- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Should Gibson Energy’s CA$400 Million Notes Issue Reshape Its Infrastructure Dividend Strategy for (TSX:GEI) Investors?

- In early July 2026, Gibson Energy Inc. completed an agreement to issue CA$400 million of 4.45% senior unsecured notes maturing January 9, 2034, offered in Canada via a private placement syndicated by RBC Capital Markets, BMO Capital Markets, and CIBC Capital Markets.

- The company plans to use the proceeds to pay down its revolving credit facility and support debt linked to its Chauvin Infrastructure Assets acquisition, effectively reshaping its funding mix while backing recent infrastructure expansion.

- We’ll now examine how this CA$400 million senior unsecured notes issuance could influence Gibson Energy’s existing infrastructure-and-dividend-focused investment narrative.

Uncover the next big thing with 10 elite penny stocks that balance risk and reward.

Gibson Energy Investment Narrative Recap

To own Gibson Energy, you need to believe in the durability of fee-based midstream cash flows, supported by contracted storage and export infrastructure and an ongoing commitment to dividends. The new CA$400,000,000 senior notes look more like a funding mix clean up than a game changing move, but they matter at the margin for the near term catalyst around balance sheet flexibility. They also sit against the risk that interest costs stay uncomfortable while earnings remain uneven.

The equity offering that raised about CA$200,000,000 earlier in 2026 feels particularly relevant alongside this latest bond issue, because both actions speak to how Gibson is financing its Chauvin and Gateway linked build out. Together, these financing steps sit behind the same catalyst investors are watching most closely in the short term: whether recently completed and acquired infrastructure can translate into steadier, fee-based earnings that comfortably support the current dividend and ongoing debt service.

Yet for investors, the bigger concern to keep in mind is the company’s reliance on North American crude volumes and the possibility that...

Read the full narrative on Gibson Energy (it's free!)

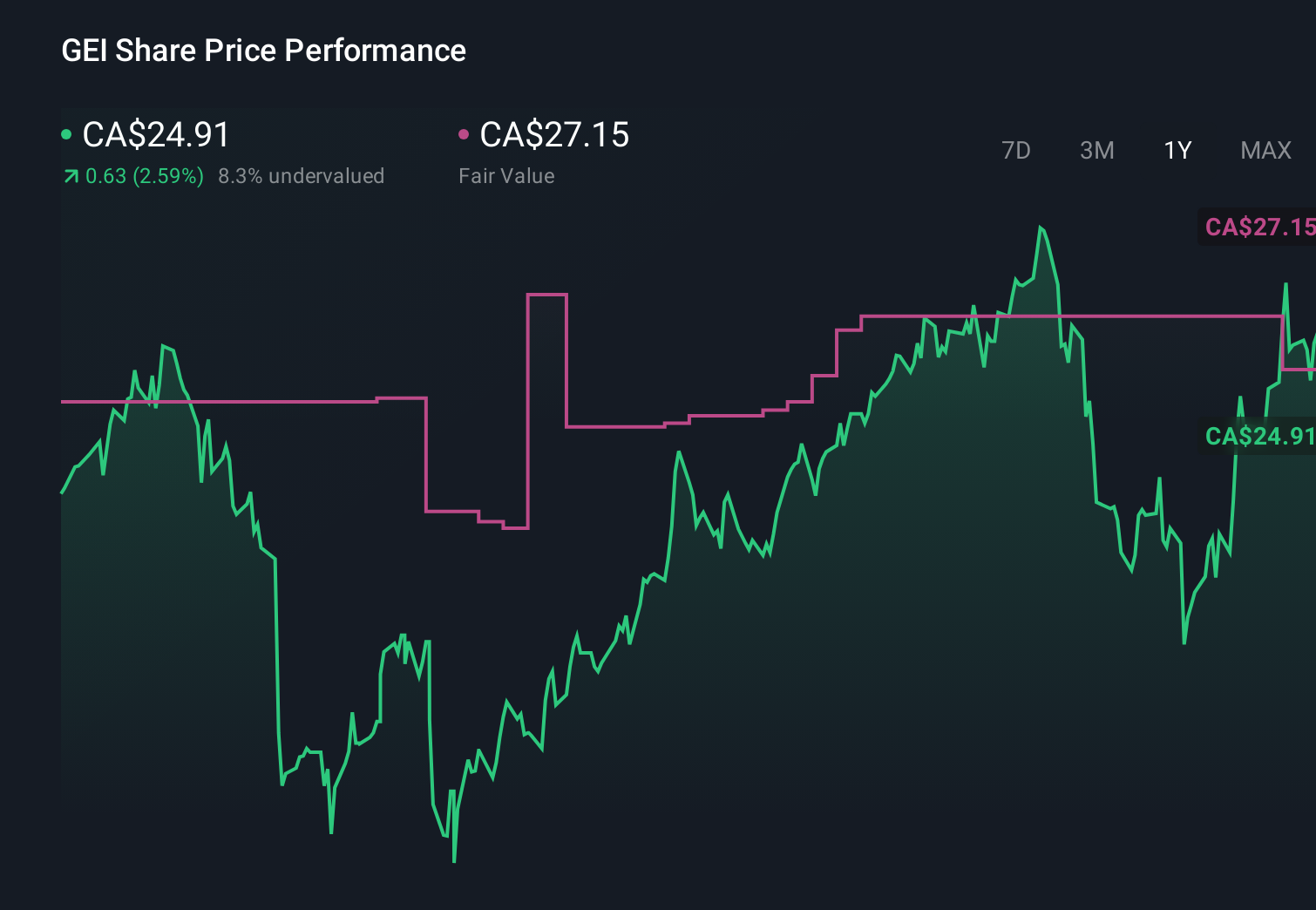

Gibson Energy's narrative projects CA$10.6 billion revenue and CA$290.9 million earnings by 2029. This implies fairly flat yearly revenue growth and about a CA$144.6 million earnings increase from CA$146.3 million today.

Uncover how Gibson Energy's forecasts yield a CA$30.46 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members offer only 2 fair value views, spanning from about CA$30.46 up to roughly CA$82.88, showing how far apart individual expectations can be. Set against this wide range, the financing shift toward longer term unsecured notes focuses attention on Gibson’s ability to keep debt service manageable if marketing EBITDA stays under pressure, so it is worth weighing several perspectives before forming a view.

Explore 2 other fair value estimates on Gibson Energy - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Gibson Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gibson Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gibson Energy's overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com