- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

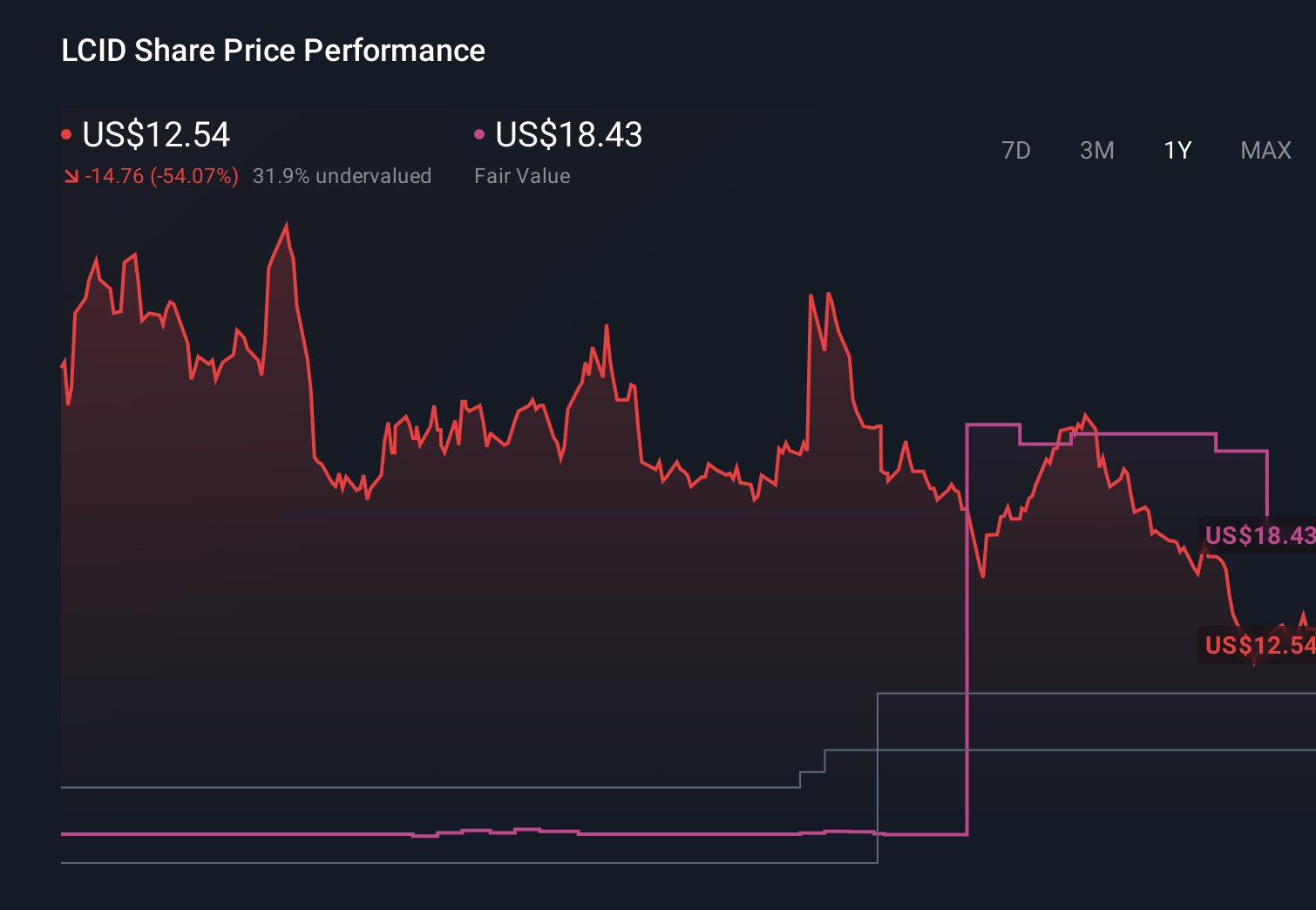

Does Lucid (LCID) Management’s Bankruptcy Denial Clarify Its Real Operational and Liquidity Challenges?

- In recent days, Lucid Group has forcefully denied media reports that it was preparing for bankruptcy or a take‑private deal, stressing that adviser AlixPartners is focused on improving operations rather than planning a court‑supervised restructuring.

- The controversy has thrown a spotlight on Lucid’s liquidity runway, restructuring efforts, and legal challenges around past disclosure of delivery disruptions, giving investors fresh information about the company’s operational and financial pressures.

- With management’s emphatic rejection of bankruptcy rumors now on record, we’ll examine how this affects Lucid’s investment narrative and risk profile.

Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Lucid Group Investment Narrative Recap

To own Lucid today, you have to believe it can turn cutting edge EV technology and the Uber robotaxi partnership into a financially sustainable business before its liquidity cushion runs thin. The recent bankruptcy rumors, and Lucid’s forceful denial, put even more attention on the upcoming Q2 2026 earnings call as the key near term catalyst, while reinforcing that funding needs and dilution risk remain the dominant overhang for shareholders.

Against this backdrop, Lucid’s June 2026 plan to cut about 18% of its U.S. workforce and eliminate a second shift at AMP-1 stands out. That move aims to align production with demand and trim roughly US$158 million in annual operating expenses, which ties directly into the liquidity concerns raised by the rumors and will be closely watched alongside any updates on the Uber robotaxi rollout.

Yet beneath the technology story, investors should be aware that concerns around cash burn and future capital raises could...

Read the full narrative on Lucid Group (it's free!)

Lucid Group's narrative projects $7.2 billion revenue and $167.8 million earnings by 2029.

Uncover how Lucid Group's forecasts yield a $8.40 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were previously banking on Lucid lifting revenue toward about US$10.9 billion by 2029, but the latest bankruptcy headlines and liquidity questions could force a rethink of those assumptions and highlight just how far apart investor views on cash burn and future funding needs really are.

Explore 5 other fair value estimates on Lucid Group - why the stock might be worth 23% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com