- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is ON Semiconductor (ON) Fairly Valued After Its $7b Deal?

ON Semiconductor stock has delivered a 145.7% return over the past five years, yet recent valuation checks suggest the shares may be trading at a premium to their intrinsic value estimate from a Discounted Cash Flow (DCF) model. That tension between a strong long term result and a DCF view that screens the stock as overvalued is front of mind for investors watching the latest swings in semiconductor sentiment.

- A 145.7% gain over five years highlights how ON Semiconductor has already generated substantial value for shareholders, which raises the bar for future returns at today’s price levels.

- Recent news around the planned Synaptics acquisition and ongoing manufacturing footprint changes can support expectations for future growth, while sector wide concerns about rich semiconductor valuations and a potential cooling in AI related demand remain a key risk to the stock’s rating.

- ON Semiconductor scores just 2 out of 6 on broader valuation checks, which leans more toward the shares looking expensive than like a clear bargain on multiple measures.

The stock’s next move may depend on whether ON Semiconductor’s current price already more than reflects its intrinsic value, or still leaves enough upside to compensate for the risks now being priced into the semiconductor sector.

Find out why ON Semiconductor's 48.3% return over the last year is lagging behind its peers.

Is ON Semiconductor Getting Expensive on Cash Flow?

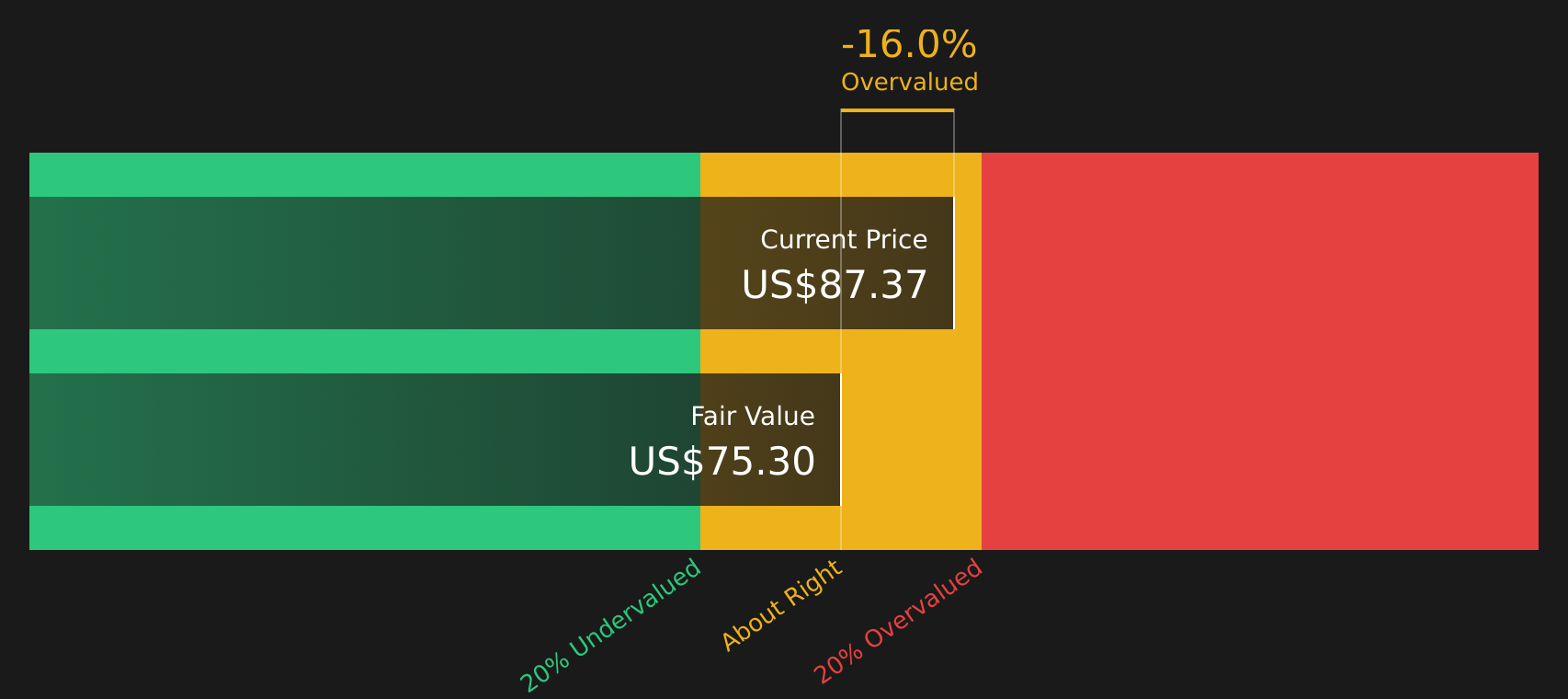

The Discounted Cash Flow (DCF) method estimates what ON Semiconductor might be worth based on the cash it is expected to generate for shareholders. For ON Semiconductor, the model uses latest twelve month free cash flow of about $745 million and assumes cash flows grow from this base rather than shrink, then discounts those future figures back to today.

On this basis, the 2 Stage Free Cash Flow to Equity model points to an intrinsic value around $75 per share. With the stock price screening roughly 16.8% above that estimate, ON Semiconductor appears overvalued on this cash flow view. Recent headlines about a planned $7 billion Synaptics acquisition, alongside plant divestments, help explain why investors may be paying up for future growth even though the DCF comes out lower than the current price.

Putting it together, the Discounted Cash Flow (DCF) workup indicates that ON Semiconductor stock currently screens as overvalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests ON Semiconductor may be overvalued by 16.8%. Discover 49 high quality undervalued stocks or create your own screener to find better value opportunities.

Where Does ON Semiconductor Sit on Earnings?

The P/E ratio is a useful lens for ON Semiconductor because earnings are a key focus for chip stocks that are still reinvesting heavily in growth. ON Semiconductor currently trades on about 59.8x earnings, which sits below the broader semiconductor industry average of 62.6x and also below a peer group average of 73.8x.

A more tailored yardstick is the fair P/E ratio of 54.9x, which reflects what might be reasonable given ON Semiconductor’s size, margins and risk profile. Against that benchmark, the current multiple is a little higher, but not significantly out of line with what investors are paying for comparable semiconductor stocks.

Overall, ON Semiconductor appears roughly fairly valued on its P/E multiple, with only a modest premium to its modelled fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The ON Semiconductor Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for ON Semiconductor take the valuation puzzle a step further by spelling out the future assumptions on growth, margins and earnings that would need to hold for the stock to be worth materially more or less than today's price. These narratives sit on the company's Community page. Each narrative links a specific fair value to a particular path for ON Semiconductor's catalysts and risks, so you can track over time which version of events is actually unfolding.

Community views on ON Semiconductor sit far apart, with one side leaning into electrification and AI power, and the other focused on margin risk and geopolitics.

Bull case: 39% undervalued

"ON's early-mover advantage in next-generation AI data center power architectures in partnership with XPU leaders like NVIDIA positions the company to capitalize on the exponential increase in semiconductor content per watt. This places their power products at the center of two structural growth curves: AI and high-power efficiency. This could open up a far bigger total addressable market and create a more durable earnings tailwind…"

Read the full Bull Case to see why ON Semiconductor could be undervalued

Bear case: roughly fairly valued

"Intensifying competition and potential overcapacity in power management and silicon carbide products threaten to erode prices and result in higher inventory levels, making it more difficult for ON Semiconductor to achieve sustained revenue growth and jeopardizing margin expansion targets…"

Read the full Bear Case to see why ON Semiconductor could be overvalued

Do you think there's more to the story for ON Semiconductor? Head over to our Community to see what others are saying!

The Bottom Line

For ON Semiconductor, the Discounted Cash Flow (DCF) workup flags the stock as overvalued, while the P/E comparison suggests pricing that is about right relative to peers. That gap reflects a market willing to pay for growth expectations and sector sentiment, even though the intrinsic value estimate sits below the current share price and broader valuation checks are weak. From here, the crux of the debate is whether ON Semiconductor can deliver the growth and margin profile implied in the current multiple, or whether cash flow realities eventually pull the valuation closer to the intrinsic value estimate.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com