- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Huntington’s New REIT and Utilities Research Platform at HBAN Has Changed Its Investment Story

- Earlier this month, Huntington Securities, Inc., a subsidiary of Huntington Bancshares Incorporated, launched an equity research platform for Huntington Capital Markets clients, initially targeting Real Estate Investment Trusts (REITs) and Utilities with coverage led by two senior analysts.

- This move adds a research capability that can deepen institutional client engagement and strengthen Huntington’s position in capital markets–adjacent services.

- We’ll now examine how adding a REITs and Utilities research platform could influence Huntington Bancshares’ existing investment narrative and growth plans.

Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

Huntington Bancshares Investment Narrative Recap

To own Huntington Bancshares, you need to believe in its ability to translate regional banking scale, disciplined lending, and fee income into durable earnings, while managing interest rate and regulatory pressures. The new REITs and Utilities research platform modestly supports the near term growth catalyst of deeper capital markets engagement, but does not materially change the primary risk around integrating its expansion into faster growing markets like Texas and the Carolinas.

Among recent announcements, the US$3,000,000,000 share repurchase authorization stands out in this context, as it sits alongside investments in areas like sector research and expansion into high population growth markets. Together, these moves reflect a focus on enhancing Huntington’s capital markets relevance while still facing the ongoing challenge of balancing growth ambitions with digitization demands and potential margin compression.

Yet behind these promising initiatives, investors should also be aware of rising regulatory scrutiny and the risk that...

Read the full narrative on Huntington Bancshares (it's free!)

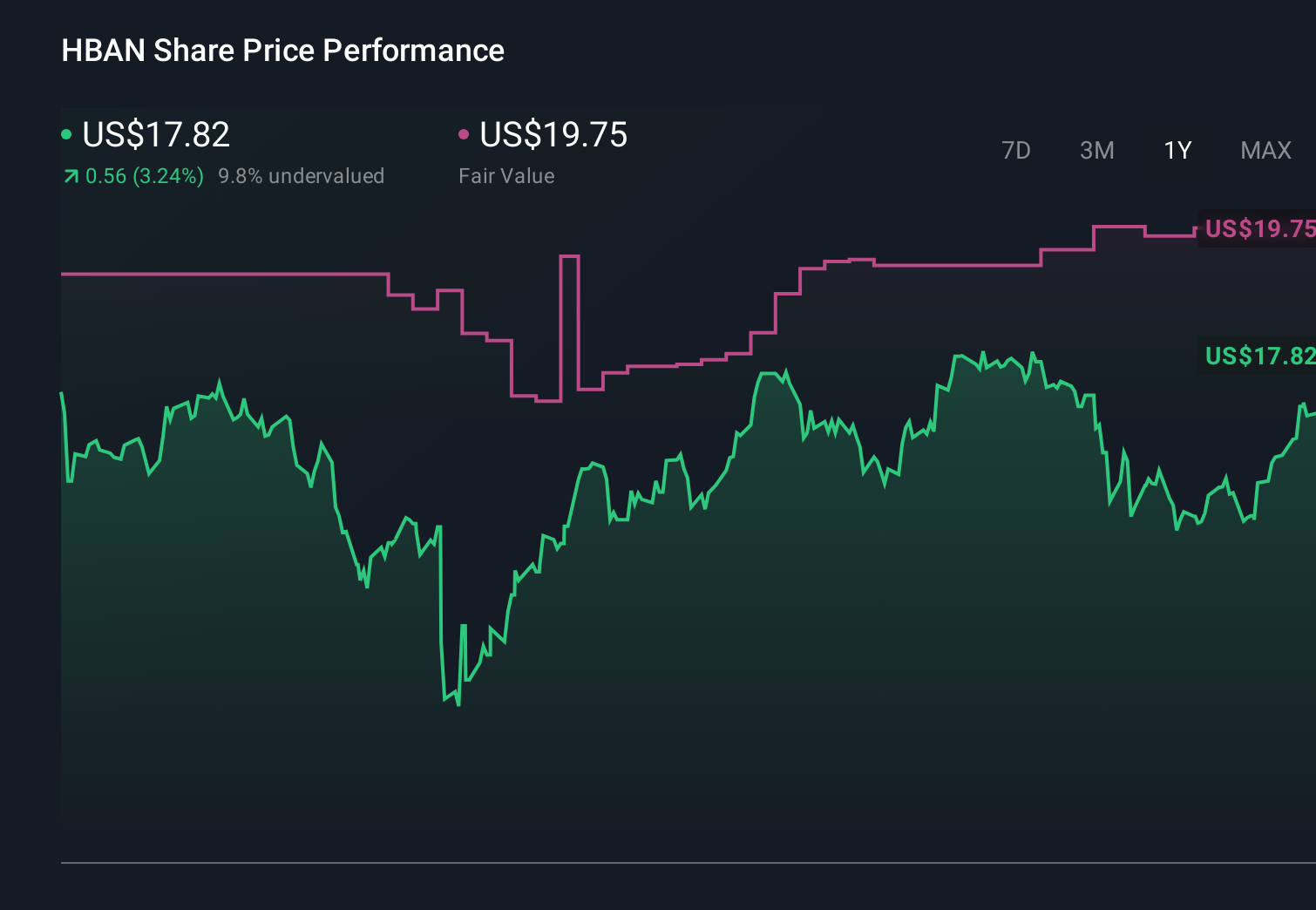

Huntington Bancshares' narrative projects $14.5 billion revenue and $3.7 billion earnings by 2029. This requires 20.5% yearly revenue growth and about a $1.6 billion earnings increase from $2.1 billion today.

Uncover how Huntington Bancshares' forecasts yield a $20.34 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community place Huntington’s fair value between US$20.34 and US$33.35, showing how far apart individual views can be. Set against this, the bank’s push into REITs and Utilities research highlights how different investors may weigh new fee income opportunities against existing concerns about integration risk and regional concentration.

Explore 3 other fair value estimates on Huntington Bancshares - why the stock might be worth just $20.34!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Huntington Bancshares research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Huntington Bancshares research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huntington Bancshares' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com