- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Will Carnival’s Next-Gen Ace Class Flagship Redefine CCL’s Long-Term Brand and Experience Narrative?

- Carnival Cruise Line recently held the steel-cutting ceremony for its next-generation Ace Class flagship, Carnival Destiny, scheduled for delivery in summer 2029 and designed with extensive ocean-facing glass, a high proportion of balcony cabins, and over 70% entirely new onboard venue concepts.

- This marks a major evolution of Carnival’s product, signaling a long-term focus on differentiated ship design, immersive guest experiences, and curated Caribbean, Bahamas, and Mexico itineraries through its Paradise Collection destinations.

- We’ll now explore how this next-generation Ace Class launch, with its focus on outward-facing design and new venues, reshapes Carnival’s investment narrative.

Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

Carnival Investment Narrative Recap

To own Carnival today, you have to believe that leisure cruising and curated destinations can keep filling ships while the company manages a still-heavy debt load and ongoing capex needs. The Ace Class launch, starting with Carnival Destiny in 2029, underlines a long-term product refresh, but it does not materially change the key near term swing factors around balance sheet strength and cash generation.

The most relevant nearby datapoint is Carnival’s continued US$0.15 per share quarterly dividend, affirmed again in July 2026. Together with share buybacks, this highlights management’s confidence in current earnings power, even as investors weigh how much future fleet investments like Ace Class and Paradise Collection buildouts could pressure free cash flow and financial flexibility.

Yet beneath the headline excitement of new ships, investors should also be aware of how Carnival’s sizable debt stack and ongoing refinancing needs could...

Read the full narrative on Carnival (it's free!)

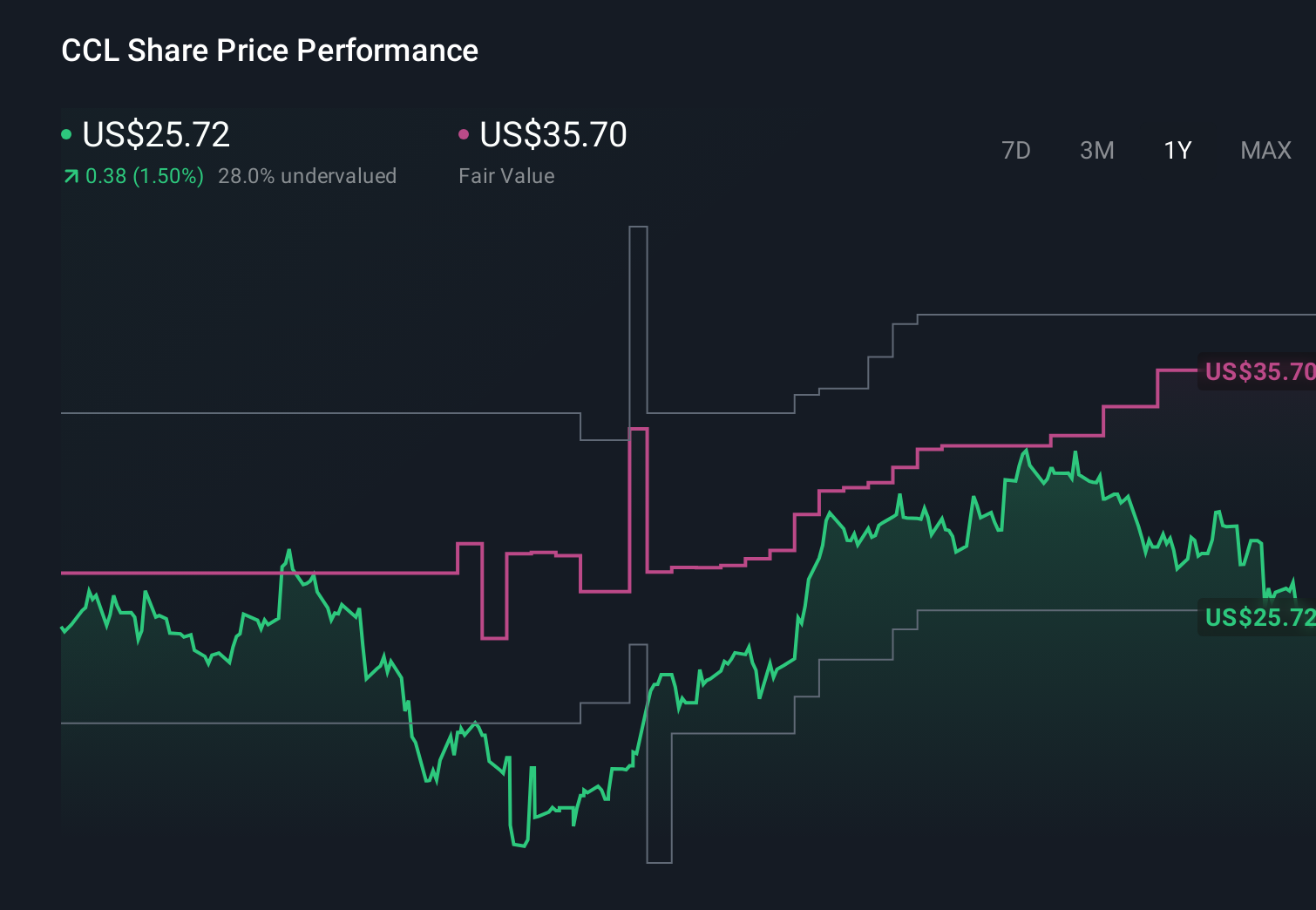

Carnival's narrative projects $30.5 billion revenue and $4.0 billion earnings by 2029. This requires 3.8% yearly revenue growth and an earnings increase of about $0.9 billion from $3.1 billion today.

Uncover how Carnival's forecasts yield a $35.60 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$31.0 billion of revenue and US$4.4 billion of earnings by 2029, but the Ace Class news and ongoing debt concerns show how widely your view of Carnival’s future can differ from theirs.

Explore 10 other fair value estimates on Carnival - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carnival research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival's overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com