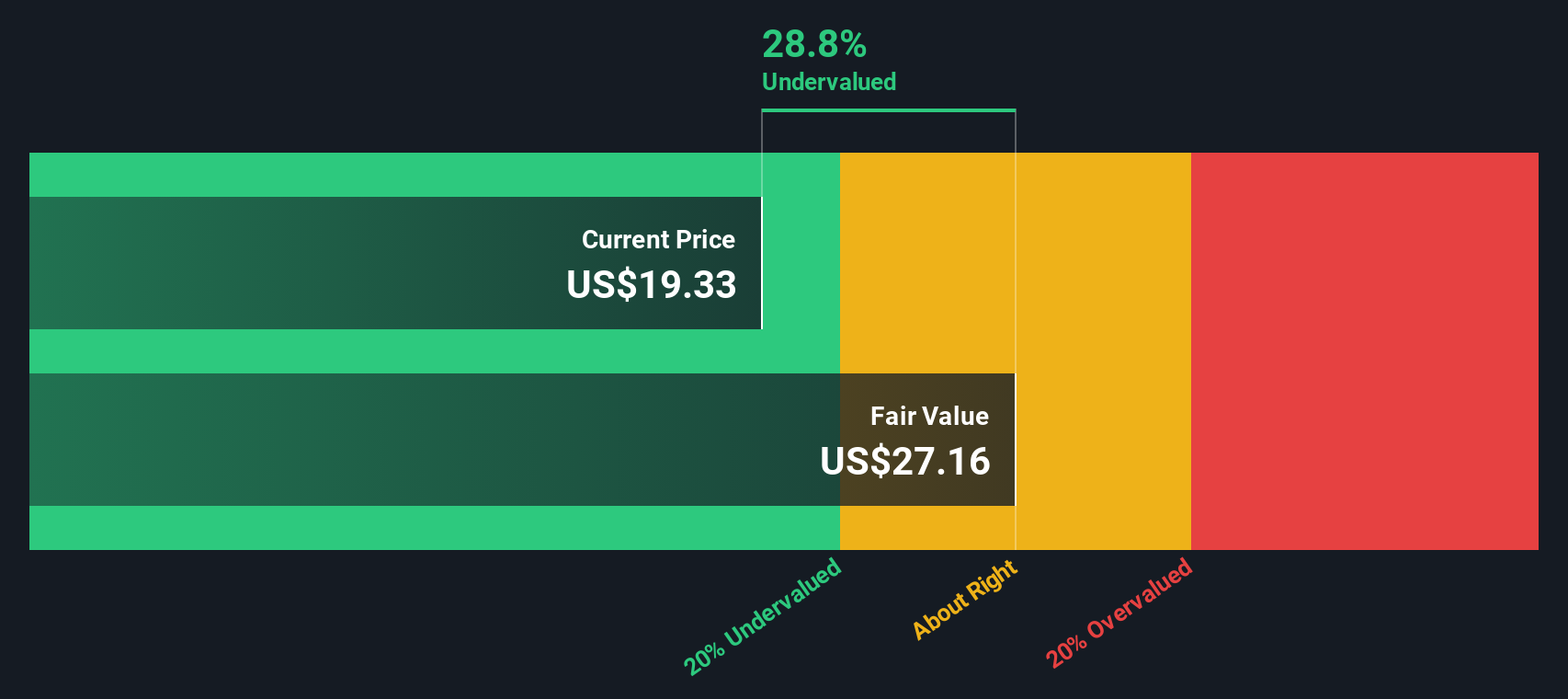

Caledonia Mining (CMCL)

Simply Wall St Value Rating: ★★★★★★

Overview: Caledonia Mining is a mining company primarily engaged in the exploration and production of gold, with a market capitalization of approximately $0.14 billion.

Operations: Caledonia Mining's revenue primarily comes from its operations, with a notable increase in revenue over the observed periods. The company's cost of goods sold (COGS) and operating expenses are significant, impacting net income. Notably, the gross profit margin reached 60.47% by March 2026, indicating a strong ability to manage production costs relative to sales.

PE: 5.4x

Caledonia Mining, a small company in the gold mining sector, has shown potential through its exploration activities at the Motapa property. The recent drilling results indicate promising gold mineralisation that could enhance production at Bilboes. Insider confidence is evident as their Chairman purchased 15,000 shares in July 2026 for US$372,150, reflecting belief in growth prospects. Despite a dip in Q1 2026 production to 14,767 ounces from previous levels, earnings improved significantly with net income rising to US$15.85 million from US$8.92 million year-on-year.

- Navigate through the intricacies of Caledonia Mining with our comprehensive valuation report here.

Explore historical data to track Caledonia Mining's performance over time in our Past section.

Key Takeaways

- Discover the full array of 60 Undervalued US Small Caps With Insider Buying right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com