- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Undervalued Small Caps In Global With Insider Buying

In recent weeks, global markets have experienced mixed performances with geopolitical tensions and fluctuating energy prices impacting investor sentiment. Notably, the small-cap Russell 2000 Index saw a slight decline amid these conditions, highlighting the challenges and opportunities present in this segment of the market. In such an environment, identifying small-cap stocks with potential for growth often involves looking at factors like insider buying as a signal of confidence from those closest to the company.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| CellaVision | 24.1x | 4.4x | 44.93% | ★★★★★★ |

| Eurocell | 11.2x | 0.3x | 49.23% | ★★★★★☆ |

| Centurion | 12.2x | 4.2x | 32.25% | ★★★★★☆ |

| Nederman Holding | 17.4x | 0.8x | 35.34% | ★★★★★☆ |

| Bytes Technology Group | 19.3x | 4.5x | 6.30% | ★★★★☆☆ |

| Primaris Real Estate Investment Trust | 13.7x | 3.9x | 44.29% | ★★★★☆☆ |

| Parkit Enterprise | 4.9x | 5.6x | 13.79% | ★★★★☆☆ |

| Firan Technology Group | 40.5x | 3.0x | 19.06% | ★★★☆☆☆ |

| Chinasoft International | 20.4x | 0.4x | -2587.61% | ★★★☆☆☆ |

| CVS Group | 53.8x | 1.3x | 46.13% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

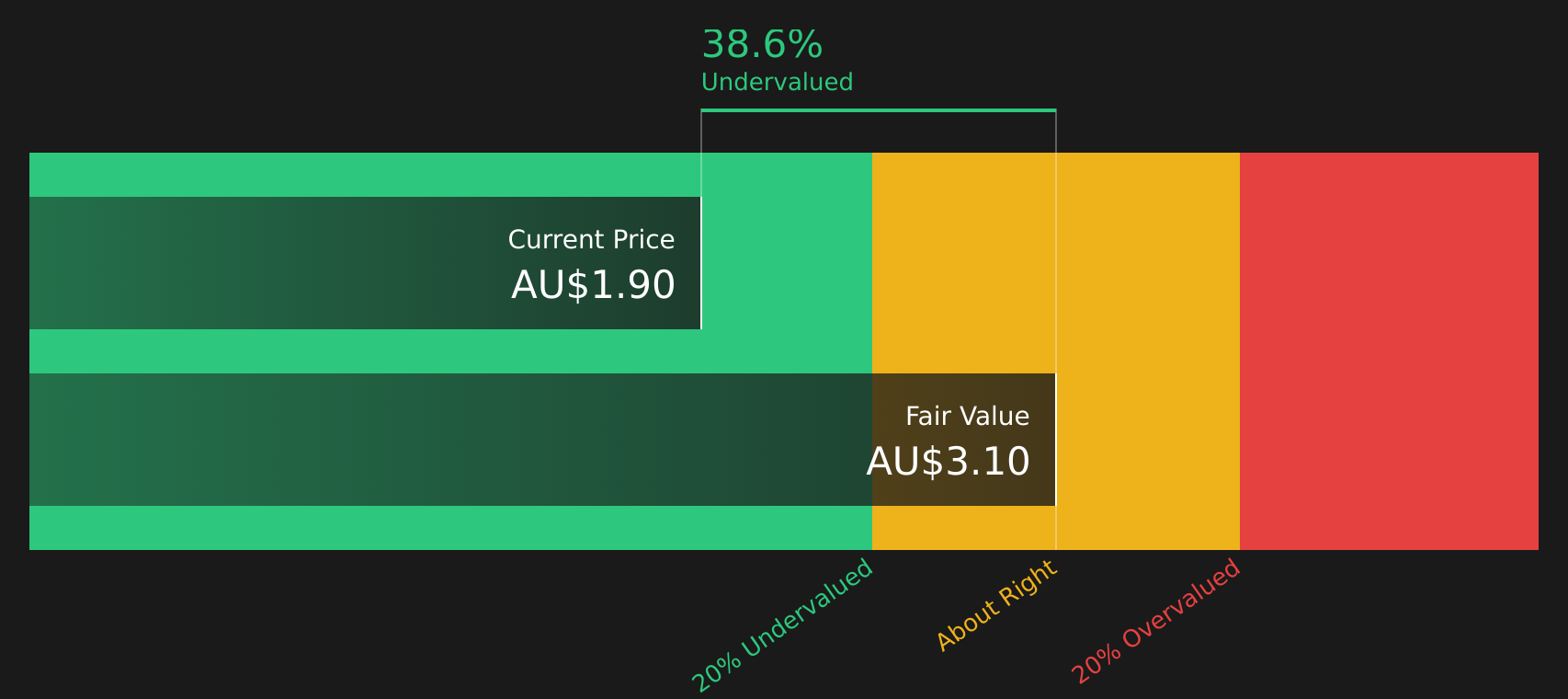

FINEOS Corporation Holdings (ASX:FCL)

Simply Wall St Value Rating: ★★★★★★

Overview: FINEOS Corporation Holdings is a software company specializing in providing core systems for life, accident, and health insurance carriers, with a market capitalization of €0.38 billion.

Operations: FINEOS Corporation Holdings generates revenue primarily from its Software & Programming segment, amounting to €138.43 million. The company has experienced fluctuations in its gross profit margin, reaching 76.21% by the end of 2025. Operating expenses are significant, with research and development being a major component at €57.03 million in the latest period reported.

PE: 432.6x

FINEOS Corporation Holdings, a key player in the insurance software industry, is gaining traction with its AdminSuite platform, recently expanded by OneAmerica Financial to enhance group insurance operations. This strategic move underscores FINEOS' commitment to digital transformation and efficiency. Insider confidence is evident through recent share purchases in May 2026. Despite relying on external borrowing for funding, FINEOS anticipates earnings growth of 39% annually, presenting potential value within its market segment.

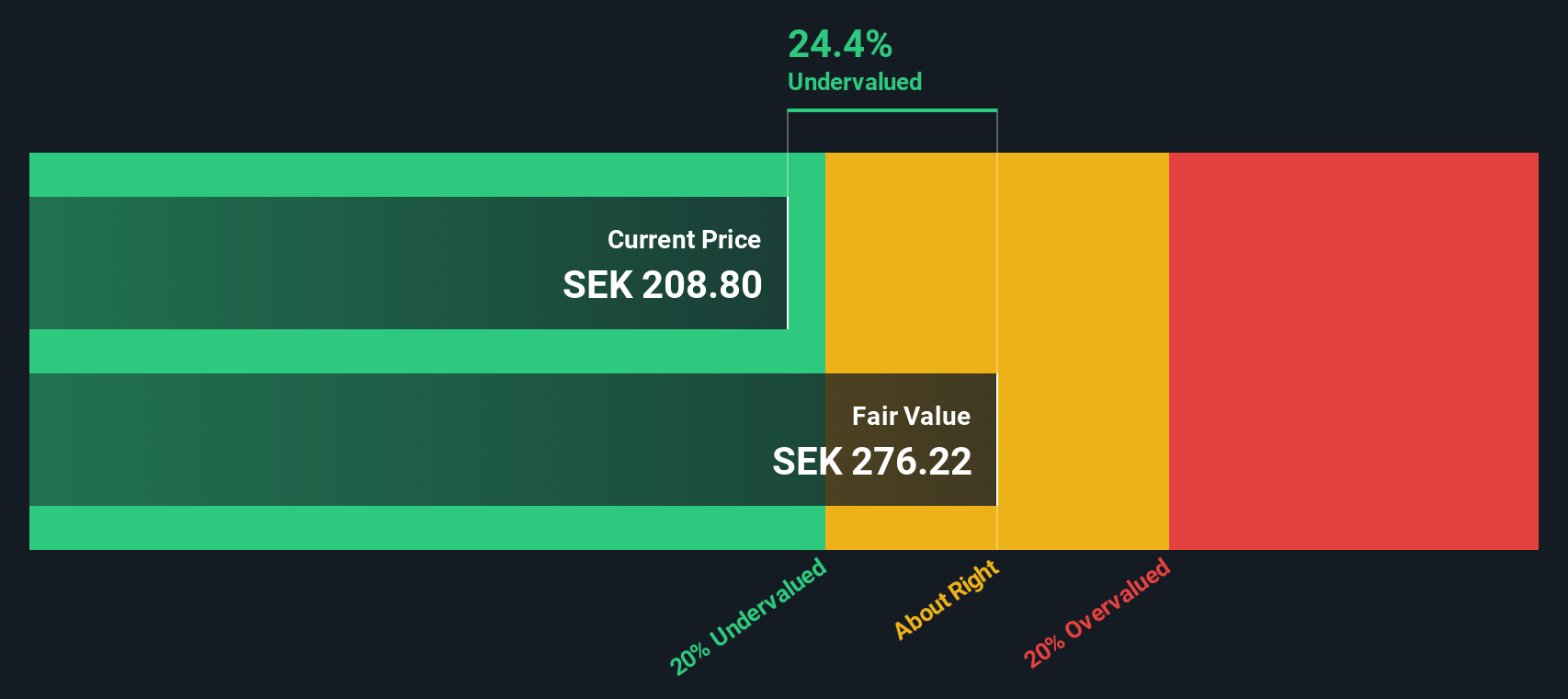

NCC (OM:NCC B)

Simply Wall St Value Rating: ★★★★☆☆

Overview: NCC is a leading construction and property development company in the Nordic region, focusing on building and infrastructure projects, with a market capitalization of approximately SEK 19.76 billion.

Operations: NCC's revenue primarily comes from its operations, with cost of goods sold (COGS) being a significant expense. The company's gross profit margin has shown variability, reaching 10.13% in June 2026. Operating expenses are another major component impacting profitability, including general and administrative costs. Net income margins have been low or negative in some periods, indicating challenges in maintaining consistent profitability over time.

PE: 216.8x

NCC, a company operating in construction and infrastructure, has been gaining attention due to its relatively low valuation in the market. Recent insider confidence is evident as Tomas Carlsson increased their shares by 27%, equating to a transaction value of SEK 8.9 million. Despite facing challenges like a slight decline in sales and net income for the second quarter of 2026, NCC secured significant contracts worth billions of SEK across various projects in Scandinavia. These developments suggest potential growth opportunities amidst current financial pressures.

- Click to explore a detailed breakdown of our findings in NCC's valuation report.

Evaluate NCC's historical performance by accessing our past performance report.

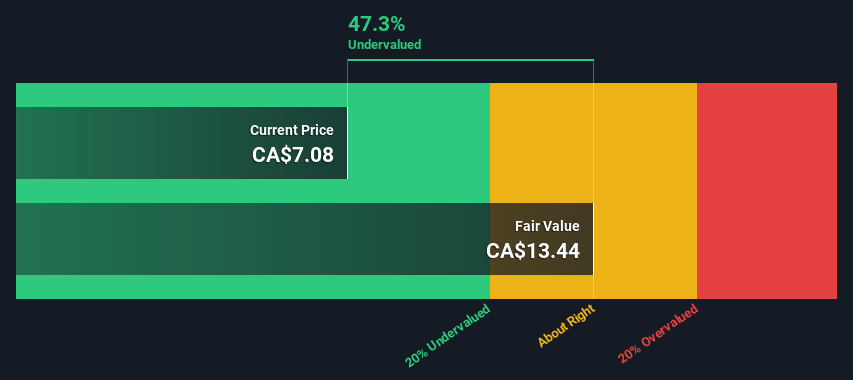

Doman Building Materials Group (TSX:DBM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Doman Building Materials Group operates as a distributor of building materials and related products, with a market capitalization of approximately CA$0.52 billion.

Operations: Doman Building Materials Group generates revenue primarily from its building materials segment, amounting to CA$3.09 billion. The company has experienced fluctuations in its gross profit margin, with a notable increase to 16.27% as of March 2026. Operating expenses have been consistently significant, including general and administrative costs which reached CA$248.07 million in the same period.

PE: 12.5x

Doman Building Materials Group, a stock within the smaller company category, shows mixed signals. Despite a 10.6% annual earnings decline over five years, it maintains steady revenue with a forecasted 5.43% growth annually. Recent insider confidence is evident as they increased their stakes in the past quarter. The company announced its 65th consecutive quarterly dividend of C$0.14 per share for July 2026, underscoring financial stability despite higher-risk external borrowing sources funding liabilities entirely.

Summing It All Up

- Gain an insight into the universe of 130 Undervalued Global Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com