- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Dropbox (DBX) Earnings Date Puts Its AI Narrative And Valuation Back In Focus

Dropbox (DBX) is back on investors’ radar after the company scheduled its second quarter 2026 earnings release for August 6, with a conference call and webcast planned for the same afternoon.

See our latest analysis for Dropbox.

At a share price of $30.45, Dropbox has seen momentum build in recent months, with a 30 day share price return of 11.54% and a 90 day share price return of 25.46%, while the 1 year total shareholder return of 13.07% sits alongside a flatter 5 year total shareholder return, as investors weigh upcoming earnings and recent insider selling disclosures.

If Dropbox’s recent run has you thinking about where else growth and cash generation might intersect in tech, it could be worth sizing up 62 profitable AI stocks that aren't just burning cash.

Dropbox now trades above the average analyst price target yet screens at a discount to some intrinsic value estimates. Is the market being too cautious on a slower revenue line, or does that caution fit the story investors see?

Most Popular Narrative: 16.4% Overvalued

Compared with the narrative fair value of $26.17, Dropbox at $30.45 sits above what that framework suggests, putting more weight on how the story unfolds from here.

The planned expansion and deeper integration of AI-driven productivity tools (Dash), including upcoming self-serve offerings and seamless bundling with Dropbox's existing file sync-and-share product, position the company to capture higher ARPU and accelerate recurring revenue growth as digital transformation and hybrid work drive demand for intelligent, collaborative cloud platforms.

Read the complete narrative. Read the complete narrative.

Want to see what keeps that fair value below the current price? The narrative leans on steady margins, modest revenue assumptions, and a specific future earnings multiple. Curious how those pieces fit together and what has to hold true to support $26.17 as the anchor point?

Result: Fair Value of $26.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Dropbox’s recent revenue and annual recurring revenue declines, alongside pressure on ARPU from lower priced plans and downsells, could still challenge the current narrative of overvaluation.

Find out about the key risks to this Dropbox narrative.

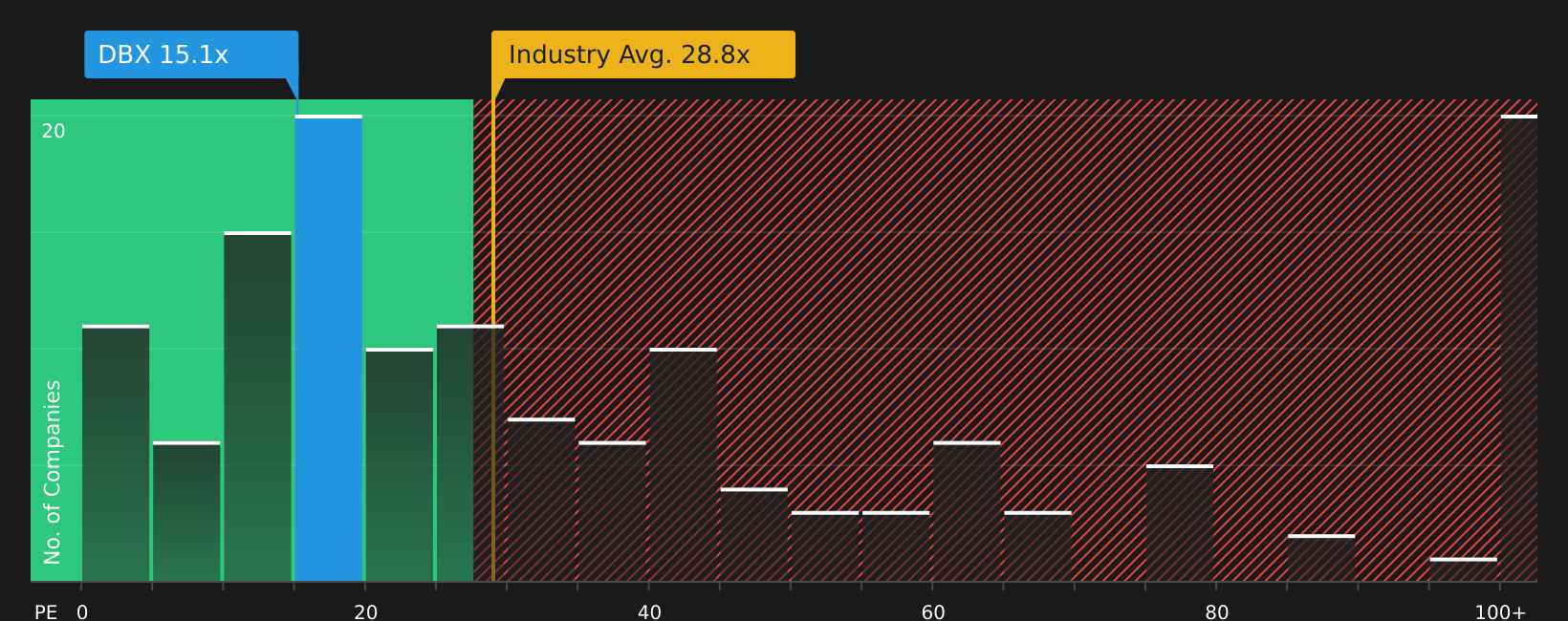

Another View: Dropbox Through The Earnings Multiple Lens

The analyst narrative flags Dropbox as 16.4% overvalued versus a $26.17 fair value, yet the current P/E of 15x tells a different story. That multiple sits well below the US Software industry at 28.8x, the peer average at 19.1x, and an estimated fair ratio of 20.1x. This suggests the market is pricing in a meaningful margin of caution. If earnings hold up, is that gap a valuation buffer or a sign investors are expecting more pressure ahead?

See what the numbers say about this price, find out in our valuation breakdown.See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed signals around Dropbox have you undecided, this is the moment to review the numbers yourself and act with intent using 3 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Dropbox?

If Dropbox has sharpened your focus on valuation and quality, do not stop here. The wider market holds plenty of other stocks worth your attention.

- Target resilient potential by scanning companies with stronger downside protection and consistent profiles through the 82 resilient stocks with low risk scores.

- Spot underappreciated opportunities that combine quality and price discipline using the screener containing 20 high quality undiscovered gems.

- Prioritise balance sheet strength and core fundamentals before the crowd catches on by checking the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com