- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Global Growth Leaders With High Insider Ownership

As global markets navigate the complexities of Middle East tensions and energy market volatility, growth stocks have notably outpaced their value counterparts, with sectors like information technology leading the charge. In this environment, companies with high insider ownership often stand out as they may signal strong confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Shanghai Biren Technology (SEHK:6082) | 11% | 116.9% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| KebNi (OM:KEBNI B) | 11.8% | 90.9% |

| HUMAN MADE (TSE:456A) | 23.9% | 23.4% |

| CD Projekt (WSE:CDR) | 35.2% | 29.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Here we highlight a subset of our preferred stocks from the screener.

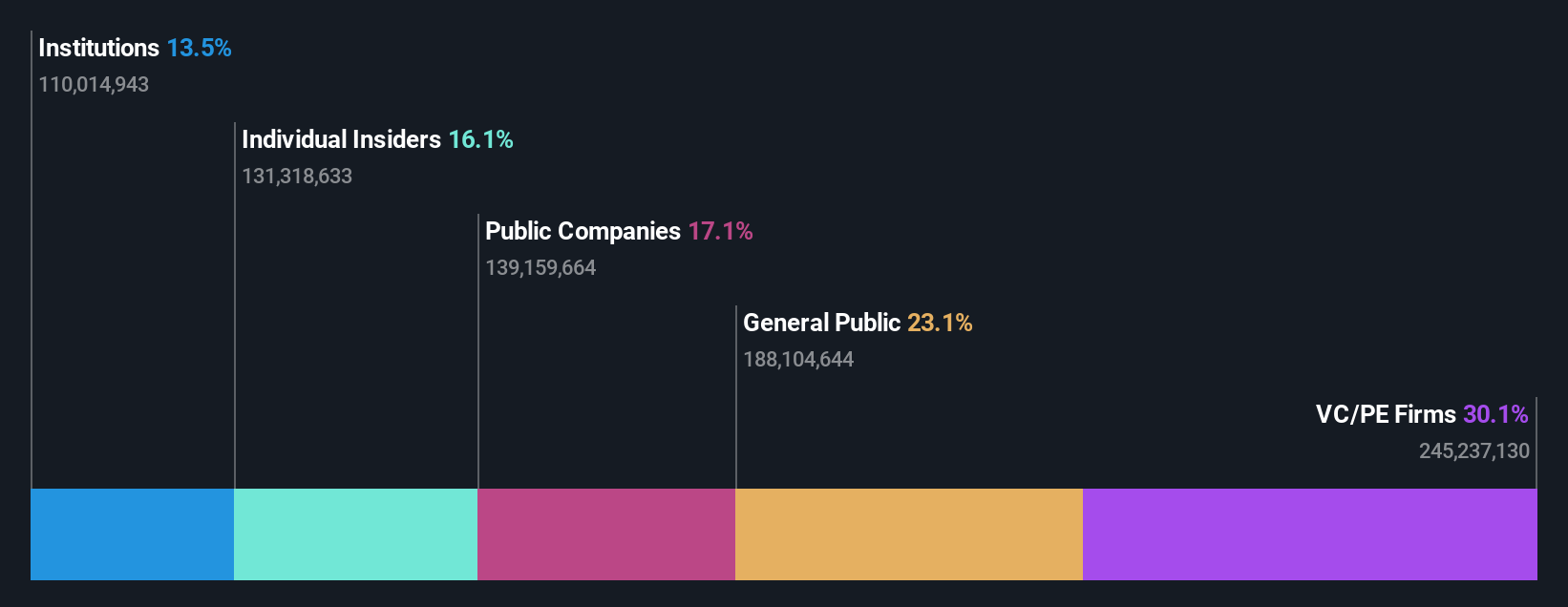

Ocumension Therapeutics (SEHK:1477)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ocumension Therapeutics, along with its subsidiaries, focuses on the research, discovery, development, and commercialization of ophthalmic therapies in China with a market cap of HK$5.07 billion.

Operations: The company's revenue from discovering, developing, and commercializing ophthalmic therapies amounted to CN¥804.35 million.

Insider Ownership: 16.5%

Earnings Growth Forecast: 94.6% p.a.

Ocumension Therapeutics, with significant insider ownership, is positioned for growth as its revenue is expected to increase by 26% annually, outpacing the Hong Kong market. The company recently received approval in China for OT-502, a pioneering single-dose intraocular steroid. Despite executive changes, including the resignation of CFO Tim Ruan and appointment of Beibei Zhuang as an independent director, Ocumension's strategic focus on innovative ophthalmic treatments supports its robust earnings growth forecast of 94.61% per year.

- Unlock comprehensive insights into our analysis of Ocumension Therapeutics stock in this growth report.

- Upon reviewing our latest valuation report, Ocumension Therapeutics' share price might be too pessimistic.

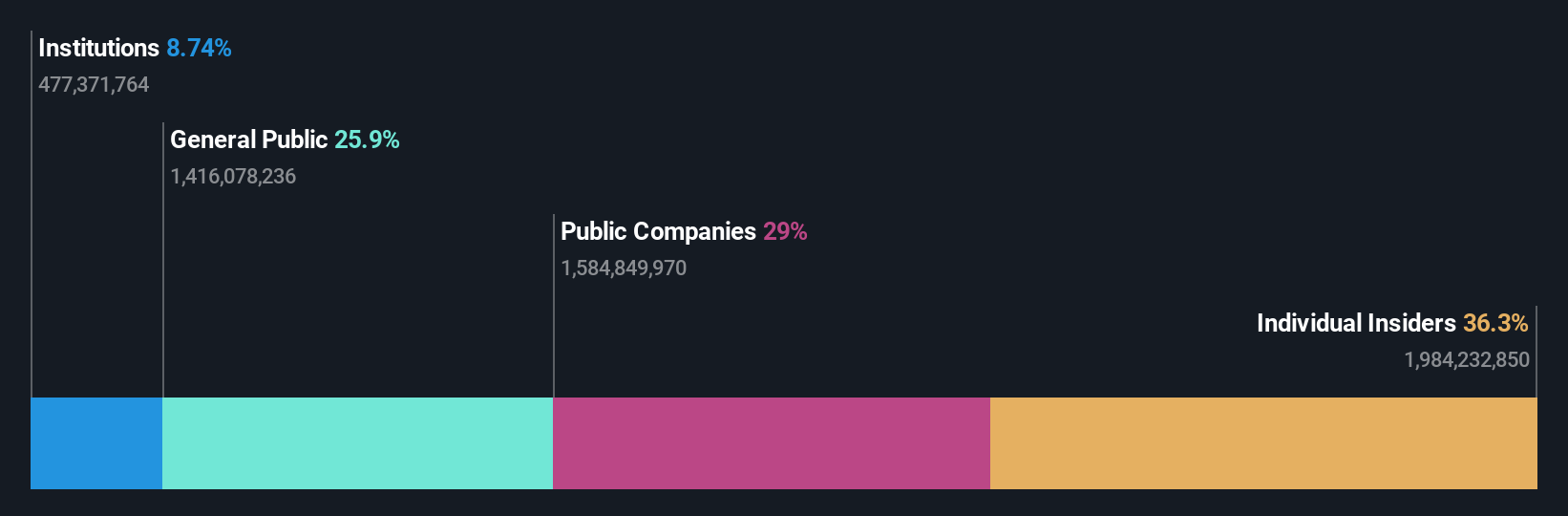

West China Cement (SEHK:2233)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: West China Cement Limited is an investment holding company that manufactures and sells cement and cement products in the People's Republic of China, Mozambique, Ethiopia, the Democratic Republic of Congo, other African countries, and internationally with a market cap of HK$9.34 billion.

Operations: The company's revenue is primarily derived from its operations in the People's Republic of China, contributing CN¥5.07 billion, and its overseas markets, which add CN¥4.70 billion.

Insider Ownership: 36.3%

Earnings Growth Forecast: 20.5% p.a.

West China Cement shows potential for growth with earnings expected to increase by 20.52% annually, surpassing the Hong Kong market's average. Despite trading at a significant discount to its estimated fair value, the company's debt coverage by operating cash flow remains a concern. Recent approval of a final dividend of RMB 0.048 per share reflects shareholder confidence but highlights sustainability issues due to limited free cash flow coverage. Insider trading activity has been minimal recently.

- Click here to discover the nuances of West China Cement with our detailed analytical future growth report.

- Our valuation report here indicates West China Cement may be undervalued.

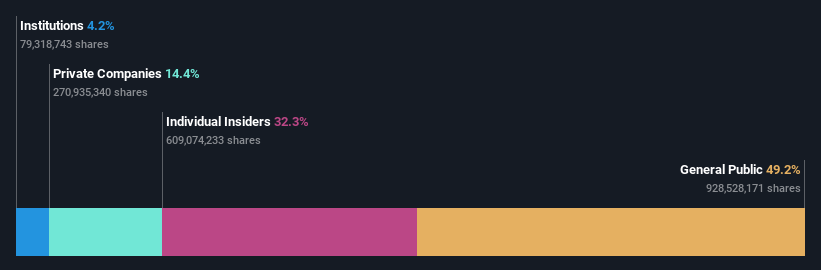

Keda Industrial Group (SHSE:600499)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Keda Industrial Group Co., Ltd. is a Chinese company engaged in the manufacturing and sale of ceramic machinery and building materials, with a market cap of CN¥28.23 billion.

Operations: Keda Industrial Group generates revenue primarily from its ceramic machinery and building materials segments.

Insider Ownership: 35.9%

Earnings Growth Forecast: 27.2% p.a.

Keda Industrial Group's earnings are projected to grow significantly at 27.2% annually, outpacing the CN market. Despite a slower revenue growth forecast of 9.2% per year, its price-to-earnings ratio of 18.5x suggests good value relative to peers and the industry average of 41.5x. Recent quarterly results showed robust performance with sales reaching CNY 4,726.62 million, up from CNY 3,766.9 million last year, indicating strong financial health despite an unstable dividend history.

- Delve into the full analysis future growth report here for a deeper understanding of Keda Industrial Group.

- According our valuation report, there's an indication that Keda Industrial Group's share price might be on the cheaper side.

Make It Happen

- Navigate through the entire inventory of 701 Fast Growing Global Companies With High Insider Ownership here.

- Interested In Other Possibilities? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com