- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is Merck (MRK) Undervalued As KEYTRUDA Wins New FDA Approvals And Phase 3 Success?

Merck (MRK) is back in focus after two fresh KEYTRUDA milestones, new FDA approvals for bladder cancer regimens with Padcev, and Phase 3 success in endometrial cancer, putting its oncology pipeline under closer investor scrutiny.

See our latest analysis for Merck.

Merck’s recent KEYTRUDA approvals and trial results come after a period of strong momentum, with a 1 month share price return of 7.58% and a year to date share price return of 16.12%. The 1 year total shareholder return of 54.97% and 5 year total shareholder return of 89.13% point to meaningful compounding over time.

If Merck’s oncology progress has caught your attention, it can be helpful to see what other healthcare focused opportunities are out there through 40 healthcare AI stocks

After a 55% 1 year total return and fresh oncology wins putting KEYTRUDA back in the spotlight, the market has clearly re-rated Merck. The real tension now is whether recent gains already reflect the story or still leave room in the valuation.

Most Popular Narrative: 6.9% Undervalued

On the most followed view of Merck, a fair value of $132.78 sits modestly above the last close at $123.61. This puts the recent KEYTRUDA momentum in a tighter valuation frame.

With its acquisition and licensing strategy, Merck has nearly tripled its late-phase pipeline since 2021, which is expected to have a potential commercial opportunity of over $50 billion by the mid-2030s, driving earnings growth.

Want to see what earnings path and margin rebuild this fair value hangs on? The narrative leans on a revamped pipeline, richer profitability and a higher future earnings multiple than many large pharma peers.

Result: Fair Value of $132.78 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Merck’s story still has pressure points, with KEYTRUDA’s eventual loss of exclusivity and policy shifts around drug pricing both capable of reshaping that 6.9% undervaluation case.

Find out about the key risks to this Merck narrative.

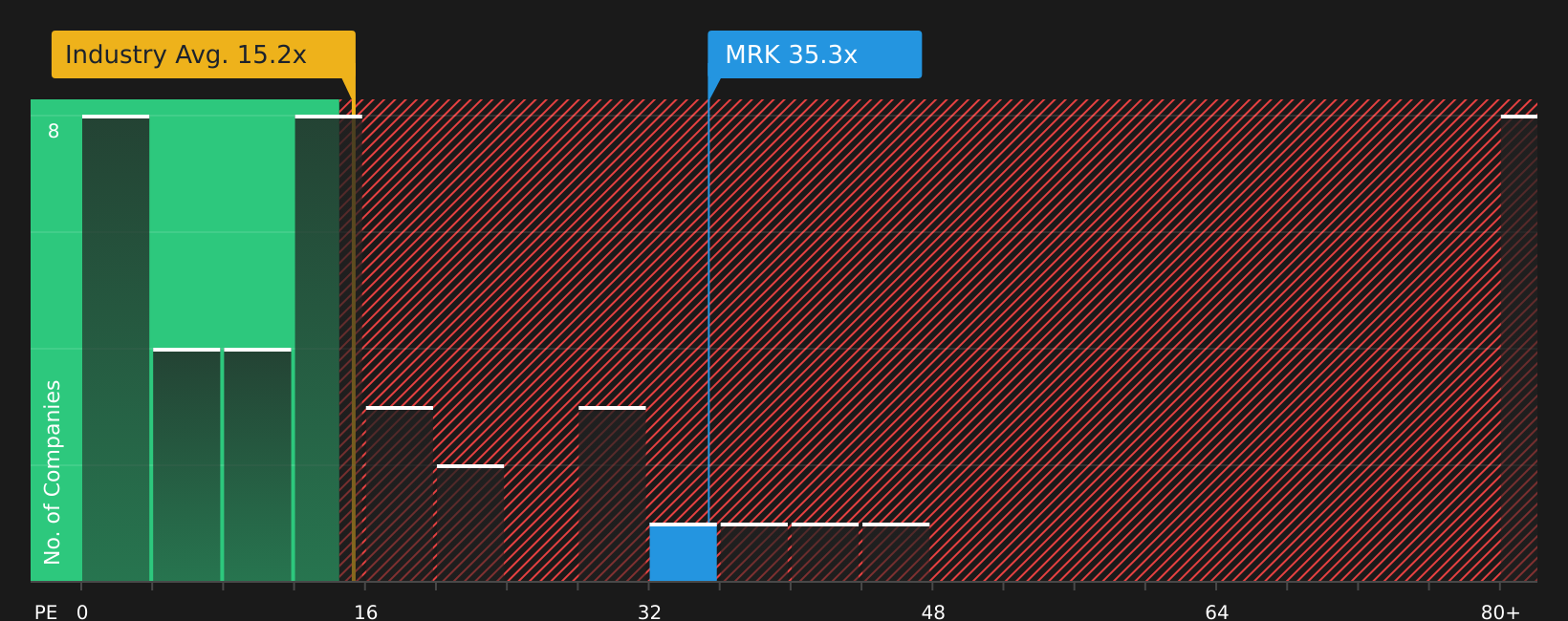

Another View: Merck’s Valuation Through a P/E Lens

If the 6.9% undervalued fair value for Merck sounds reasonable, its current P/E of 34.2x tells a more cautious story. That multiple sits well above the US Pharmaceuticals sector at 15.1x and above peers at 26.1x, even though it is close to the fair ratio of 35.8x. For investors, does paying such a premium for Merck’s earnings feel like a margin of safety, or more like paying up for a crowded oncology story?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Balanced on this mix of oncology excitement and valuation questions, it makes sense to act now and test the data yourself. Weigh Merck’s potential rewards against its pressure points by checking the 2 key rewards and 4 important warning signs

Looking for more Merck sized investment ideas?

If Merck has sharpened your focus on finding stronger opportunities, do not stop here. Broaden your watchlist with a few targeted screens that can surface fresh candidates.

- Target potential mispricing by checking companies highlighted in the 47 high quality undervalued stocks.

- Strengthen your income stream by reviewing the 10 dividend fortresses.

- Dial down portfolio stress by focusing on the 78 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com