- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 Stocks Estimated To Be Trading At Up To 36.9% Below Intrinsic Value

In the last week, the United States market has been flat, yet it has seen a 21% increase over the past year with earnings forecasted to grow by 18% annually. In this context of growth and stability, identifying stocks trading below their intrinsic value can present potential opportunities for investors looking to capitalize on undervalued assets.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Western Digital (WDC) | $513.84 | $1013.34 | 49.3% |

| Rayonier (RYN) | $21.81 | $43.20 | 49.5% |

| Q2 Holdings (QTWO) | $52.62 | $103.54 | 49.2% |

| Natera (NTRA) | $277.37 | $551.71 | 49.7% |

| Dime Commercial Bancshares (DCOM) | $40.45 | $80.68 | 49.9% |

| ConnectOne Bancorp (CNOB) | $33.02 | $65.10 | 49.3% |

| Betterware de MéxicoP.I. de (BWMX) | $18.09 | $36.11 | 49.9% |

| Beacon Financial (BBT) | $30.28 | $59.46 | 49.1% |

| Amaroq (AMRQ.F) | $1.13 | $2.25 | 49.7% |

| AAON (AAON) | $113.11 | $221.51 | 48.9% |

We'll examine a selection from our screener results.

Flywire (FLYW)

Overview: Flywire Corporation operates as a payment enablement and software company across the United States, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of approximately $2.14 billion.

Operations: The company's revenue segment consists of Data Processing, which generated $677.68 million.

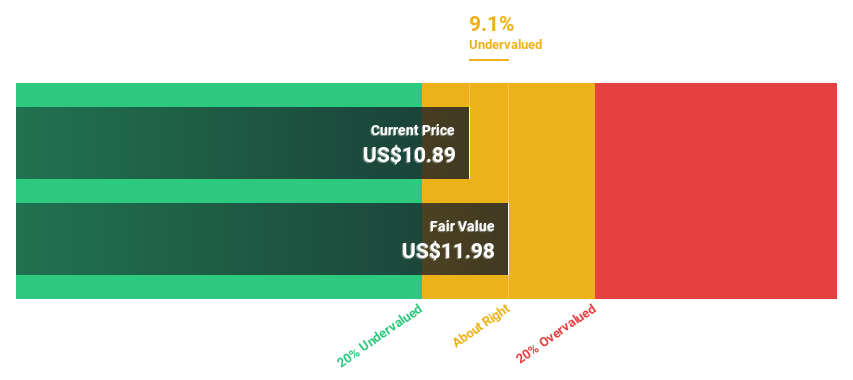

Estimated Discount To Fair Value: 14.5%

Flywire is trading at US$18.78, slightly below its estimated future cash flow value of US$21.96, indicating potential undervaluation based on cash flows. The company has demonstrated substantial earnings growth, with a significant increase over the past year and forecasted annual profit growth of 41.9%, outpacing the broader U.S. market's expected growth rate. Recent additions to multiple Russell 2000 indices highlight Flywire's defensive and growth attributes amidst expanding partnerships in sectors like hospitality and education to enhance payment efficiencies and reduce costs.

- The analysis detailed in our Flywire growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of Flywire.

Lumentum Holdings (LITE)

Overview: Lumentum Holdings Inc. is a company that manufactures and sells optical and photonic products across various regions including the Americas, Asia-Pacific, Europe, the Middle East, and Africa, with a market cap of approximately $6.34 billion.

Operations: Lumentum Holdings Inc. generates revenue through the sale of optical and photonic products across diverse geographical regions such as the Americas, Asia-Pacific, Europe, the Middle East, and Africa.

Estimated Discount To Fair Value: 27.4%

Lumentum Holdings is trading at US$752, below its estimated future cash flow value of US$1,036.01, reflecting potential undervaluation based on cash flows. The company has become profitable this year with earnings expected to grow significantly at 56.3% annually, surpassing market averages. Despite recent index exclusions and insider selling concerns, Lumentum's revenue growth forecast of 42.7% annually indicates robust future prospects in the U.S. market context.

- In light of our recent growth report, it seems possible that Lumentum Holdings' financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of Lumentum Holdings stock in this financial health report.

Estée Lauder Companies (EL)

Overview: The Estée Lauder Companies Inc. is a global manufacturer and marketer of skincare, makeup, fragrance, and hair care products with a market cap of approximately $29.25 billion.

Operations: The company's revenue is primarily derived from skin care products at $7.19 billion, followed by makeup at $4.25 billion, fragrance at $2.72 billion, and hair care products contributing $566 million.

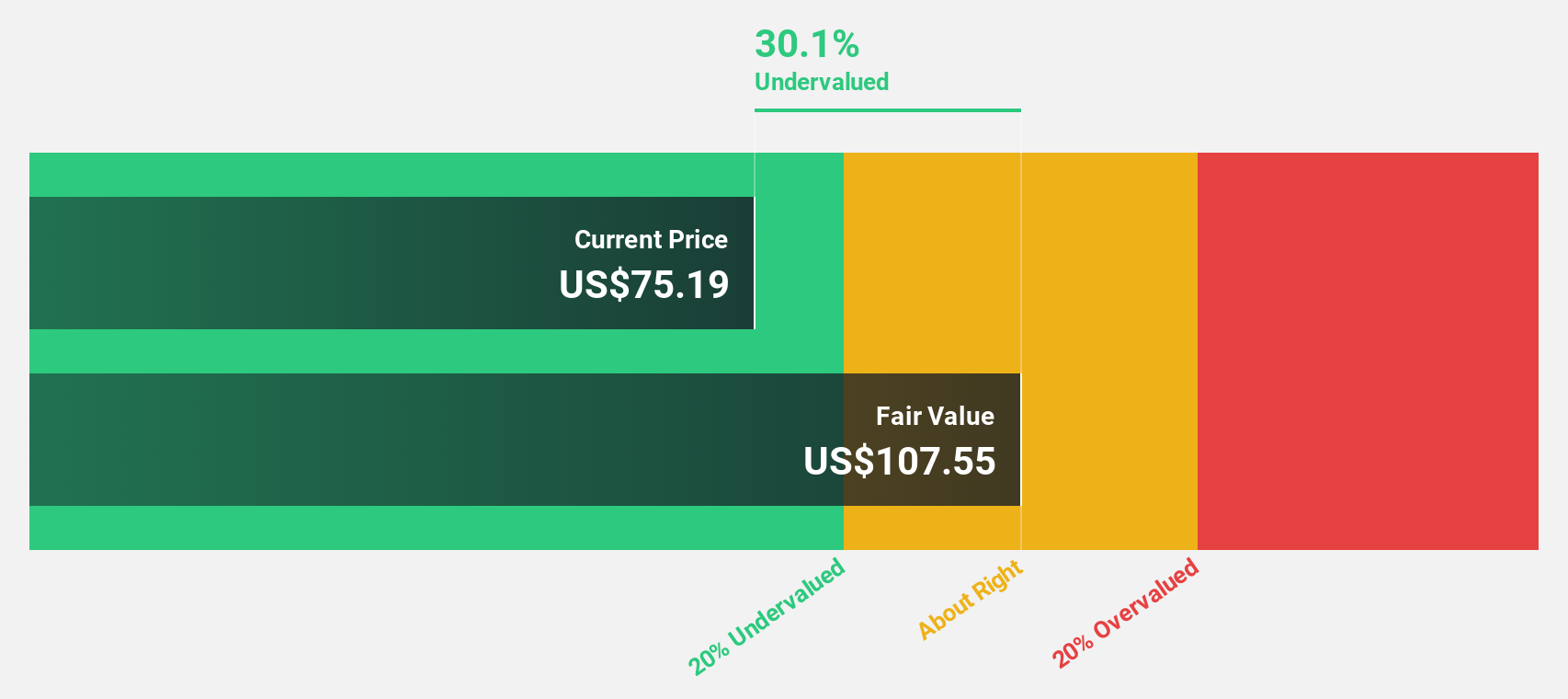

Estimated Discount To Fair Value: 36.9%

Estée Lauder Companies is trading at US$82.31, significantly below its estimated future cash flow value of US$130.49, suggesting undervaluation based on cash flows. Despite high debt levels and a dividend not fully covered by earnings, the company is expected to become profitable within three years with annual profit growth forecasted at 34.38%. Recent inclusion in several Russell indices could enhance visibility, although revenue growth lags behind broader market expectations.

- According our earnings growth report, there's an indication that Estée Lauder Companies might be ready to expand.

- Get an in-depth perspective on Estée Lauder Companies' balance sheet by reading our health report here.

Make It Happen

- Click here to access our complete index of 149 Undervalued US Stocks Based On Cash Flows.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com