- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

UK Dividend Stocks Featuring Kainos Group And 2 Other Top Picks

The United Kingdom's stock market has been facing challenges recently, with the FTSE 100 index closing lower due to weak trade data from China, highlighting concerns over global economic recovery. In this environment, dividend stocks can offer investors a degree of stability and income potential, making them an attractive option for those looking to navigate uncertain markets.

Top 10 Dividend Stocks In The United Kingdom

| Name | Dividend Yield | Dividend Rating |

| Telecom Plus (LSE:TEP) | 5.77% | ★★★★★☆ |

| Pollen Street Group (LSE:POLN) | 6.67% | ★★★★★☆ |

| Multitude (LSE:0R4W) | 9.82% | ★★★★★☆ |

| MONY Group (LSE:MONY) | 6.16% | ★★★★★★ |

| James Halstead (AIM:JHD) | 6.91% | ★★★★★☆ |

| Dunelm Group (LSE:DNLM) | 8.13% | ★★★★★☆ |

| BTG Consulting (AIM:BTG) | 4.28% | ★★★★★☆ |

| Arbuthnot Banking Group (AIM:ARBB) | 6.39% | ★★★★★☆ |

| 4imprint Group (LSE:FOUR) | 4.52% | ★★★★★☆ |

| 3i Group (LSE:III) | 3.20% | ★★★★★☆ |

Click here to see the full list of 46 stocks from our Top UK Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

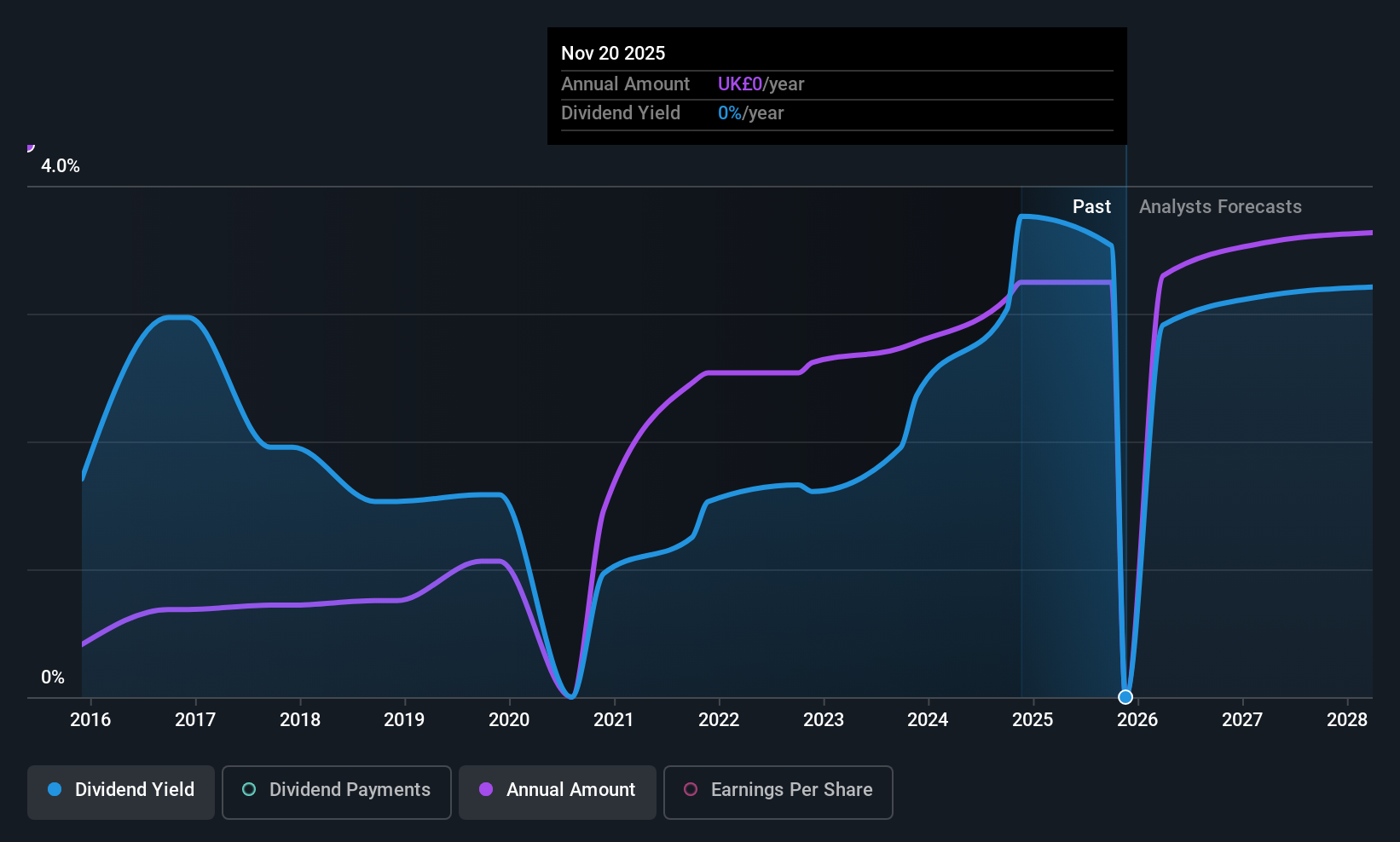

Kainos Group (LSE:KNOS)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Kainos Group plc provides digital technology services across the United Kingdom, Ireland, the Americas, Central Europe, and internationally, with a market cap of £959.30 million.

Operations: Kainos Group's revenue is primarily derived from Digital Services (£241.74 million), Workday Products (£81.75 million), and Workday Services (£107.61 million).

Dividend Yield: 3.6%

Kainos Group's dividend payments are covered by both earnings and cash flows, with payout ratios of 83.4% and 68.8%, respectively, indicating sustainability despite a historically volatile track record. Recent insider selling raises concerns, but the company has announced a modest dividend increase for the year to 29.6 pence per share, distributed at 70% of adjusted profit after tax. Earnings growth remains robust with sales reaching £431.1 million and net income at £42.5 million for the year ending March 31, 2026.

- Take a closer look at Kainos Group's potential here in our dividend report.

- In light of our recent valuation report, it seems possible that Kainos Group is trading behind its estimated value.

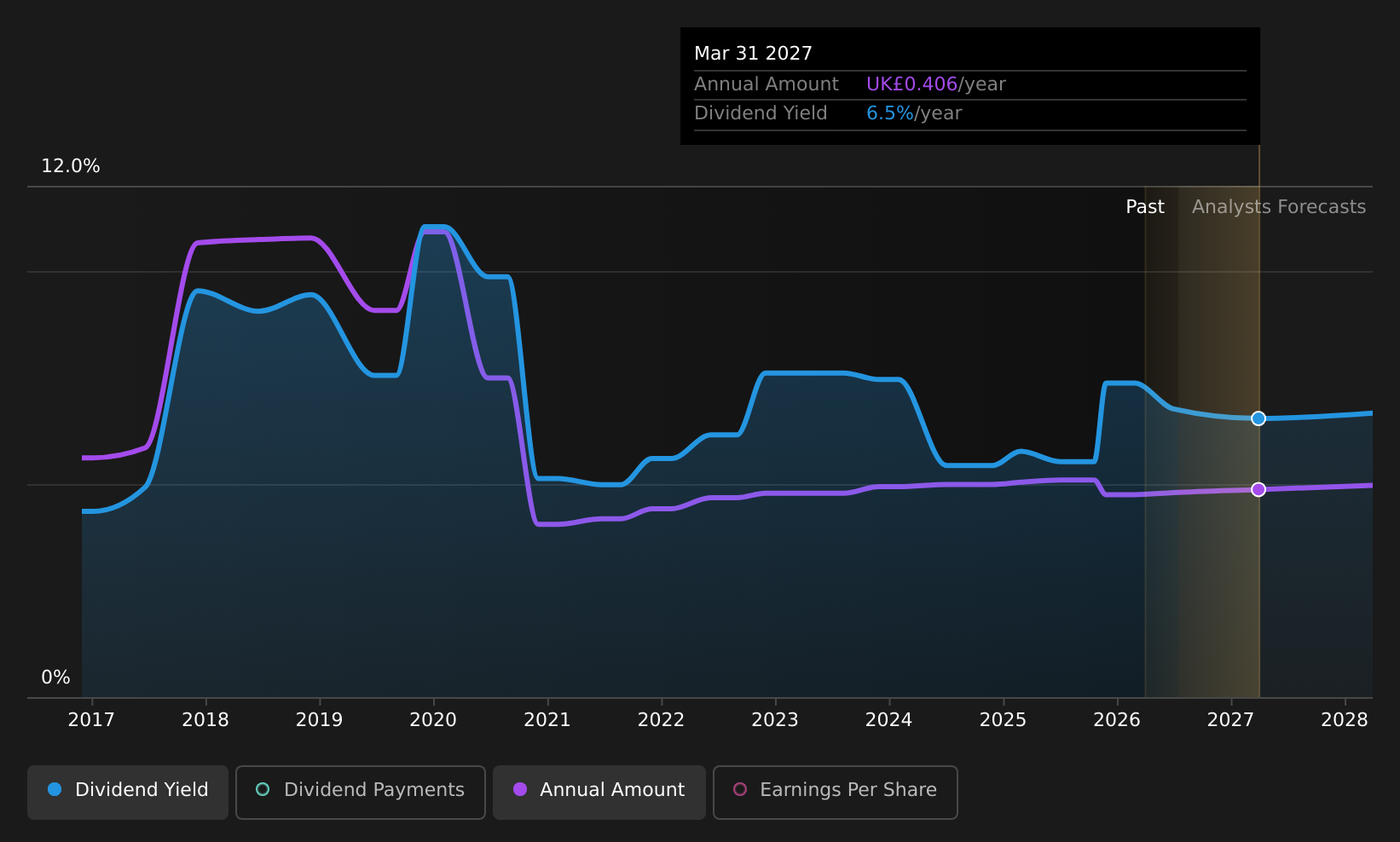

PayPoint (LSE:PAY)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: PayPoint plc provides payments and banking, shopping, and e-commerce services in the United Kingdom and New Zealand, with a market cap of £383.95 million.

Operations: PayPoint plc generates revenue from its Love2shop segment, which accounts for £158.23 million, and its Pay Point segment, contributing £178.78 million.

Dividend Yield: 6.3%

PayPoint's dividend yield ranks in the top 25% of UK payers, supported by a low cash payout ratio of 24% and an earnings payout ratio of 67.4%, though its dividend history is unstable. Recent earnings showed significant growth, with net income rising to £39.33 million, which supports the declared final dividend increase to 20 pence per share. The company completed a substantial buyback program, repurchasing shares worth £45 million since June 2024.

- Click to explore a detailed breakdown of our findings in PayPoint's dividend report.

- Our valuation report unveils the possibility PayPoint's shares may be trading at a discount.

Rathbones Group (LSE:RAT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Rathbones Group Plc, along with its subsidiaries, offers wealth and asset management services in the United Kingdom and Channel Islands, with a market cap of £1.73 billion.

Operations: Rathbones Group Plc generates revenue through its two main segments: Asset Management, contributing £85.40 million, and Wealth Management, providing £837.90 million.

Dividend Yield: 5.8%

Rathbones Group's dividend yield is among the UK's top 25% at 5.84%, though its history shows volatility and unreliability over the past decade. Despite a low cash payout ratio of 9.6%, dividends are not well covered by earnings, with a high payout ratio of 91.8%. Recent board changes include appointing Kathryn Purves and Angela Seymour-Jackson as directors, which may influence future governance and strategy decisions impacting dividends.

- Get an in-depth perspective on Rathbones Group's performance by reading our dividend report here.

- Our comprehensive valuation report raises the possibility that Rathbones Group is priced lower than what may be justified by its financials.

Turning Ideas Into Actions

- Explore the 46 names from our Top UK Dividend Stocks screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com