- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Cui Dongshu: Automobile consumption of 1968.8 billion yuan in the first half of the year fell 13% year on year, and the penetration rate of new energy reached 49%

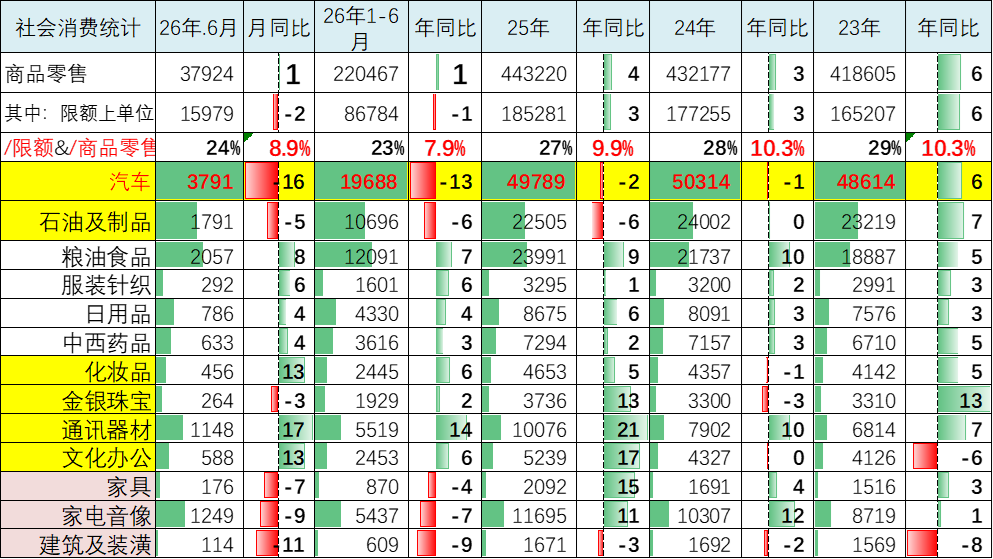

The Zhitong Finance App learned that on July 16, Cui Dongshu, Secretary General of the China Federation Branch, published an article stating that in 2026, the country will implement more active and promising macroeconomic policies, increase countercyclical and cross-cycle adjustments, continue to expand domestic demand and optimize supply. Overall market demand is rising steadily, and a good start has been achieved. In the first half of 2026, total retail sales of consumer goods amounted to 24872.2 billion yuan, an increase of 1.3% over the previous year. Among them, automobile consumption was 1968.8 billion yuan, a year-on-year decrease of 13%; retail sales of consumer goods other than automobiles were 22903.4 billion yuan, an increase of 2.8%.

In June, total retail sales of consumer goods amounted to 4269.1 billion yuan, an increase of 1.0% over the previous year. Among them, automobile consumption was 379.1 billion yuan, a year-on-year decrease of 16%; retail sales of consumer goods other than automobiles were 3890 billion yuan, an increase of 3.0%.

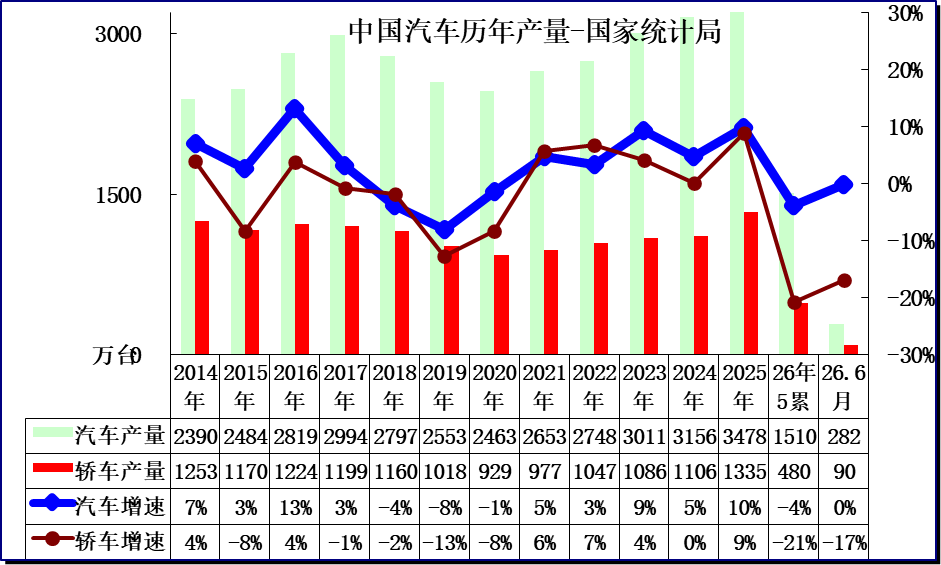

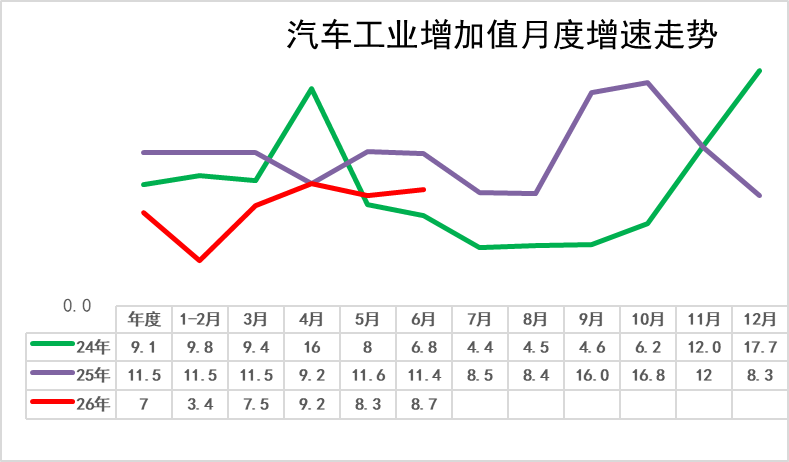

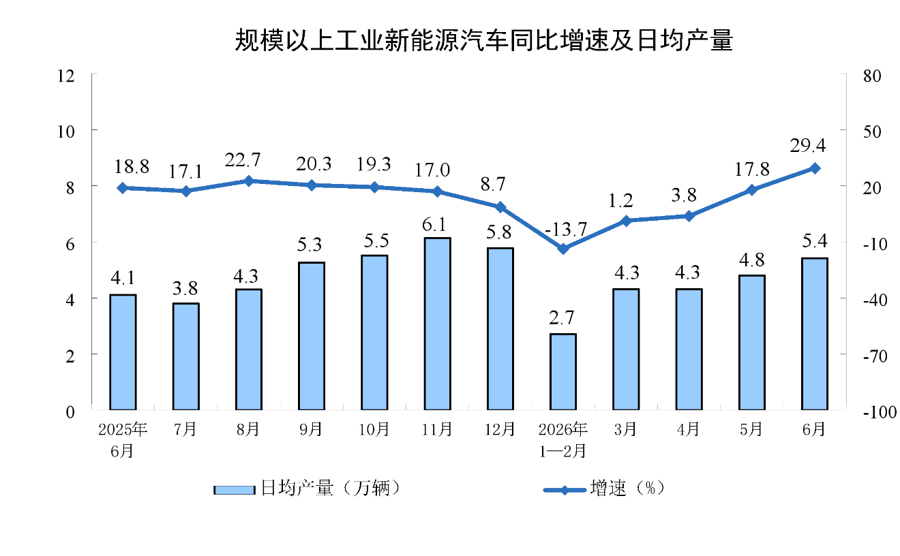

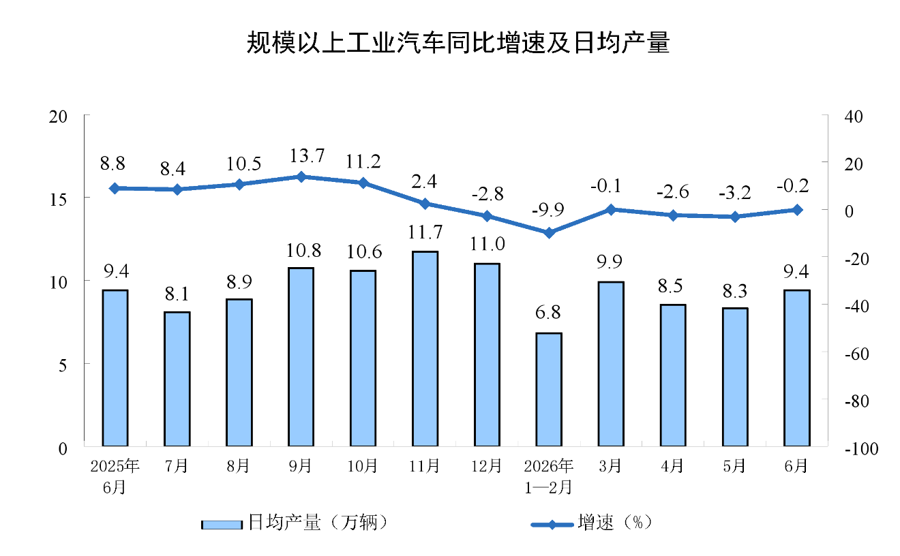

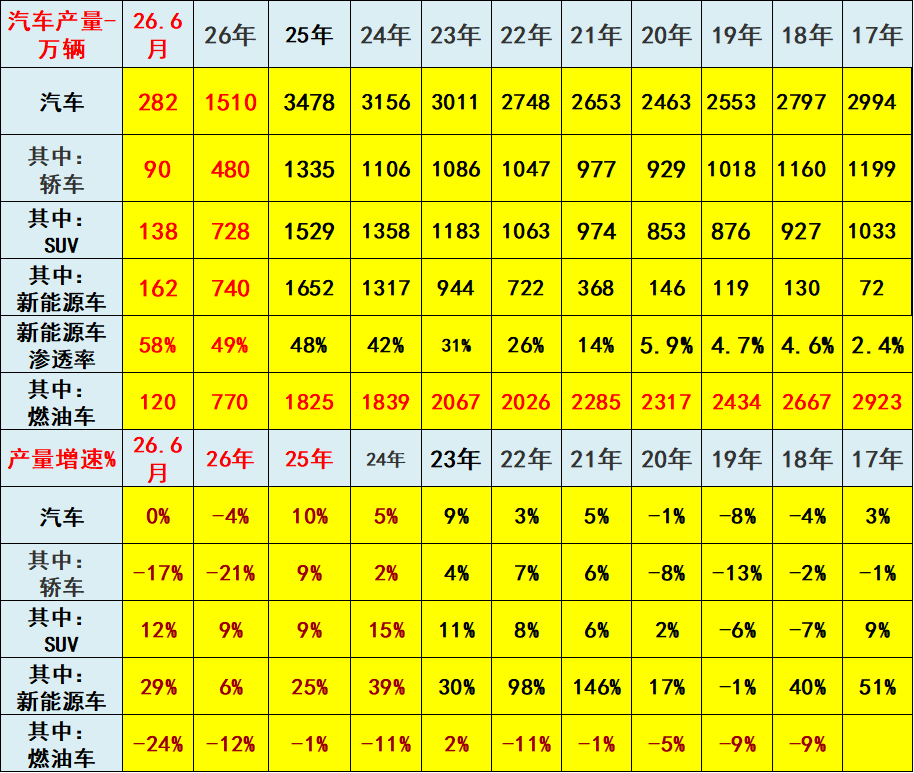

In June, the value added of industries above scale actually increased by 5.3% year on year. From January to June, the value added of industries above scale increased by 5.4% year on year. The value added of the automobile industry increased by 7% from January to June 2026. Among them, the value added of the automobile industry increased by 8.7% in June, and the automobile industry's production performance was strong. From January to June 2026, automobile production was 15.1 million units, down 4% year on year; new energy vehicle production was 7.4 million units, up 6% year on year, penetration rate 49%; fuel vehicle production was 7.7 million units, down 12% year on year. In June 2026, automobile production was 2.82 million units, down 0% year on year; new energy vehicle production was 1.62 million units, up 29% year on year, penetration rate 58%; fuel vehicle production was 1.2 million units, down 24% year on year.

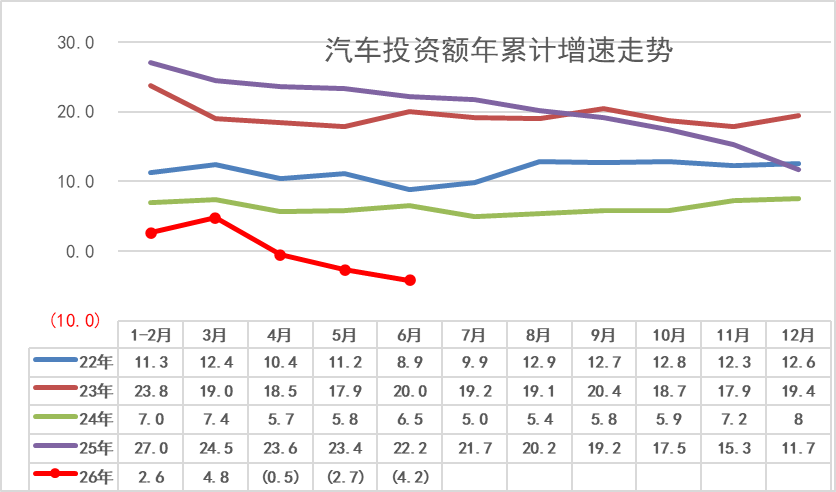

From January to June 2026, fixed asset investment in the automotive industry fell 4.2% year on year, and is still above the 5.7% average of all industries. Recently, investment pressure has been high in the tertiary sector. In particular, investment in public infrastructure, education, culture, and health has declined sharply.

Currently, the external environment is becoming more complex and severe. The situation in the Gulf is complicated, and high oil prices impact the stability of the industrial chain supply chain and consumer demand; the foundation for domestic economic recovery is not stable, prices are high, spending on clothing and food has skyrocketed, problems such as insufficient effective demand, and lack of market vitality, and the task of steady industry growth is still arduous.

Since the 2026 trade-in passenger car subsidies were far less strong than commercial vehicles, commercial vehicle subsidies contributed particularly well to the growth of NEV retail sales, and NEV passenger vehicles plummeted. Currently, there is a lot of pressure on passenger car consumption. It is expected that there will be a long-term strong continuation policy in the future, reducing personal taxes for car buyers, promoting new energy vehicles going to the countryside, setting standards for economical electric vehicles, optimizing C7 economy electric vehicle driver license applications, greater tax concessions for compliant pure electric vehicles with a battery life of less than 200 kilometers, and encouraging marriage and childbearing car purchases to boost economic growth.

1. Automobile consumption declined relatively steadily

Since the decline in the property market in 2021, automobile consumption has risen from 3.94 trillion yuan in 2020 to 5.03 trillion yuan in 2024, breaking away from the passive situation of hovering around 3.9 trillion yuan for 3 consecutive years in 2018-2020. Since the decline in real estate favors consumption, the problem of investment squeezing consumption has improved. Currently, the problem of poor consumption has improved slightly.

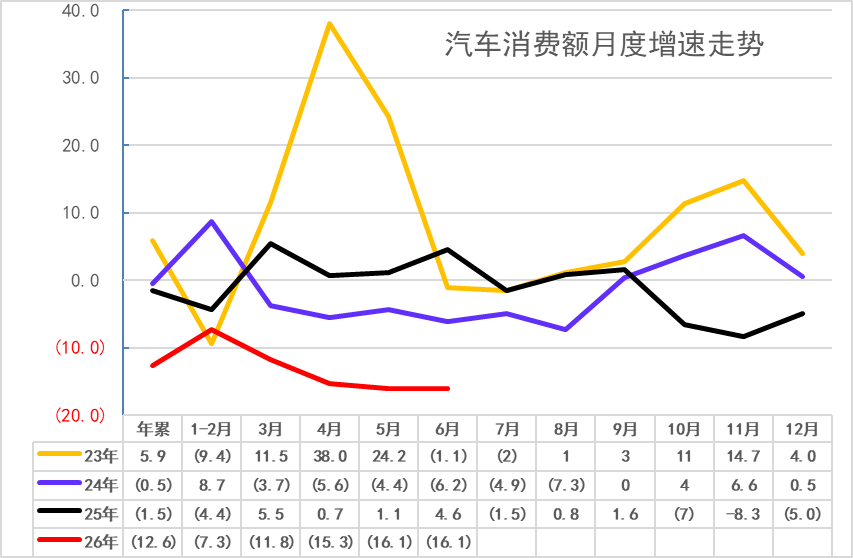

From January to June 2026, automobile consumption fell 12.6% year on year, and automobile consumption fell 16.1% year on year in June. After the base figure continued to rise, this year's decline was significant. The high base pressure was greatest in March and June 2025. Under base pressure in June, automobile retail remained stable month-on-month, and the impact of high oil prices on consumption improved.

2. Automobile production started low in 2026

By product, in June, the output of 314 products out of 626 products in large-scale industries increased year-on-year. Among them, there were 2,824 million vehicles, a decrease of 0.2%, including 1.624 million new energy vehicles, an increase of 29.4%; the power generation capacity was 827.6 billion kilowatt-hours, an increase of 2.0%.

3. Automobile value added performed well in 2026

The value added of the automobile industry increased by 6.6% in 2020; the growth rate hovered at the level of 5.5% in 2021; the value added value of automobiles in 2022 was 6.3%, which was strong; the value added of the automobile industry increased by 13% in 2023, achieving super growth; the value added of 9.1% of automobiles increased relatively well in 2024; and the value added of the automobile industry increased by 11.5% in 2025.

In June, the value added of industries above scale actually increased by 5.3% year on year. From January to June, the value added of industries above scale increased by 5.4% year on year. The value added of the automobile industry increased by 7% from January to June 2026. Among them, the value added of the automobile industry increased by 8.7% in June, and the automobile industry's production performance was strong.

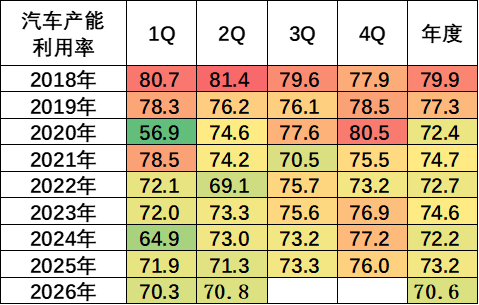

4. The utilization rate of automobile production capacity is relatively stable

In the fourth quarter of 2024, the utilization rate of industrial capacity above the national scale was 76.2%, up 0.3 percentage points from the same period last year, and 1.1 percentage points higher than in the third quarter. In 2025, the utilization rate of industrial capacity above the national scale was 74.4%. Looking at major industries, the capacity utilization rate of the automobile industry remained within a small fluctuation range of 72.4 to 74.6 in 2020-2024. In 2025, the automobile industry's capacity utilization rate was 73.2%, which is relatively low.

In the first quarter of 2026, the utilization rate of industrial capacity above the national scale was 73.6%, down 1.3 percentage points from the fourth quarter of the previous year, down 0.5 percentage points from the same period of the previous year; in the second quarter of 2026, the capacity utilization rate of industries above the national scale was 73.0%, down 0.6 percentage points from the first quarter and 1.0 percentage point from the same period last year. In the first quarter of 2026, the automobile industry's capacity utilization rate was 70.3%, down 1.6 percentage points from last year; in the second quarter of 2026, the automobile industry's capacity utilization rate was 70.8%, down 0.5 percentage points from last year.

5. The specific situation of automobile production

The average daily production of new energy vehicles in June 2026 was 54,000, an increase of 29.4% over the previous year. Due to the high base of new energy cars last year, production fluctuated greatly this year. Production in the first half of 2025 was better for small and micro electric vehicles. Demand is also strong in the middle and low end, so the sales growth rate is slightly lower than the sales growth rate. The sharp reduction in subsidies this year had a big impact, but commercial vehicle subsidies were high, and the market skyrocketed.

By product, in June 2026, the average number of cars per day was 94,000, a decrease of 0.2%. Considering the increase in the base figure from January to June 2025 and the contraction of policy subsidies in 2026, the growth rate from January to June this year was weak.

In 2022, automobile production was 27.48 million units, with a year-on-year increase of 3%; production of new energy vehicles was 7.22 million, an increase of 98%, with a penetration rate of 26%; production of fuel vehicles was 2.06 million units, a decrease of 11%.

In 2023, automobile production was 30.11 million units, up 9% year on year; new energy vehicle production was 9.44 million units, up 30% year on year, penetration rate 31%; fuel vehicle production was 20.67 million units, up 2% year on year.

In 2024, automobile production was 31.56 million units, up 5% year on year; new energy vehicle production was 13.17 million units, up 39% year on year, penetration rate 42%; fuel vehicle production was 18.39 million units, down 11%.

In 2025, automobile production was 34.78 million units, up 10% year on year; new energy vehicle production was 16.52 million units, up 25% year on year, penetration rate 48%; fuel vehicle production was 18.25 million units, down 1% year on year.

From January to June 2026, automobile production was 15.1 million units, down 4% year on year; new energy vehicle production was 7.4 million units, up 6% year on year, penetration rate 49%; fuel vehicle production was 7.7 million units, down 12% year on year.

In June 2026, automobile production was 2.82 million units, down 0% year on year; new energy vehicle production was 1.62 million units, up 29% year on year, penetration rate 58%; fuel vehicle production was 1.2 million units, down 24% year on year.

6. Auto investment falls slightly in 2026

From January to June, the country's fixed asset investment (excluding rural households) was 22637 billion yuan, a year-on-year decrease of 5.7%. Investment pressure is high in the tertiary sector, where investment in public infrastructure, education, culture, and health has declined sharply.

From January to June 2026, fixed asset investment in the automotive industry fell 4.2% year on year, and is still above the 5.7% average of all industries.

7. The real estate consumption squeeze has improved slightly

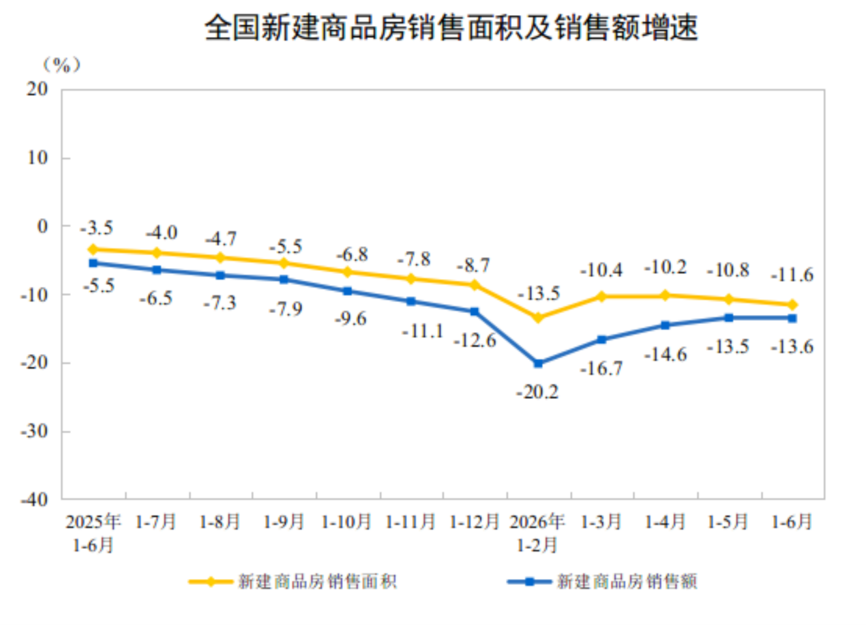

From January to June, the sales area of newly built commercial housing was 401.4 million square meters, a year-on-year decrease of 11.6%, of which the residential sales area decreased by 12.4%. Sales of newly built commercial housing reached 3794.5 billion yuan, a decrease of 13.6%, of which residential sales fell 13.7%.

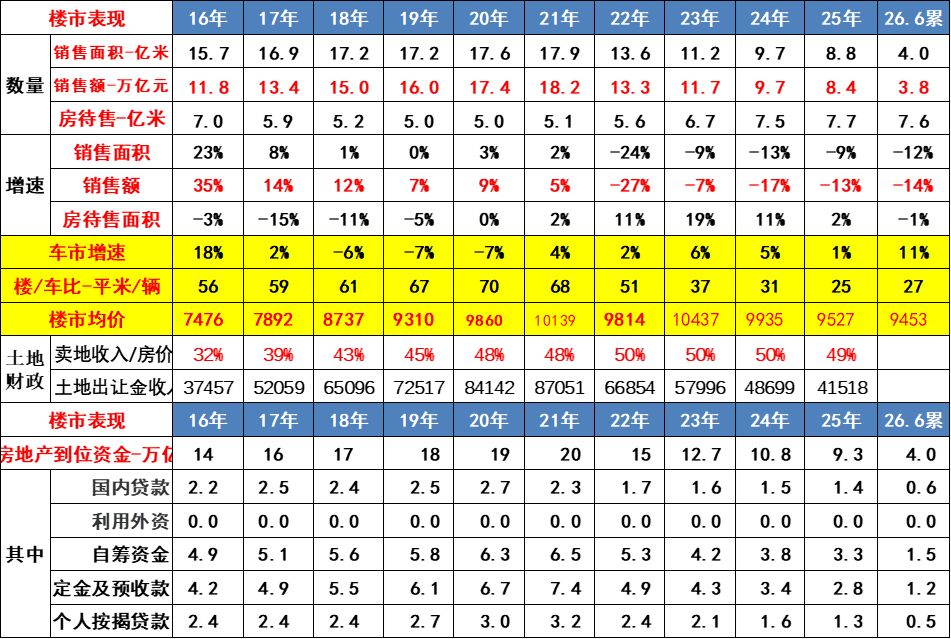

Land concession revenue in 2021 was 8705.1 billion yuan, accounting for 48% of real estate sales; in 2023, land concession revenue was 579.6 billion yuan, accounting for 50% of real estate sales; in 2024, land concession revenue was 4869.9 billion yuan, accounting for 50% of house sales revenue, and real estate contributed greatly to local finance. The 2025 land sales revenue data still accounts for 49% of housing prices.

Currently, the relationship between automobile sales and real estate sales from January to June 2026 is a 27-square-meter house/1 vehicle, and the unreasonable comparison of sales has improved. Although motorhomes have improved compared to the 70-square-meter house/1 car at their peak in 2020, the pressure on debt in the early period and the pressure on the current 10,000 yuan property market are still squeezing consumption, causing demand in the car market to be sluggish due to debt pressure.

The wealth effect of the property market has had a certain effect on boosting demand for high-end cars. The recent decline in residents' property market debt pressure and weakening demand for home purchases have also brought certain potential benefits to improving car market consumption.

8. Car market consumption requires continuous policy support

Since the decline in the property market in 2021, automobile consumption has risen from 3.94 trillion yuan in 2020 to 4.98 trillion yuan in 2025, breaking away from the passive situation of hovering around 3.9 trillion yuan for 3 consecutive years in 2018-2020. As the decline in real estate favors consumption, the problem of investment in buying a house squeezes consumption has improved. In 2025, total retail sales of consumer goods amounted to 5012.2 billion yuan, an increase of 3.7% over the previous year. Among them, automobile consumption was 4978.9 billion yuan, down 2% year on year; retail sales of consumer goods other than automobiles were 45141.3 billion yuan, an increase of 4.4%.

The cost of living has risen sharply, consumption of clothing and food is growing too fast, and consumption of car purchases is being seriously squeezed by food and clothing. Automobile market consumption fell 13% from January to June 2026. Currently, the problem of poor consumption still needs to be improved.

In the first half of 2026, total retail sales of consumer goods amounted to 24872.2 billion yuan, an increase of 1.3% over the previous year. Among them, automobile consumption was 1968.8 billion yuan, a year-on-year decrease of 13%; retail sales of consumer goods other than automobiles were 22903.4 billion yuan, an increase of 2.8%. In June, total retail sales of consumer goods amounted to 4269.1 billion yuan, an increase of 1.0% over the previous year. Among them, automobile consumption was 379.1 billion yuan, a year-on-year decrease of 16%; retail sales of consumer goods other than automobiles were 3890 billion yuan, an increase of 3.0%.

Automobile consumption in the first half of 2026 presented a complex situation of “policy continuation, market fragmentation, and pressure on demand”. The trade-in policy continues to gain strength, but due to factors such as the accelerated contraction of fuel vehicles, price wars diluting consumer confidence, and the downturn in the low-end market, the total retail volume is still declining. The steady increase in consumption of petroleum products reflects the fact that residents' demand for travel is still rigid, and weak automobile consumption is more indicative of a marginal weakening of the will to spend on durable goods and disposable income.