- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Xiaomi Stock Leads 3 Asian Tech Picks Worth Watching After The AI Selloff

Asian tech stocks have been hit hard by renewed doubts around the AI trade, with chipmakers in particular facing sharp selling just as earnings headlines from ASML and TSMC raise fresh questions about what is already priced in. For investors, broad sector pressure can sometimes leave solid, well capitalized companies trading at levels that do not fully reflect their balance sheet strength or long term potential. This article looks at three stocks from our Undervalued Asian Technology Stocks screener that are directly exposed to the latest news, and explains why some readers may see current volatility as a chance to reassess them.

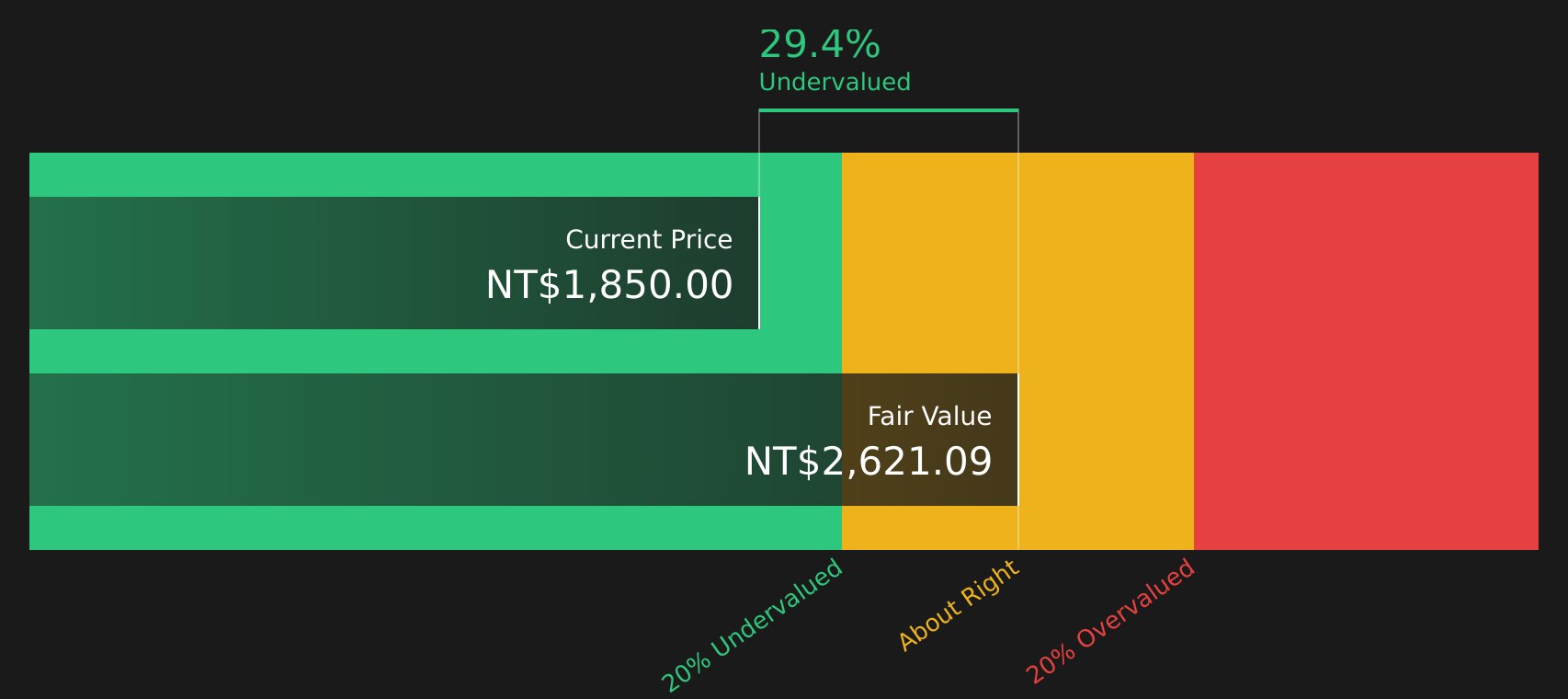

Chroma ATE (TWSE:2360)

Overview: Chroma ATE is a Taiwan based test equipment specialist that builds hardware, software and automated systems used to check and validate semiconductors, power electronics, batteries, EV components and displays for industries from computing and communications to aerospace and green energy worldwide.

Operations: Chroma ATE generates most of its revenue from its Measuring Instruments Business at NT$54.4b and a smaller portion from the Automatic Equipment Department at NT$1.1b, with only modest contributions from other segments.

Market Cap: NT$843.1b

Chroma ATE stands out in the current AI related selloff because it sits in the testing equipment segment where demand for AI servers, advanced packaging and EV power systems all feed into orders for its tools. At the same time, the stock is flagged as trading below an internally estimated fair value, while still posting very high margins and rapid earnings growth. Over 95% of revenue is tied to testing equipment, inventory has risen and funding leans on external borrowing, which could magnify any downturn in capex. With recent quarterly results showing strong revenue and EPS, the key question for you is whether the current volatility fairly reflects those risks or is giving you a rare entry point to consider in a high quality test platform business.

Chroma ATE’s high margin test platform story and AI exposure are only half the picture. The real tension is how its valuation stacks up against those fundamentals in the DCF valuation analysis for Chroma ATE

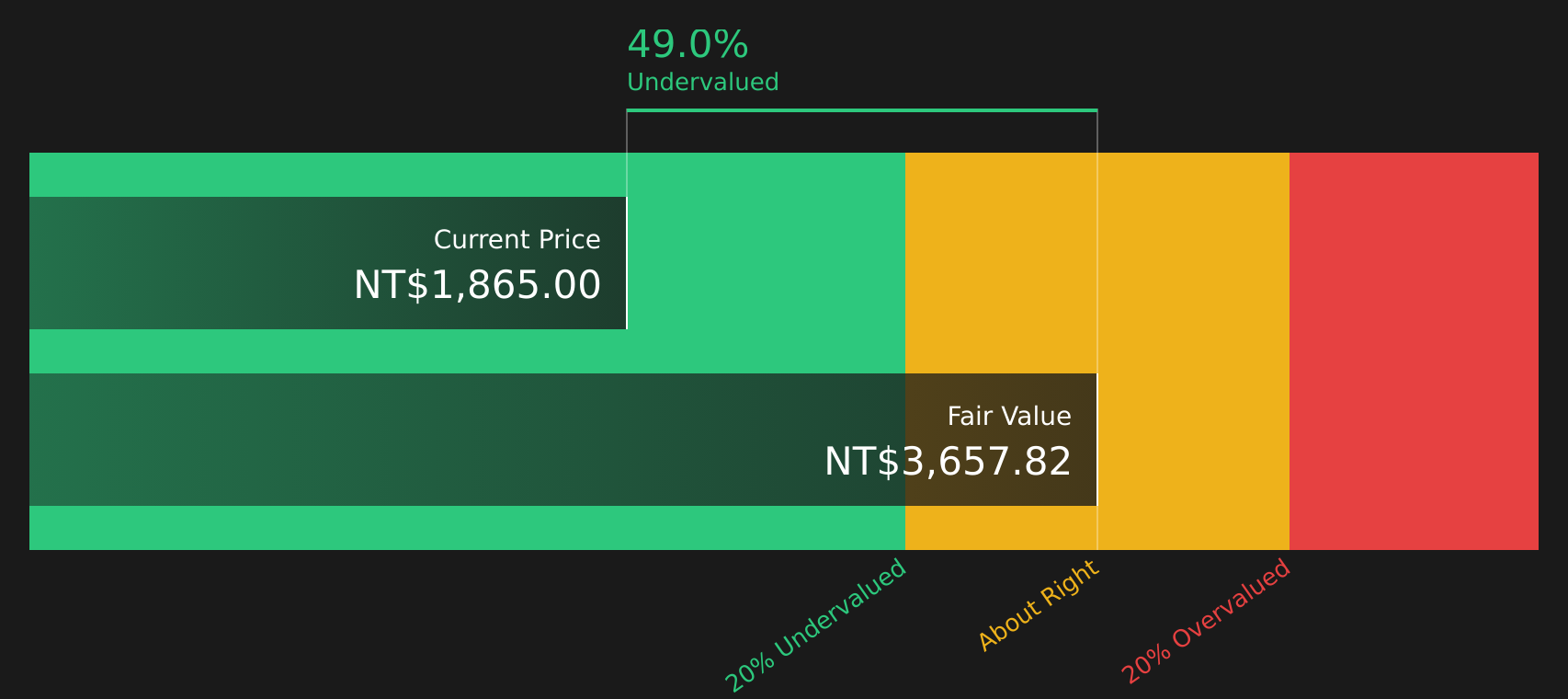

Xiaomi (SEHK:1810)

Overview: Xiaomi is a Beijing headquartered technology company that designs and sells smartphones, smart home devices and a wide range of connected consumer electronics, while also offering internet services and developing smart electric vehicles to tie users into a single ecosystem.

Operations: Xiaomi generates most of its revenue from Smartphones at about CN¥180.1b, IoT and Lifestyle Products at CN¥115.5b, and Smart EV, AI and Other New Initiatives at CN¥107.4b, with smaller contributions from Internet Services at CN¥37.8b and Other Related Businesses at CN¥4.3b.

Market Cap: HK$706.6b

Investors looking at Xiaomi today are getting a large consumer tech and smart EV platform that is still priced below its estimated fair value and trading on a P/E below many Asian tech peers. Analysts expect earnings to grow around 20% a year over the next 3 years. The company is pushing into premium smartphones, AI powered home appliances and electric vehicles, which could deepen its ecosystem and lift margins if R&D spending translates into sticky customers and higher value services. At the same time, you need to weigh intense global smartphone competition, higher memory and component costs, reliance on external borrowing and a recent one off gain that clouds earnings quality. The open question is whether the current discount properly reflects those risks or underestimates Xiaomi’s long term ecosystem story.

Momentum around Xiaomi’s ecosystem pivot and smart EV push is building, yet the valuation gap and questions about earnings quality are not fully priced in. It is therefore worth reading the analysis report for Xiaomi.

Lotes (TWSE:3533)

Overview: Lotes is a Taiwan based manufacturer of precision electronic connectors, sockets and hardware that sit between chips, circuit boards and cables in everything from PCs and servers to cars and consumer devices worldwide.

Operations: Lotes generates essentially all of its NT$35.3b revenue from Electronic Components & Parts, selling into Chinese Mainland, Taiwan and other international markets.

Market Cap: NT$226.7b

Lotes provides exposure to global semiconductor and electronics demand through the quieter but essential connector and socket layer. It currently screens as undervalued versus an internal fair value estimate, with a P/E below industry averages. Forecast earnings growth of about 29.1% a year and net profit margins in the low 20% range indicate a business that is already profitable, while recent quarterly numbers show higher revenue and EPS year on year. On the risk side, dividends are not well covered by free cash flow and the balance sheet relies entirely on higher risk external borrowing, so funding conditions matter. With AI hardware volatility pressuring component suppliers, the key question is whether the market is underestimating how central Lotes is to the next phase of hardware growth in Asia.

Lotes appears to be an accelerating earnings story within a connector supplier, with a P/E below industry averages and solid margins. See how those pieces fit together in the 4 key rewards and 2 important warning signs (1 is major!)

The three stocks in this article are just a starting point, and the full Undervalued Asian Technology Stocks screener surfaces 31 more Asian technology companies with balance sheets and valuations that raise equally compelling questions. Use Simply Wall St to identify and analyze the specific catalysts, value angles and business narratives that matter to you so you can focus on the highest conviction opportunities in this part of the market.

Take Control of Your Investment Journey

If Xiaomi or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others?

Markets move fast and the freshest ideas do not stay under the radar for long. Spot potential breakouts, shifting momentum and dropping entry points before the crowd, then act promptly.

- Track cash rich companies quietly building momentum by scanning the 220 high quality undervalued stocks while valuations and balance sheets still line up in your favor.

- Catch early movers in intelligent automation by running the 32 robotics and automation stocks so you see which enablers of factory and warehouse upgrades are flying under the radar for now.

- Consider structural demand for electrification and data centers by checking the 35 power grid technology and infrastructure stocks before infrastructure spending headlines fully reflect developments in this space.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com