- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Heightened Trading and Seaborne Trade Shifts Might Change The Case For Investing In Frontline (FRO)

- In recent days, Frontline has drawn increased market attention as heightened trading and options activity coincided with new developments in its global shipping operations, boosting its visibility across the NYSE Composite.

- This renewed focus on Frontline’s role in worldwide tanker shipping underscores how shifts in seaborne trade patterns can quickly reframe investor interest in the company’s core business.

- Building on this heightened trading and options activity, we’ll now examine how these developments may influence Frontline’s existing investment narrative.

The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Frontline Investment Narrative Recap

To own Frontline, you need to believe that global crude and product flows will keep supporting healthy tanker utilization and that the company can convert that demand into solid cash generation despite industry cyclicality. The recent spike in trading and options activity mainly reflects shifting sentiment around these shipping fundamentals; it does not, on its own, change the key near term catalyst of freight rate strength or the biggest current risk of volatile spot exposure.

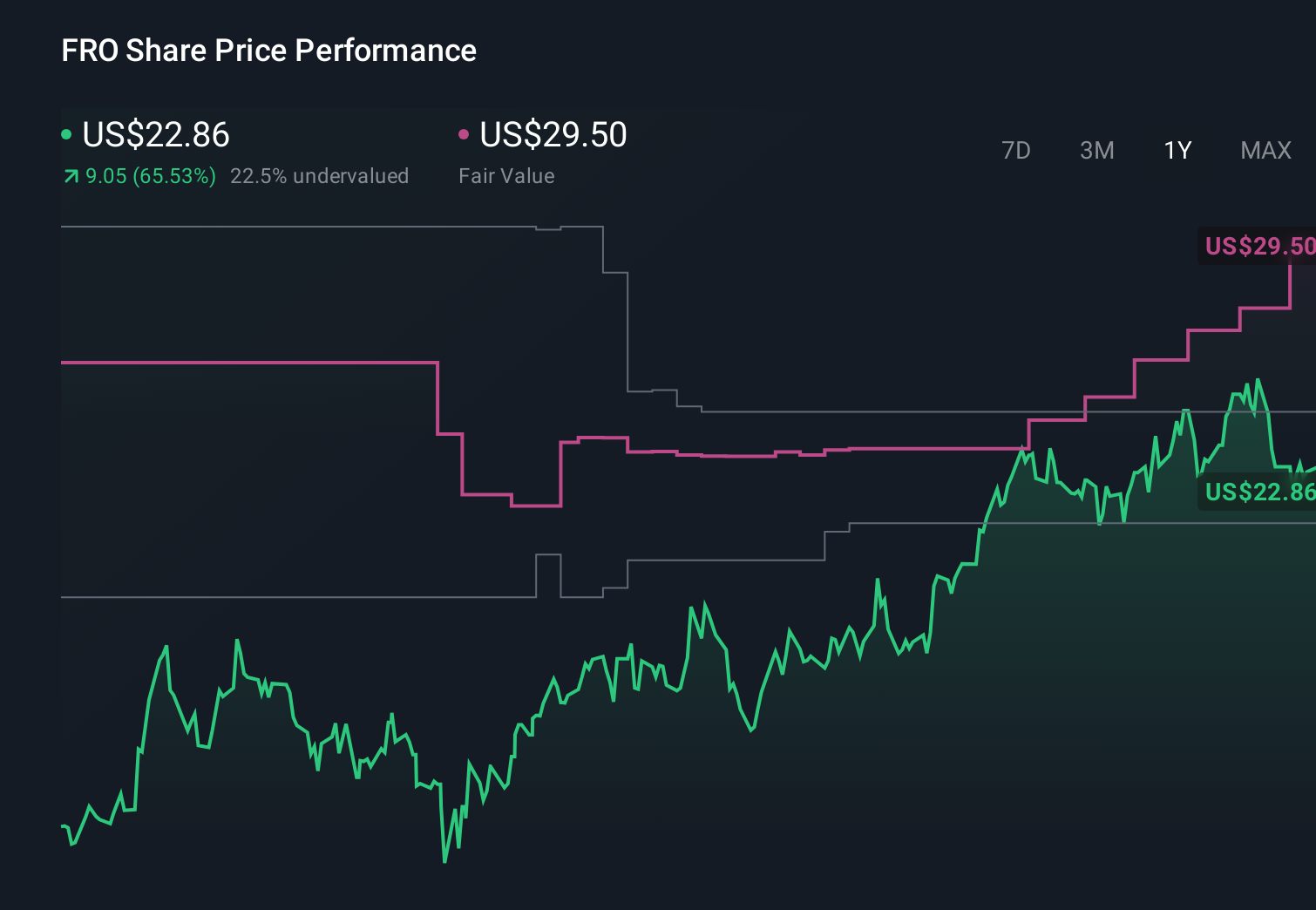

The most relevant recent announcement alongside this renewed attention is Frontline’s May 2026 quarterly update, where the company reported Q1 2026 revenue of US$929.33 million and net income of US$559.12 million, alongside a higher US$1.55 per share dividend. For many investors, this kind of earnings and payout profile is central to assessing how sensitive Frontline might be if freight markets soften or regulatory costs rise from here.

Yet, against this strong recent quarter, investors should still weigh the risk that prolonged spot market weakness could...

Read the full narrative on Frontline (it's free!)

Frontline's narrative projects $1.6 billion revenue and $697.7 million earnings by 2029.

Uncover how Frontline's forecasts yield a $41.25 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting earnings of about US$786.8 million by 2029 and a richer valuation multiple, which contrasts sharply with concerns about rising regulatory costs and shows how widely opinions can differ, especially if this latest shipping news alters views on future trade flows.

Explore 4 other fair value estimates on Frontline - why the stock might be worth just $41.25!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Frontline research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Frontline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontline's overall financial health at a glance.

No Opportunity In Frontline?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com