- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Procter & Gamble (PG) Extends 70 Years Of Dividend Increases, Is It Fully Priced?

Procter & Gamble (PG) is back in focus after its board reaffirmed a quarterly dividend of $1.0885 per share on both common and ESOP convertible preferred stock, extending the company’s 70 year streak of annual dividend increases.

See our latest analysis for Procter & Gamble.

Procter & Gamble’s latest dividend move comes as the stock trades at US$148.05, with a 90 day share price return of 3.45% and a 5 year total shareholder return of 20.79%, suggesting steady but not explosive momentum.

If you are assessing dividend reliability at Procter & Gamble and want fresh ideas, this could be a good moment to widen your search with 18 top founder-led companies

Bulls will point to Procter & Gamble’s 70 year dividend streak and steady returns, while bears will highlight the recent share price softness and easing earnings expectations. The key question is whether the current numbers justify today’s valuation.

Most Popular Narrative: 22.3% Overvalued

The most followed narrative on Procter & Gamble values the stock at $121.06, which sits below the latest close at $148.05 and shapes a fairly cautious stance.

Procter & Gamble, despite being within a very competitive industry, still has some competitive advantages shown in its higher operating margin above the ~20% mark and the Morningstar Wide Moat. Also, the fact that the ROIC is double the Cost of Capital means its capital allocation is being well managed. Its solid Moody’s debt rating, along with the Low Uncertainty Morningstar rating, maintains the company as a stable and reliable investment if the opportunity arises.

Want to understand how this wide moat story still ends below today’s price? The key is in modest growth assumptions, disciplined capital costs, and a tight range of valuation models working together.

According to andre_santos, that fair value of $121.06 is built from multiple methods, including dividend-based models, cash flow projections, and several historical market multiples, all anchored on a discount rate of 8.32%.

Result: Fair Value of $121.06 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this overvaluation case for Procter & Gamble could be upset by stronger than expected revenue or earnings trends, or a shift in market risk appetite.

Find out about the key risks to this Procter & Gamble narrative.

Another View on Procter & Gamble’s Value

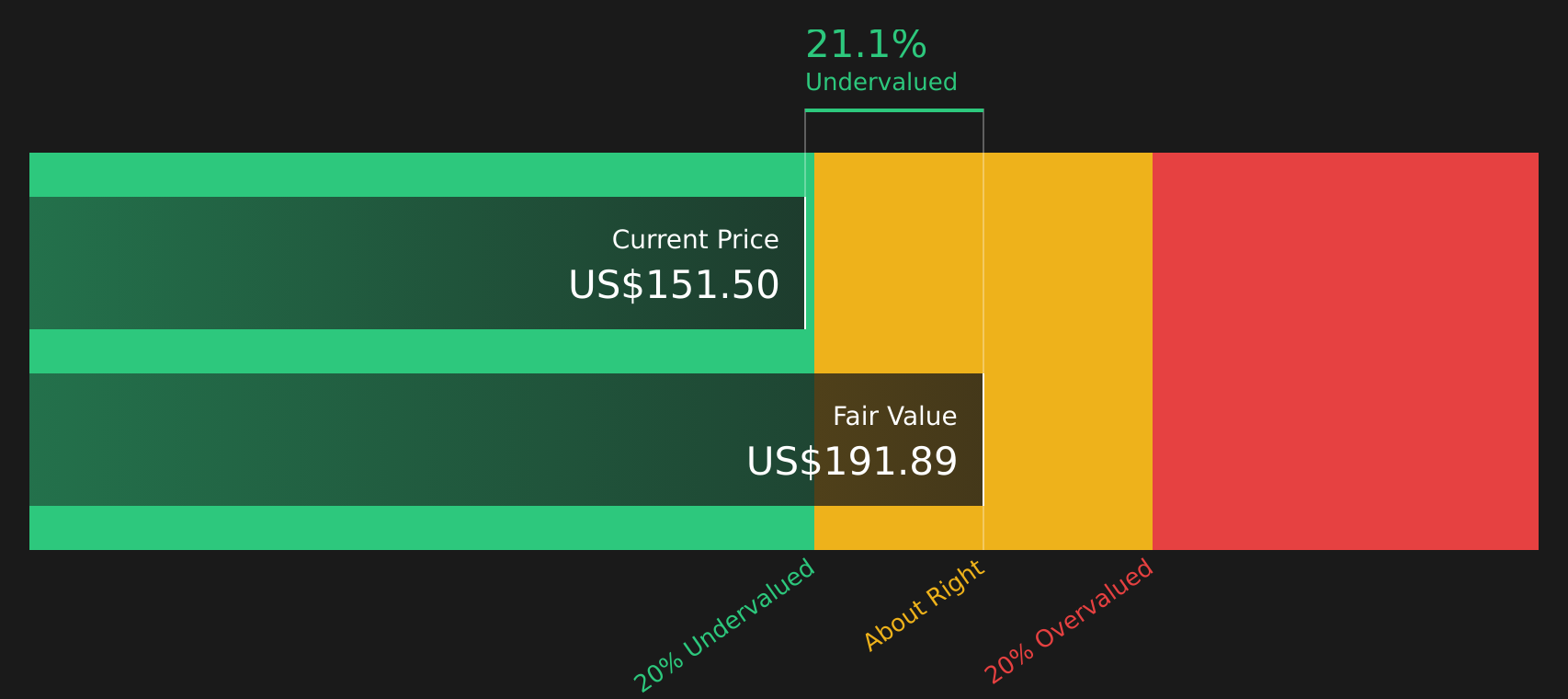

While the most popular narrative on Procter & Gamble argues the stock is overvalued at $148.05 versus a $121.06 fair value, the SWS DCF model points in the opposite direction, suggesting a fair value of $191.89, or 22.8% above the current price. Which set of assumptions do you find more reasonable?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Procter & Gamble for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Procter & Gamble pulling investors in both directions, this is a good time to look through the data yourself and weigh the trade offs. To see both sides clearly and sharpen your own view, start with the 3 key rewards and 1 important warning sign

Looking for more investment ideas beyond Procter & Gamble?

If Procter & Gamble has sharpened your focus on quality and valuation, keep that momentum going by scanning wider opportunities with the Simply Wall Street Screener today.

- Target resilient income by checking out 10 dividend fortresses that aim to combine higher yields with stability for long term portfolios.

- Hunt for potential value opportunities using 47 high quality undervalued stocks that pair strong fundamentals with prices that may sit below intrinsic worth.

- Spot potential future leaders early through a screener containing 20 high quality undiscovered gems before they attract broader market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com