- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Omdia: Market demand in the second half of the year is expected to be weaker than in the first half of the year, but the continued increase in cost pressure will still support the further rise in DDIC prices

The Zhitong Finance App learned that Omdia published an article stating that the price of display driver chips (DDIC) is rising as foundry production capacity tightens and upstream semiconductor manufacturing costs continue to rise. Omdia expects market demand in the second half of 2026 to be weaker than in the first half of the year, but continued increasing cost pressure will support the further rise in DDIC prices.

AI-related applications continue to drive rapid growth in demand for power management chips (PMICs) and memory (Memory), and foundry factories in Taiwan and South Korea are reducing production capacity allocations for TVs, displays, laptop DDICs, and touch and display driver integrated chips (TDDI).

Although total global production capacity is still surplus, some large DDIC orders that are not restricted by geopolitical factors are gradually being transferred from 8-inch fabs in Taiwan to 12-inch fabs in mainland China, but the transfer of orders and production takes time. This shift is causing DDIC's production capacity to temporarily tighten in some application areas. At the same time, the prices of key raw materials required for upstream semiconductor manufacturing are also showing a clear upward trend. Prices of key metals such as gold, silver, and copper used in packaging and chip manufacturing have risen sharply, driving up the overall costs of foundry, packaging, and testing.

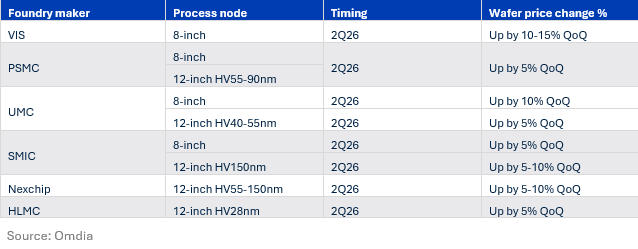

As a result, foundry companies such as World Advanced (VIS), PSMC, and SMIC (SMIC) raised the wafer foundry price for 8-inch fabs by 5% to 10% month-on-month in the first quarter of 2026. At the same time, in the first quarter of 2026, PSC also raised the foundry price for the 12-inch wafer factory HV 90nm (high pressure 90 nm) process. Entering the second quarter of 2026, foundry prices continued to rise, and more foundry companies joined the price increase. It is expected that some foundry prices may continue to rise in the second half of 2026.

Table 1: Price changes by supplier in the second quarter of 2026

Foundry accounts for the highest proportion of display driver chip (DDIC) costs, accounting for 60% to 70% of the total cost, of which silicon wafer (wafer) costs account for about 40%. This means that any increase in foundry prices will directly affect the cost structure of DDIC vendors.

For IC design houses (Design Houses), rising foundry costs provided sufficient grounds for them to raise DDIC prices to reflect increasing production costs.

Smartphone and tablet TDDI have been the first to be affected, and prices rose in the second quarter of 2026, mainly due to reduced HV 90nm process production capacity and price increases in fabs. Among them, the TDDI price of high-definition (HD) smartphones rose 15% to 30% in the second quarter of 2026, and is expected to continue to rise in the second half of 2026.

At the same time, laptop DDIC was affected. Since the market is mainly dominated by IC designers in Taiwan, laptop DDIC prices have risen 5% — 15% in the second quarter of 2026.

Display panel DDIC prices are likely to rise in the third quarter of 2026, while TV DDIC prices are expected to remain flat.

Omdia senior analyst Queenie Jiang (Queenie Jiang) said, “The main driving force behind this round of DDIC price increases is not demand growth, but supply tightening. Although market demand is expected to be weaker in the second half of 2026 than in the first half of the year, rising costs and tight production capacity will still drive DDIC prices up to reflect increasing production costs.”