- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Hancock Whitney Stock And 2 US Bank Shares For Dividend Growth Investors

Dividend growth stocks linked to consumer finance are under fresh scrutiny after reports that policy shifts at the CFPB helped banks collect an extra $22.5b in late and overdraft fees while $4b of consumer relief went missing. For investors, changes like these can influence profitability, political risk, and how steady a dividend stream might feel. This article explains how those CFPB moves relate to dividend growth and highlights 3 stocks from a U.S. Dividend Growth Stocks screener that appear positively exposed to this news so you can decide whether they fit, or do not fit, your own watchlist.

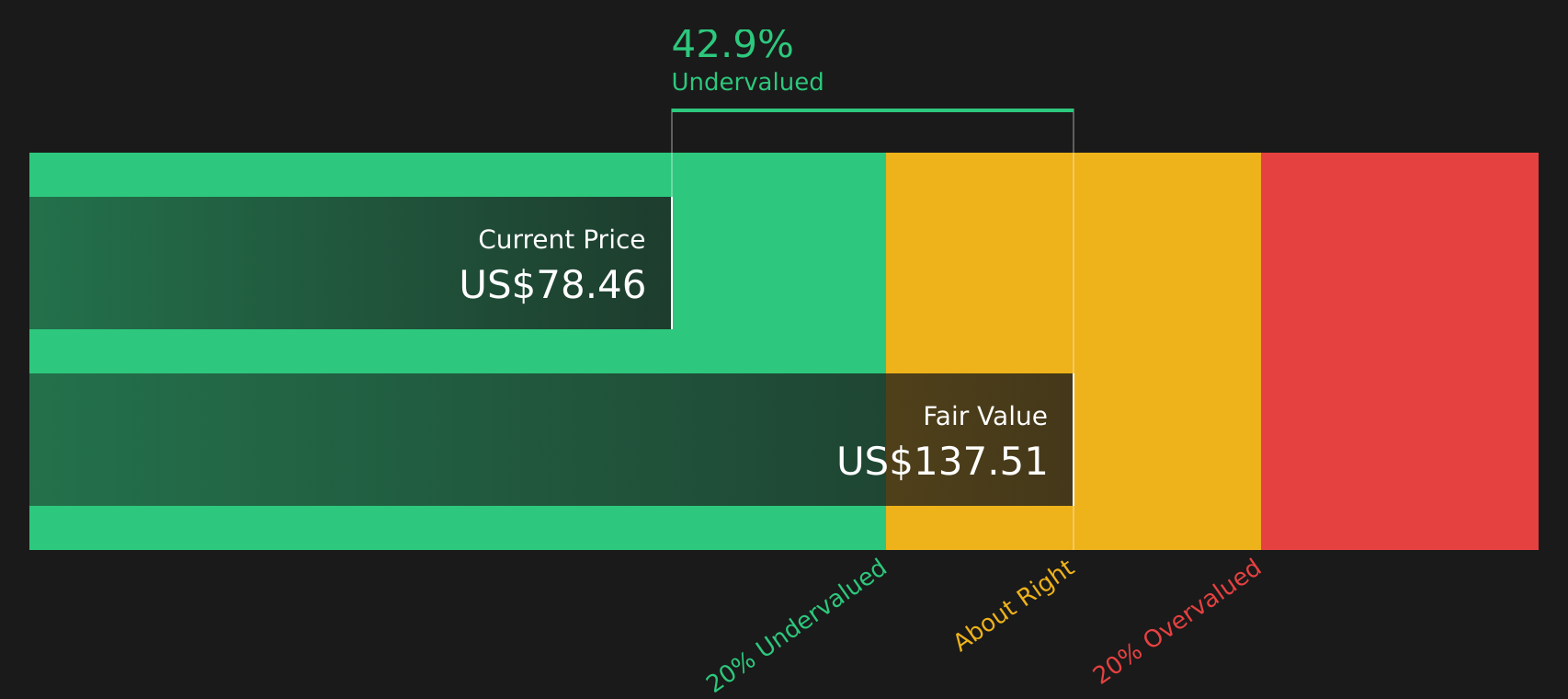

Hancock Whitney (HWC)

Overview: Hancock Whitney is a Gulfport based regional bank that provides traditional and online banking, lending, and wealth management services to commercial, small business, and retail clients across the United States, from everyday deposit accounts and mortgages to corporate credit facilities, trust services, and brokerage products.

Operations: Hancock Whitney generates about US$1.4b in revenue from its core banking operations, all within the United States.

Market Cap: US$6.2b

Hancock Whitney gives you exposure to a U.S. regional bank that is closely tied to the consumer fee story in Washington, yet has already moved to eliminate some NSF and overdraft fees. This may soften political risk while still participating in a friendlier regulatory backdrop. The company combines a 2.6% dividend yield, a history of dividend growth, and active capital returns through buybacks with reported net profit margins, even as earnings over the last year declined and Return on Equity sits in the low double digits. With acquisitions in wealth management, ongoing hiring in growth markets, and a valuation that screens as below an internal DCF estimate, the trade off between income potential and credit or integration risks is where the real opportunity, or caution, lies.

Hancock Whitney’s mix of fee pressure, dividend growth and buybacks raises a clear question: is the market misreading its income story or its risks? Get the full context in the analysis report for Hancock Whitney

West Bancorporation (WTBA)

Overview: West Bancorporation is a West Des Moines based community bank that offers deposits, business and consumer lending, and trust services to individuals and small to medium sized businesses across its Midwest footprint, supported by online and mobile banking tools.

Operations: West Bancorporation generates about US$99.1m in revenue from its community banking operations in the United States.

Market Cap: US$450.7m

West Bancorporation ties the CFPB fee story to a more traditional dividend growth profile, with a long history of regular payouts, a 3.7% yield, and Q1 2026 earnings metrics that show strong net interest income and a net profit margin of 35.6%. The appeal is that this Midwest focused bank combines conservative credit quality, experienced management and a share price that screens below some cash flow based estimates, while also operating within a regulatory backdrop that currently appears more permissive. The trade off is that earnings trends over five years have declined, returns on equity sit around 13%, and geographic concentration plus pockets of distressed commercial real estate keep risk firmly on the table for anyone considering WTBA as a long term dividend compounder.

West Bancorporation’s strong dividend record, 35.6% net profit margin and Midwest footprint could be masking a more interesting valuation story. See how the bank stacks up in the DCF valuation analysis for West Bancorporation.

Norwood Financial (NWFL)

Overview: Norwood Financial is a long established community bank based in Honesdale, Pennsylvania, providing deposits, loans, wealth management, insurance and brokerage services to consumers, businesses, nonprofits and municipalities across Northeastern Pennsylvania and parts of New York. It combines traditional branch banking, ATMs and a full suite of digital services, from mobile deposit to cash management and real estate settlement.

Operations: Norwood Financial generates about US$92.6m in revenue from banking and related financial services in the United States.

Market Cap: US$340.4m

Norwood Financial may appeal to dividend focused investors because it pairs a 4.12% yield and a multi year record of growing payouts with profitability metrics that include a net profit margin of 27.8%, and a P/E below the broader U.S. market. The CFPB fee backdrop and a focus on fee income from wealth management, trust and insurance provide Norwood with more ways to support earnings than spread income alone, while the pending Presence Bank merger and recent securities repositioning highlight strategic initiatives that investors may wish to monitor. At the same time, recent earnings softness, past shareholder dilution and integration risk mean this is a bank to research carefully rather than focus on yield figures alone.

Norwood Financial’s 4.12% yield and 27.8% net profit margin could be masking a more complex story around earnings power and dilution, so the next step is the analysis report for Norwood Financial

The three dividend growth stocks covered here are a useful starting point, but they are only a slice of what the full U.S. Dividend Growth Stocks screener reveals, with 12 more companies that pair income potential with equally compelling narratives across financials, utilities, and consumer staples in the U.S. Dividend Growth Stocks screener. Identify and analyze the specific catalysts, fee sensitivities, and balance sheet traits that matter to you inside Simply Wall St so you can focus on the highest conviction ideas for your own watchlist.

Take Control of Your Investment Journey

If Norwood Financial or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Fresh Dividend Alternatives?

Fresh opportunities can move from quiet to breakout quickly. By the time momentum is strong, the ideal entry point may have passed, so consider getting in early.

- Target resilient income by scanning a curated mix of companies with strong cash positions and low risk scores using the list of solid balance sheet and fundamentals (48 results).

- Spot early momentum in high potential businesses by reviewing a focused group of under the radar for now opportunities via the 20 high quality undiscovered gems.

- Pursue long term compounding by looking for consistent cash generators highlighted in the 78 resilient stocks with low risk scores before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com