- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Xero Stock And 2 ASX Software Picks Trading Below Fair Value

With inflation, interest rates and energy prices all tugging at market sentiment, it is easy to feel pulled in several directions at once. One way to cut through the noise is to focus on companies where cash flows look promising yet the stock trades below an assessed fair value. That is exactly what the Undervalued Stocks Based On Cash Flows screener aims to highlight. It uses SWS DCF valuation to flag potential mispricing. In this article, you will see 3 stocks from the screener that show this gap, along with clear context to help you assess each opportunity.

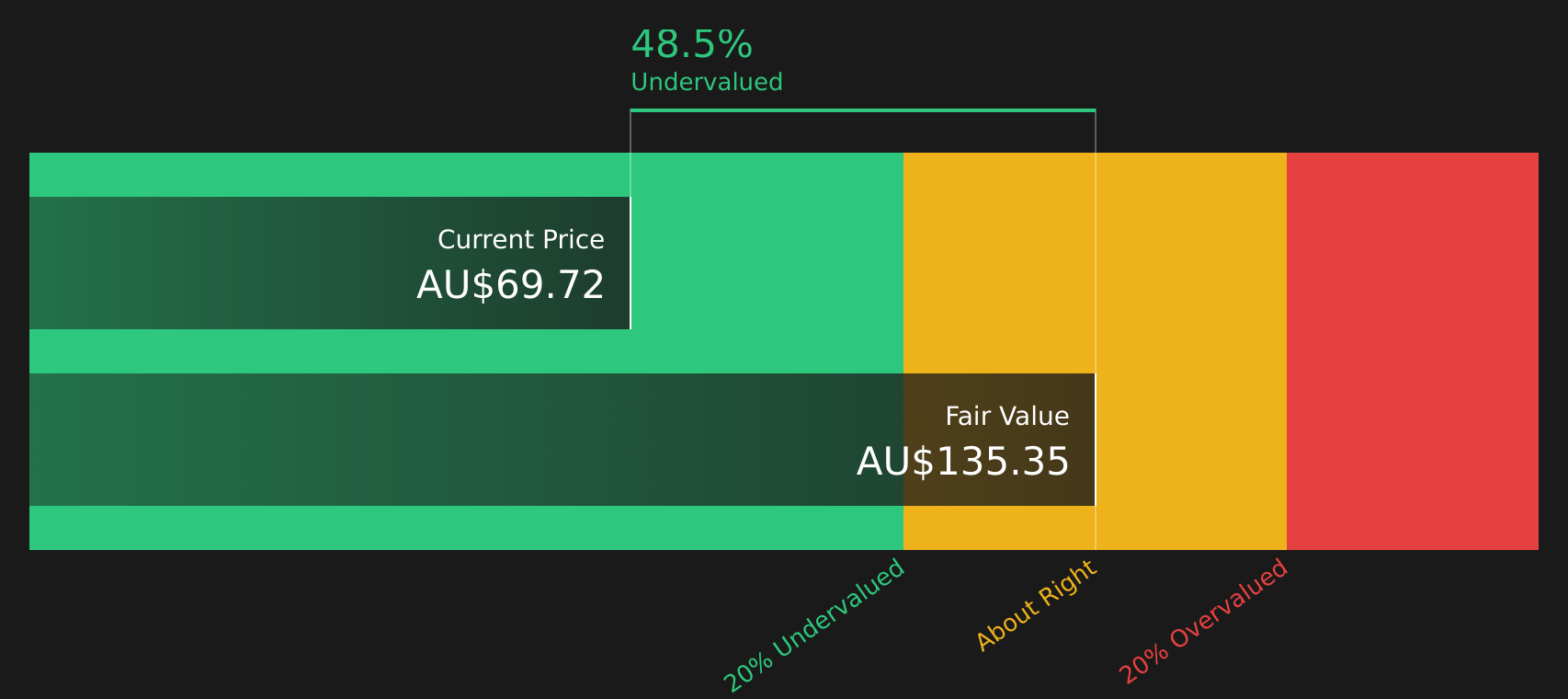

Xero (ASX:XRO)

Overview: Xero is a Wellington based software company that provides cloud accounting, payroll, payments and related tools that help small businesses and their advisors manage finances in one place, supported by add ons like Planday for scheduling, Hubdoc for bill capture and Melio for bill payments.

Operations: Xero generates all of its NZ$2.75b in revenue from providing online solutions for small businesses and their advisors, with key regions including Australia, the United Kingdom, the United States and other international markets.

Market Cap: A$11.65b

Investors looking at Xero get a global small business platform built around cash flow, with NZ$2.75b in revenue and a growing set of AI enabled tools like XeroForce, Melio and real time benchmarking that aim to make its software more central to customers’ daily operations. The company’s premium P/E multiple and net margin of 6.1%, down from 10.8% last year, indicate that the market already expects a lot and that execution risk is real, especially after a year of earnings decline. At the same time, Simply Wall St’s DCF suggests the stock trades well below an assessed fair value, which is why Xero appears in a cash flow based undervaluation screen for investors who are weighing quality, growth potential and funding risk together.

Xero’s premium P/E and shrinking net margin suggest expectations may be colliding with reality. However, the stock still appears undervalued on cash flows, so it is worth seeing how the DCF valuation analysis for Xero could change your view.

Lynas Rare Earths (ASX:LYC)

Overview: Lynas Rare Earths is an Australian company that mines and processes rare earth minerals used in products like electric vehicle motors, wind turbines and electronics, running an integrated chain from the Mt Weld mine in Western Australia through processing facilities in Kalgoorlie and an advanced materials plant in Malaysia.

Operations: Lynas generates A$715.9m in revenue from its rare earth operations, producing a mix of light and heavy rare earth materials for industrial customers.

Market Cap: A$16.59b

Lynas Rare Earths stands out for investors who want exposure to critical materials tied to electrification, with rare earth earnings growing 62% over the past year and net margins at 11.5%, alongside a long term supply and equity deal with JS Link that extends to 2038 and supports downstream magnet production in Malaysia and Korea. At the same time, the stock trades at a discount to analyst assessed fair value, while relying on higher risk external borrowing and carrying a rich P/S multiple that could magnify downside if demand, prices or expansion plans stumble. The combination of growth expectations, current earnings quality and concentrated risks makes Lynas a company some investors may wish to study in more detail.

Lynas Rare Earths sits at the intersection of electrification, rare earth supply and long dated contracts, yet the stock trades below some fair value estimates. Before you decide how that gap should be priced, review the analysis report for Lynas Rare Earths for what the market might be missing.

WiseTech Global (ASX:WTC)

Overview: WiseTech Global is an Australian software company that builds cloud based systems for freight forwarders, customs brokers and other logistics providers so they can manage the movement, storage and documentation of goods across global supply chains from a single platform.

Operations: WiseTech Global generates revenue across major logistics hubs, with about US$450.7m from the Americas, US$254.8m from Asia Pacific and US$364.2m from Europe, the Middle East and Africa.

Market Cap: A$11.43b

WiseTech Global attracts attention because it operates at the center of supply chain software, with a unified, AI enabled SaaS platform, the CargoWise Value Pack model and the E2open acquisition all targeting deeper customer integration and new transaction based revenue. At the same time, margin pressure, a recent one off loss of A$75.6m, higher leverage from a A$3b debt facility and governance concerns around founder Richard White, alongside recent board changes, highlight that execution and integration risks exist. For investors who focus on both cash flow based valuation and quality, the combination of business characteristics, current analyst views and ongoing governance debate may warrant closer consideration of WiseTech.

WiseTech Global’s freight software story is accelerating, but the real tension is how its acquisition, debt facility and governance questions fit together, so the full narrative for WiseTech Global might surprise you

The 3 stocks in this article are just a sample of the opportunities flagged by Simply Wall St. The full Undervalued Stocks Based On Cash Flows screen surfaces 34 more companies that pair cash flow potential with apparent discounts to fair value through the Undervalued Stocks Based On Cash Flows screener. Identify and analyze the catalysts that matter most to you, from cash flow resilience to funding risk and business quality filters, so you can focus on the ideas that best match your objectives inside Simply Wall St.

Take Control of Your Investment Journey

If Xero or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Picks?

Fresh stock ideas can move from quiet to breakout fast, and once momentum is flying you are either caught in or left watching. Consider these while it matters and review them in a timely way.

- Spot sturdy companies that aim to ride volatility with resilient balance sheets by scanning the curated list of solid balance sheet and fundamentals (20 results).

- Explore payout opportunities that could support your income goals by checking the hand picked 6 dividend fortresses before yields change or attention surges.

- Search for future facing AI platforms that already produce profits, not just promises, by reviewing the focused 63 profitable AI stocks that aren't just burning cash list.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com