- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Enterprise Products Partners (EPD) Stock Looks Reasonable On Earnings While Broader Checks Stay Stretched

After a strong multi year run, Enterprise Products Partners now faces a valuation debate, with a solid 5 year return profile set against a mixed read from its broader valuation checks and an earnings multiple that screens as undervalued.

- Enterprise Products Partners has returned 127.4% over 5 years, which puts sharper focus on whether the current price still offers an attractive entry point.

- For long term valuation, expectations around the durability of its cash generation can support the current share price, while any deterioration in balance sheet strength or funding needs may limit how much investors are willing to pay.

- On Simply Wall St's checks, Enterprise Products Partners is assessed as undervalued in 4 of 6 areas, a mixed picture that points to value support in several metrics but stops short of a clear across the board bargain, as shown by its 4 out of 6 value score.

The issue now is whether Enterprise Products Partners' current valuation still leaves enough upside potential to justify the risk after such a strong multi year return.

Is Enterprise Products Partners a Bargain on Earnings?

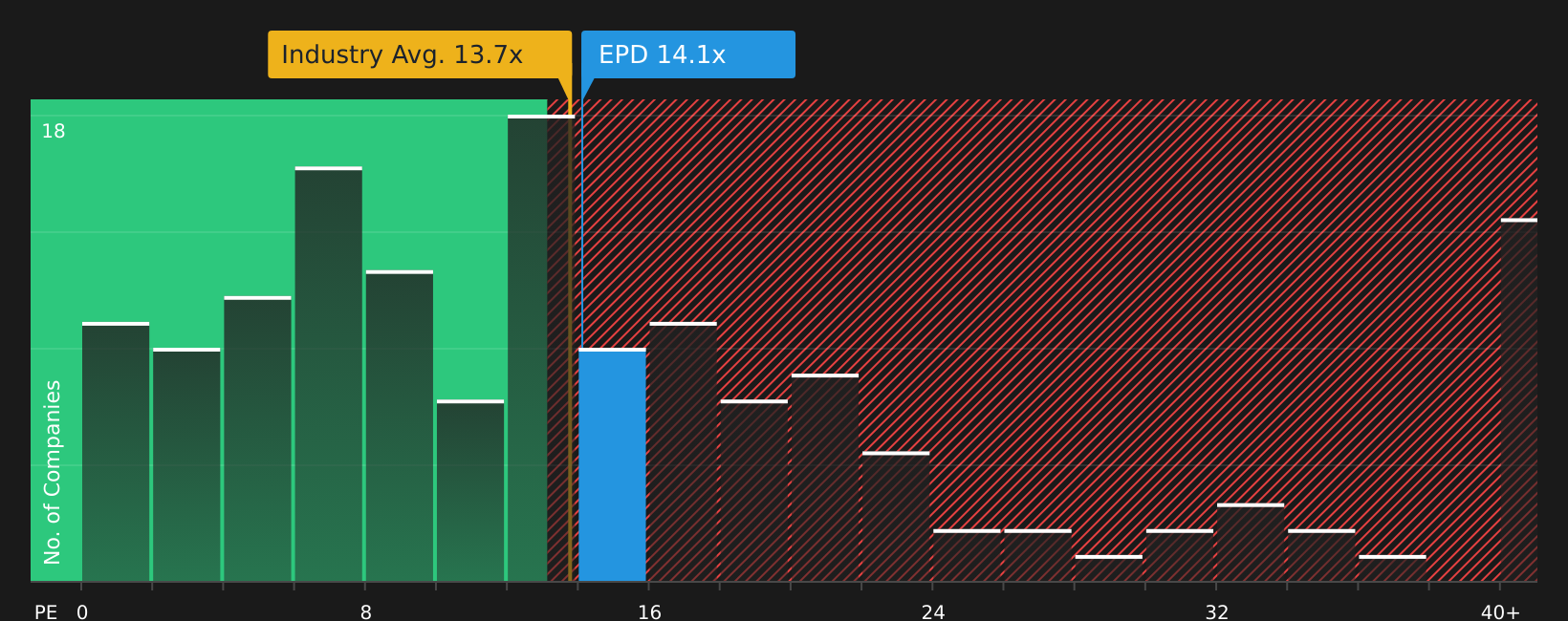

The P/E multiple fits Enterprise Products Partners because earnings are a key anchor for how investors tend to look at established pipeline and midstream businesses. On this measure, the stock currently trades at about 13.9x earnings, which is close to the Oil and Gas industry average of roughly 13.6x. Against the broader peer group, where the average is about 24.8x, Enterprise Products Partners trades at a discount.

The fair P/E ratio for Enterprise Products Partners is estimated at around 23.2x, which reflects what investors might typically pay given its sector, scale and risk profile. Set against the current 13.9x, that is a sizeable gap. This indicates that the market is applying a more cautious earnings multiple than this framework implies.

On a P/E basis, Enterprise Products Partners stock appears undervalued relative to both its tailored fair multiple and wider peer group.

See what the numbers say about this price — find out in our valuation breakdown.

The Enterprise Products Partners Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Enterprise Products Partners are designed to bridge the valuation puzzle above by explaining which future paths for growth, margins and earnings would need to occur for the stock to be worth materially more or less than it is today. Each one treats fair value as a hypothesis about Enterprise Products Partners' business that you can revisit over time, rather than a single static snapshot, and these are available on Simply Wall St's Community page.

If you have a clear, number driven view on where Enterprise Products Partners' growth, margins and execution go from here, this is a chance to add your voice in the Simply Wall St community and set out a narrative others can track over time.

Share your thesis, the key drivers you think matter most, and how that ties back to Enterprise Products Partners' valuation so readers can follow how it plays out as new results arrive.

Do you think there's more to the story for Enterprise Products Partners? Head over to our Community to see what others are saying!

The Bottom Line

For Enterprise Products Partners, the valuation hinges on whether the current P/E discount to peers fairly reflects its risks or offers a margin of safety. The stock screens as undervalued on earnings, but the broader checks are mixed rather than overwhelmingly supportive. That leaves the key question whether investors continue to give weight to its cash generation profile or grow more cautious about balance sheet strength and funding needs. The crux from here is whether that discount proves to be a genuine opportunity or a sign that the market is correctly pricing in those constraints.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com