- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Ultra Clean Holdings (UCTT) Could Be 14% Undervalued As New CFO Appointment Draws Focus

New CFO Appointment Draws Attention to Ultra Clean Holdings Stock

Ultra Clean Holdings (UCTT) has attracted fresh attention after appointing Michael Keogh as its next Chief Financial Officer, effective August 5, 2026. He previously held a series of senior finance roles at large industrial and technology companies.

See our latest analysis for Ultra Clean Holdings.

Ultra Clean Holdings' share price has pulled back sharply in the short term, with a 1 day share price return of down 9.31% and a 30 day share price return of down 15.29%. However, the year to date share price return of 238.95% and 1 year total shareholder return of 256.43% point to strong longer term momentum that is now consolidating as investors reassess expectations around the incoming CFO and recent capital raising plans.

If you are weighing what could be next for semiconductor related suppliers, it may be a good time to scan a wider set of AI infrastructure opportunities using the 53 AI infrastructure stocks.

Ultra Clean Holdings now trades at $92.60, below the average analyst estimate of $113.40 and close to some intrinsic value models. The key question is where fair value sits after this sharp pullback.

Most Popular Narrative: 13.8% Undervalued

On the most followed narrative, Ultra Clean Holdings' fair value of $107.40 sits above the last close at $92.60, putting the recent pullback in a different light.

Ongoing organizational flattening, cost reduction initiatives, and factory/site consolidation are producing tangible decreases in OpEx, with further improvements expected by Q4, providing sustainable margin enhancement as industry volumes recover (impacts net margins and overall profitability). Progress in vertical integration, particularly the Fluid Solutions business unit, along with deployment of company-wide SAP systems, is set to improve operational efficiency and streamline customer engagement, driving higher margin mix and improved earnings beginning in early 2026 (supports higher net margins and earnings improvement).

Want to see what sits behind that margin story and growth curve? The narrative leans on aggressive revenue ramps, rising profitability and a future valuation multiple that might surprise you.

Result: Fair Value of $107.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Ultra Clean Holdings still faces concentration and demand risks, due to its reliance on a few large customers and ongoing industry weakness that could pressure revenue and margins.

Find out about the key risks to this Ultra Clean Holdings narrative.

Another View on Ultra Clean Holdings Valuation

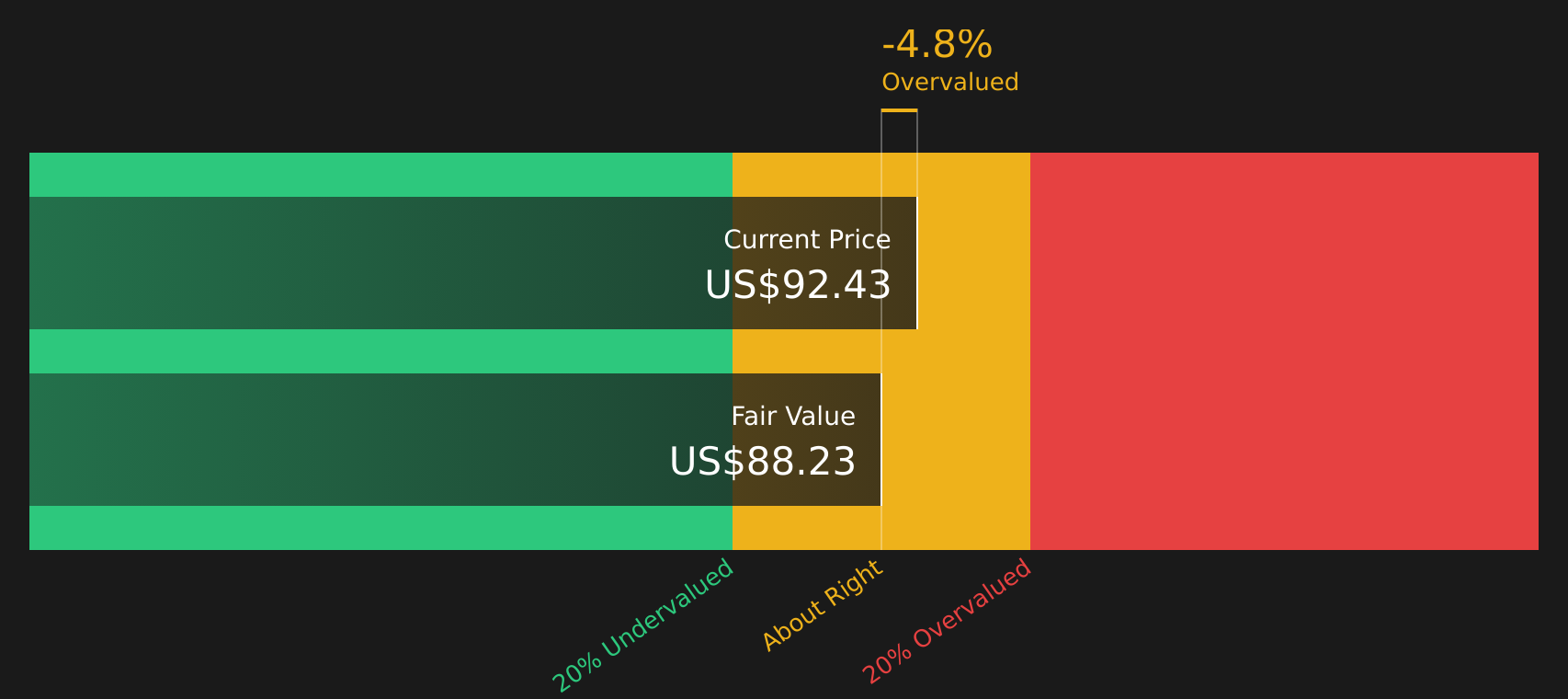

Analysts see Ultra Clean Holdings as undervalued against their $107.40 fair value, but the SWS DCF model points to a different picture. On that framework, the stock at $92.60 sits above an estimated future cash flow value of $88.23, which screens as slightly overvalued. Which storyline do you think fits your expectations for cash generation and risk?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ultra Clean Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After considering both the positive and cautious signals around Ultra Clean Holdings, now is an appropriate moment to review the underlying data and determine your own view, starting with the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Ultra Clean Holdings?

If Ultra Clean Holdings has sharpened your focus, now is the moment to widen your search and uncover other compelling setups before the market prices them in.

- Target potential mispricings by scanning companies that combine quality metrics with attractive entry points using the 49 high quality undervalued stocks.

- Strengthen your income side by reviewing businesses with higher yields that may offer more consistent cash returns through the 8 dividend fortresses.

- Prioritize durability and capital protection by filtering for companies that pair financial resilience with lower overall risk scores via the 82 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com