- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Toyota Stock, SoftBank And More Dividend Income Ideas From Japan

With inflation trends and interest rate policies pulling markets in different directions, many investors are looking for steadier sources of potential return and income. That is where high quality dividend stocks from the Dividend Powerhouses (3%+ Yield) screener can help. This screener focuses on companies with dividend yields above 5% that are described as well covered, growing and stable. Instead of trying to second guess every central bank move or commodity price shift, you can focus on businesses that pay you to hold their stock. In this article, you will see 3 of the best stocks highlighted from this screener.

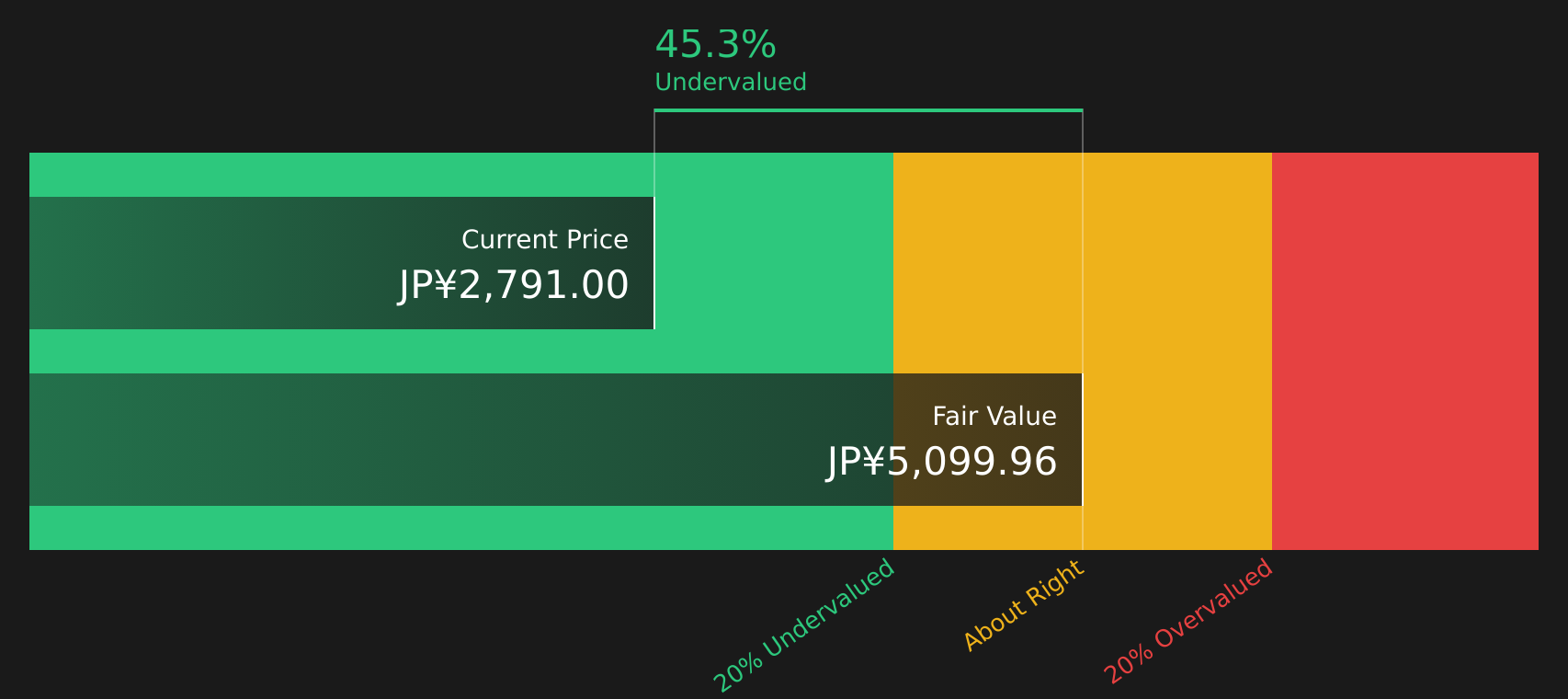

Daiichi Sankyo Company (TSE:4568)

Overview: Daiichi Sankyo Company is a global pharmaceutical group headquartered in Japan, focused on cancer, cardiovascular and metabolic diseases, and vaccines, with a portfolio that includes targeted oncology drugs like Enhertu and Datroway as well as treatments for diabetes, osteoporosis and migraines.

Operations: Daiichi Sankyo Company generates about ¥2.1t in revenue from its Pharmaceutical Operation, with sales spread across Japan (¥580.1b), the United States (¥749.4b), Europe (¥497.4b) and other regions (¥296.2b).

Market Cap: ¥4.8t

Daiichi Sankyo Company stands out in the Dividend Powerhouses screener because its 3.65% yield is paired with a fast evolving oncology franchise built around Enhertu and Datroway, supported by global approvals and reimbursement decisions across the US, EU, China and other key markets. The stock is flagged as trading well below some fair value estimates, which may appeal to valuation focused investors. At the same time, heavy dependence on a few blockbuster drugs, rising R&D spend, and dividend coverage that is not supported by free cash flow all point to risk factors that need careful attention.

Daiichi Sankyo Company’s fast evolving oncology franchise and flagged valuation gap could be telling two very different stories about the same stock, and the real tension sits inside the 2 key rewards and 2 important warning signs (1 is major!)

Toyota Motor (TSE:7203)

Overview: Toyota Motor is a global auto group headquartered in Japan that designs, builds and sells a full range of vehicles, from compact cars and pickup trucks to buses and premium Lexus models, while also offering financial services like auto loans, leasing and insurance.

Operations: Toyota Motor generates about ¥45.4t from Automotive, ¥4.9t from Financial Services and ¥1.7t from All Other activities, with some internal eliminations reducing the consolidated total.

Market Cap: ¥34.0t

Toyota Motor appears in a dividend focused screen because investors are getting exposure to one of the largest global automakers, a 3.43% dividend yield, and a business investing heavily in electrified vehicles, internal battery production and US manufacturing, including a ¥3.6b expansion of its Texas plant. At the same time, earnings fell in the last year, margins slipped from 9.9% to 7.6%, cash flow coverage of the dividend is weak, and production issues, recalls and currency swings add uncertainty. The company’s P/E sits below both the Japanese market and Asian auto peers, and analysts currently expect upside from recent prices. However, the relationship between its electrification strategy, US reshoring efforts and capital intensity is more complex than headline valuation metrics alone might indicate.

Toyota Motor’s lower P/E, 3.43% yield and substantial push into electrified vehicles and US manufacturing suggest a story investors may be misreading, and the real twist sits inside the 4 key rewards and 2 important warning signs (1 is major!)

SoftBank (TSE:9434)

Overview: SoftBank is a Japanese telecom and technology services company that provides mobile and fixed-line connectivity, broadband, cloud and data center services, plus digital platforms in media, e-commerce and financial services such as QR payments, credit cards and banking.

Operations: SoftBank generates roughly ¥3.0t from Consumer services, ¥1.7t from Media & EC, ¥1.1t from Enterprise, ¥1.1t from Distribution, and ¥0.4t from Financial services, with total revenue of about ¥7.0t almost entirely from Japan.

Market Cap: ¥10.5t

SoftBank may interest dividend focused investors because it combines a large domestic telecom base with exposure to AI, digital payments and cloud infrastructure, supported by partnerships around GPUs, data centers and fintech platforms such as PayPay. Reported expectations of earnings growth of around 7% a year, high earnings quality and a share price that is indicated as below some fair value estimates contribute to the appeal, particularly if AI and data services keep gaining traction. However, a debt heavy balance sheet, an above industry P/E and a relatively less experienced management team mean the investment case rests on confidence that capital intensive AI and data center projects can be executed without putting undue pressure on margins or dividend resilience.

SoftBank’s AI and data center push could be masking a much bigger shift in where its value really sits, and the 3 key rewards and 1 important warning sign might be the key to what most investors are missing

The three dividend stocks highlighted here are only a small sample of what is available, as the full Dividend Powerhouses (3%+ Yield) screen uncovers 469 more companies with yields above 5% and equally detailed stories behind their income potential. To identify and analyze the highest conviction dividend ideas that match the catalysts and narratives discussed here, unlock the full Dividend Powerhouses (3%+ Yield) screener.

Take Control of Your Investment Journey

If Daiichi Sankyo Company or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Dividends?

Some of the most interesting ideas move from quiet to breakout before the crowd catches on. Scan these fresh stock groups while it matters and get in early.

- Spot companies quietly building momentum in tough conditions by running a quick pass over a curated list of solid balance sheet and fundamentals (37 results) that can better shoulder shocks than weaker peers.

- Hunt for resilient compounding opportunities with growing payouts by scanning a focused 53 resilient stocks with low risk scores that filters for steadier balance sheets and lower overall risk profiles.

- Review a curated 34 power grid technology and infrastructure stocks focused on infrastructure and power-grid related names as you evaluate potential exposure to grid upgrades and electrification trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com