- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Aritzia Stock And 2 Undervalued Canadian Shares Worth A Closer Look

Global markets are sending mixed signals, from easing inflation in major economies to shifting trade policies and stubborn energy costs. In this kind of backdrop, investors often look for companies with strong cash generation and solid balance sheets that are not already priced for perfection. That is exactly what the High Quality Undervalued Stocks screener aims to highlight, focusing on businesses the market may be overlooking. In this article, you will see 3 of the best stocks from this screener, showing how quality and value can sit together in a portfolio when conditions are changing quickly across countries and sectors.

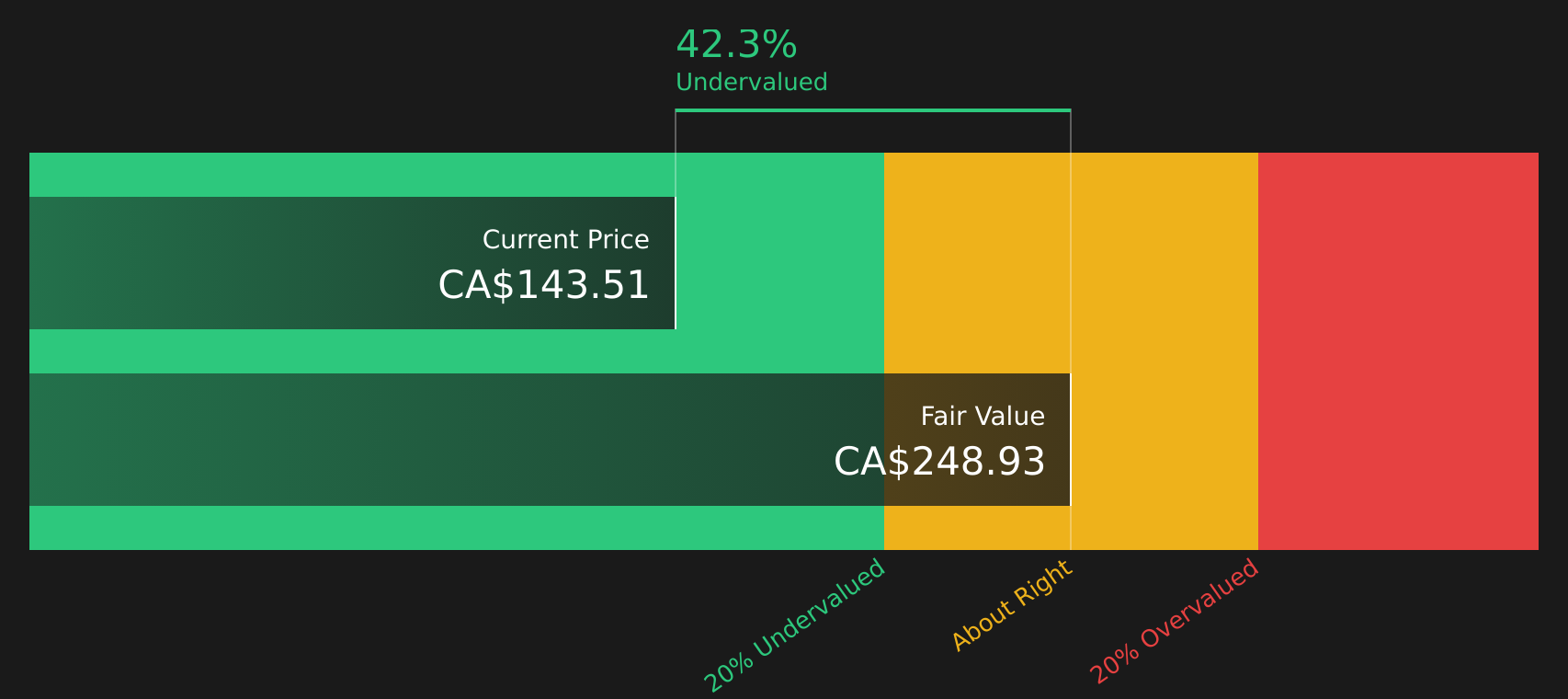

Aritzia (TSX:ATZ)

Overview: Aritzia is a Vancouver based fashion retailer that designs, develops, and sells womens apparel and accessories across its own brands, with products ranging from everyday basics to premium outerwear, sold through its boutiques and online channels in Canada and the United States.

Operations: Aritzia generates all of its CA$4.0b in revenue from apparel, with around CA$2.5b from the United States and CA$1.5b from Canada.

Market Cap: CA$16.8b

Aritzia is on many investors radars because it blends fast growing U.S. expansion and digital sales with profitability metrics that stand out, including an 11.4% net margin and return on equity around 32.3%. The stock is described as trading about 41.1% below estimated fair value, and analysts see further upside. However, the current P/E is higher than many peers, which means execution on new boutiques and a stronger mobile and eCommerce offering really matters. Combined with strong recent revenue and earnings performance, buybacks, and a board that is mostly independent, this creates a quality profile that remains exposed to risks such as insider selling and a funding structure reliant on external borrowing.

Aritzia’s rapid U.S. rollout, online growth and high returns on equity raise a simple question: is the current share price fully reflecting the story or missing key details hiding in the analysis report for Aritzia

Stantec (TSX:STN)

Overview: Stantec is an Edmonton based engineering and professional services company that helps governments and private clients plan, design, and manage infrastructure, buildings, water systems, and environmental projects across Canada, the United States, and global markets.

Operations: Stantec generates about CA$3.5b of revenue in the United States, CA$1.6b in Canada, and CA$1.6b from global markets across its consulting and engineering service lines.

Market Cap: CA$11.0b

Stantec may appeal to investors who like infrastructure exposure backed by a CA$9.0b backlog, recurring consulting work and strong recent earnings growth. Some may also see this as reflected in a valuation that looks restrained against peers and certain analyst fair value estimates. At the same time, the company carries a high level of debt, relies completely on external funding, and faces integration and execution risk from a string of acquisitions just as it prepares for a CEO transition in 2026. For investors weighing whether the current share price is pricing those moving parts correctly, the bigger story sits in how its water, transportation and environmental projects, plus its digital push, relate to long term earnings power and risk.

Stantec’s CA$9.0b backlog and global footprint hint at a bigger earnings story that the market may not be fully pricing in, but the real twist sits inside the 5 key rewards and 1 important warning sign

Avino Silver & Gold Mines (TSX:ASM)

Overview: Avino Silver & Gold Mines is a Vancouver based miner focused on acquiring, exploring, and advancing silver, gold, copper, and base metal deposits in Mexico, anchored by its 100% owned Avino Mine area in Durango and options over additional properties such as Ana Maria and El Laberinto.

Operations: Avino Silver & Gold Mines generates about US$112.8m in revenue from gold and other precious metals mining in Mexico.

Market Cap: CA$1.43b

Investors looking at Avino Silver & Gold Mines are often drawn to its combination of precious metals exposure, strong recent earnings momentum and high net profit margins around 32.7%, supported by sizeable reserves and resources in Mexico that underpin future production plans. Forecast earnings and revenue growth are described as running ahead of the broader Canadian market and industry. Yet the stock is trading at a discount of about 36.4% to one fair value estimate, which raises questions about whether risks such as insider selling, shareholder dilution and reliance on higher risk external funding are weighing too heavily on sentiment. The fuller picture, including how its growth pipeline and governance stack up against these concerns, sits beyond the headline numbers.

Avino Silver & Gold Mines pairs high net margins and described fair value upside with precious metals reserves that many investors may be glossing over, but the real tension between growth and funding risk is unpacked in the analyst forecasts for Avino Silver & Gold Mines

The three stocks in this article are a starting point, and the full High Quality Undervalued Stocks screener surfaces 3 more companies with similarly compelling quality and valuation stories that could round out your watchlist. Use Simply Wall St to identify the specific catalysts, analyze balance sheets and cash flows, and filter narratives so you can focus on the highest conviction opportunities that fit your own approach.

Take Control of Your Investment Journey

If Stantec or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Fresh stock ideas can move from quiet to flying once the crowd catches on, so use this moment while it matters and get in early.

- Spot potential market leaders early by scanning a curated group of resilient companies using the 10 resilient stocks with low risk scores before the spotlight fully turns their way.

- Position ahead of possible sector momentum by reviewing a hand picked mix of infrastructure players in the 34 power grid technology and infrastructure stocks while many are still under the radar for now.

- Explore emerging automation trends by checking companies screened through the 32 robotics and automation stocks before attention shifts and opportunities become more limited.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com