- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Alkermes (ALKS) Following Alixorexton Data, Is The Bull Case Already Priced In?

Alkermes (ALKS) recently reported interim data from its long term extension study of alixorexton in narcolepsy and idiopathic hypersomnia, highlighting sustained treatment effects through 24 weeks and a generally favorable safety and tolerability profile.

See our latest analysis for Alkermes.

The latest alixorexton data lands after a strong run in Alkermes stock, with a 30 day share price return of 17.8% and a 90 day share price return of 50.42%. This has contributed to an 83.79% year to date share price return and a 5 year total shareholder return of 118.58%, which together indicate that momentum has been building over both shorter and longer periods.

If positive drug news such as Alkermes' alixorexton update has your attention, this may be a good moment to widen your watchlist with 39 healthcare AI stocks

Alkermes now has a larger revenue base, positive net income and a stock that has surged in recent months. The next step is to determine whether you are paying a fair price for that strength or stretching at these levels.

Most Popular Narrative: 8.9% Overvalued

At a last close of $51.94 versus a narrative fair value of $47.69, Alkermes is framed as slightly ahead of where the most widely followed narrative suggests, putting the focus on what assumptions are doing the heavy lifting.

Results from the Vibrance 1 Phase II study and the expanding orexin agonist pipeline de-risk the company's long-term R&D strategy, opening avenues to additional addressable disorders beyond narcolepsy and highlighting potential for future multi-indication revenue streams pending successful late-stage trials and commercialization.

Read the complete narrative. Read the complete narrative.

Want to understand why Alkermes might justify a premium to many US biotechs? This narrative leans heavily on compound earnings growth, wider margins, and a rich future earnings multiple. Curious which revenue and profit assumptions have to line up for that to work? The full storyline spells out the numbers behind that 8.9% gap.

This most followed view then translates those building blocks into a fair value of $47.69 per share, using an 8.05% discount rate and a future earnings outlook that implies a higher P/E than the broader US Biotechs industry. The current share price sitting slightly above that mark means the narrative does not see Alkermes as stretched, but it also does not leave a large margin of safety if the earnings path or orexin execution differ from expectations.

Result: Fair Value of $47.69 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Alkermes' reliance on a concentrated set of proprietary products and rising R&D spend around alixorexton could quickly challenge this premium narrative if expectations slip.

Find out about the key risks to this Alkermes narrative.

Another View on Alkermes Valuation

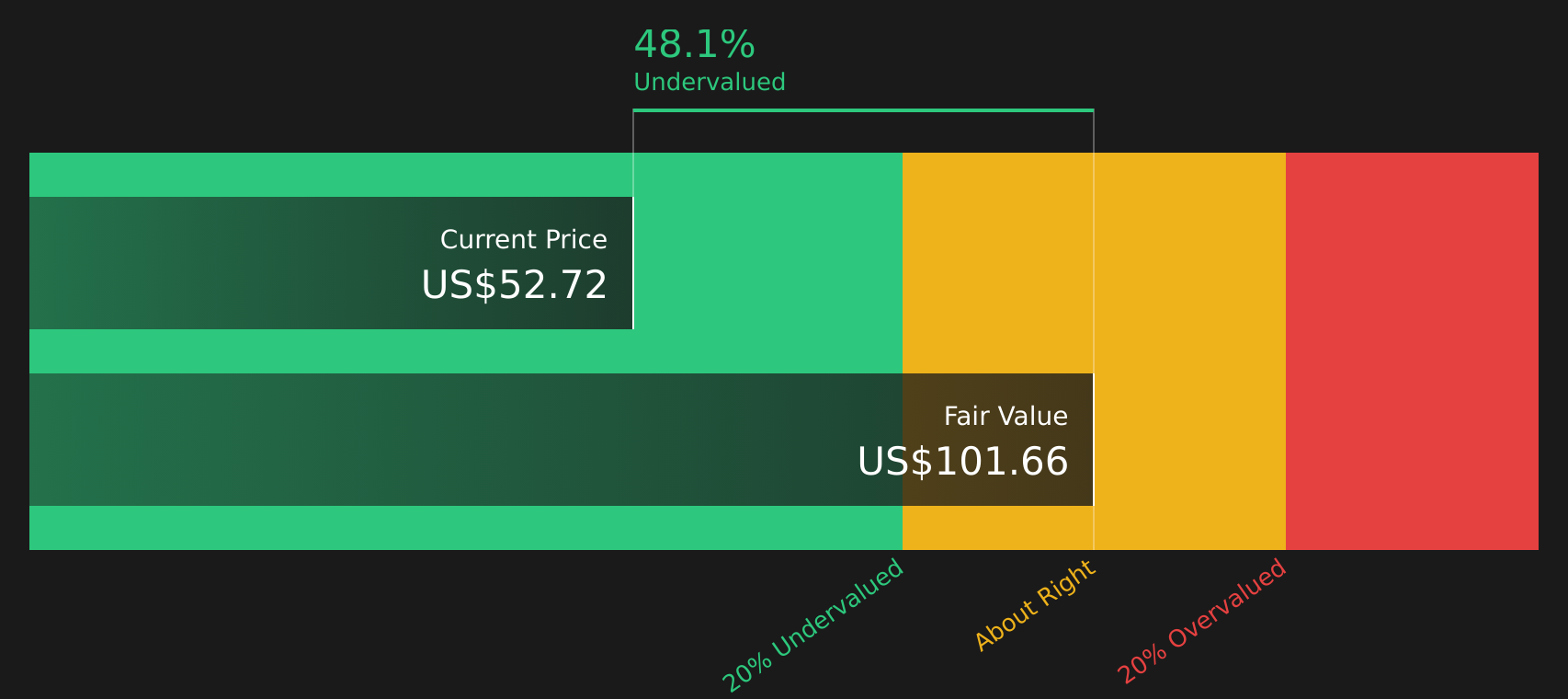

While the analyst narrative suggests Alkermes is 8.9% overvalued around $51.94 versus a $47.69 fair value, the Simply Wall St DCF model points in the opposite direction, with an estimate of $100.22. That gap flags a very different risk reward trade off, so which framework do you trust more for a long term view?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Alkermes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals around Alkermes and not sure what to make of them? Take a closer look at both sides of the story with 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Alkermes?

If Alkermes has sharpened your focus, do not stop here. Broaden your opportunity set with a few targeted stock ideas that match your goals.

- Spot potential upside in quality companies trading below their estimated worth by scanning 49 high quality undervalued stocks.

- Strengthen your income stream by reviewing higher yielding opportunities through 8 dividend fortresses.

- Prioritize resilience and capital preservation by focusing on companies highlighted in 82 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com