- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Seagate (STX) Stock Still Looks Undervalued Despite Its Huge 3 Year Run

Seagate Technology Holdings has delivered a very large 3 year return while the current checks suggest the stock screens as undervalued on both intrinsic value estimates and market multiples. This sets up a clear question about how much of the story is already in the price.

- Over the past 3 years, Seagate has returned about 12.5x, which puts recent volatility in context as a move after an exceptional run.

- Expectations around high capacity storage demand tied to AI and cloud spending can support the current valuation, while concerns about capital spending cycles and execution on newer recording technologies may limit how much investors are willing to pay.

- The company scores 3 out of 6 on our valuation checks, which points to a mixed picture rather than a clear bargain or clear overvaluation even though both the Discounted Cash Flow (DCF) and multiples screens point to undervaluation.

The issue now is whether Seagate's share price already reflects these expectations or still sits at a discount to a reasonable intrinsic value estimate.

Does Seagate Technology Holdings Look Undervalued on Cash Flow?

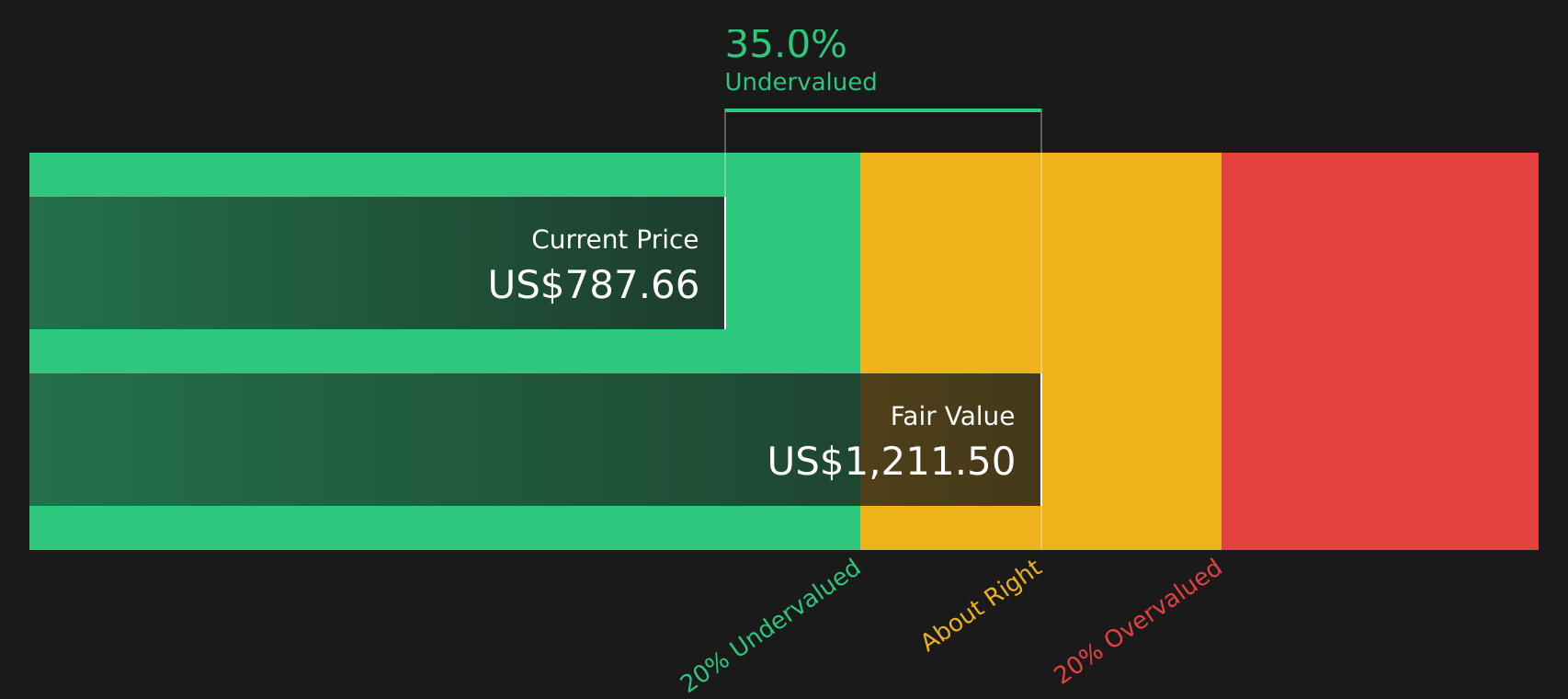

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what Seagate Technology Holdings might be worth today. On this view, Seagate generated about $2.5b of free cash flow over the last twelve months, with the model assuming those cash flows continue growing rather than shrinking over time.

Rolling those projections together, the DCF points to an intrinsic value of about $1,207 per share. Compared with the current share price, this suggests the stock screens as roughly 38.2% undervalued. Despite recent sector selloffs tied to concerns around AI related demand and capital spending cycles, the DCF indicates the market is pricing Seagate below the level implied by its projected cash flows.

On this cash flow view, Seagate Technology Holdings currently appears undervalued relative to the price investors are paying in the market.

Our Discounted Cash Flow (DCF) analysis suggests Seagate Technology Holdings is undervalued by 38.2%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Does Seagate Technology Holdings Look Undervalued on Earnings?

The P/E ratio is a useful way to think about Seagate Technology Holdings because earnings are a key focus for many investors in established hardware and semiconductor related companies. Seagate currently trades on a P/E of about 70.9x, compared with a Tech sector average of roughly 23.2x and a peer average of about 35.8x.

On Simply Wall St's fair P/E estimate of 79.3x, which reflects factors such as Seagate's profitability profile, industry, size and risk, the current multiple sits below what this tailored benchmark suggests. That means the stock screens as undervalued on earnings relative to where this framework would typically place it, even though the absolute P/E level is high against broad sector norms and peers.

On the P/E multiple, Seagate Technology Holdings looks undervalued relative to the fair ratio implied by its earnings profile.

See what the numbers say about this price — find out in our valuation breakdown.

The Seagate Technology Holdings Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Seagate Technology Holdings are designed as the link between the current valuation puzzle and the specific assumptions about growth, margins and earnings that would need to hold for the stock to be worth meaningfully more or less than today's price. They sit on Simply Wall St's Community page. Each Narrative connects its number to a clear view of where Seagate Technology Holdings' growth, profitability and risks might go next, giving you something concrete to revisit as new information comes through.

Community views on Seagate Technology Holdings sit far apart, with one side focused on AI driven upside and the other on HDD cycle risks.

Bull case: 22% undervalued

"Ongoing agreements with large cloud and hyperscale customers indicate strong nearline exabyte demand, providing revenue visibility into calendar year 2026..."

Read the full Bull Case to see why Seagate Technology Holdings could be undervalued

Bear case: 32% overvalued

"Despite strong near-term revenue growth and margin expansion fueled by build-to-order contracts and high-capacity HDD adoption, the accelerating shift of cloud service providers and hyperscalers toward SSDs and other energy-efficient storage solutions will structurally undermine Seagate's long-term addressable markets..."

Read the full Bear Case to see why Seagate Technology Holdings could be overvalued

Do you think there's more to the story for Seagate Technology Holdings? Head over to our Community to see what others are saying!

The Bottom Line

For Seagate Technology Holdings, both the Discounted Cash Flow (DCF) intrinsic value estimate and the earnings multiple approach point in the same direction, suggesting the stock still looks undervalued despite the very large move investors have already seen. The broader valuation checks are mixed rather than emphatically supportive, so the discount may be compensation for real risks around capital spending cycles and execution on newer storage technologies. What matters most from here is whether high capacity storage demand linked to AI and cloud spending holds up well enough for Seagate to sustain cash flows at, or above, the levels implied in those models.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com