- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Camtek (CAMT) Jumps As AI Packaging Demand Narrative Keeps Fair Value In View

Camtek (CAMT) shares moved sharply on July 14, 2026, rising 9.5% to US$149.90 after a 4.9% decline the previous day, putting the stock well above its referenced GF Value.

See our latest analysis for Camtek.

That sharp move in Camtek comes after a mixed stretch, with the share price return up 5.2% over the past week but down 25.5% over 30 days. At the same time, the 1-year total shareholder return of 61.9% and 3-year total shareholder return above 3x point to strong longer term momentum.

If Camtek’s recent volatility has you thinking about where else growth and risk are being repriced, this is a good moment to scan 52 AI infrastructure stocks.

After a one day jump that has pushed Camtek well above its referenced GF Value, the core issue now is simple: is most of the re rating already in the price, or is there meaningful upside still on the table?

Most Popular Narrative: 21.3% Undervalued

Compared with Camtek’s last close at $147.31, the most widely followed narrative fair value of $187.25 reflects a sizeable valuation gap that rests on specific growth and margin assumptions rather than short term trading swings.

Accelerating demand for high-performance computing (HPC) and AI-driven applications is expanding the need for advanced packaging, micro-bump, and hybrid bonding inspection, directly growing Camtek's total addressable market and supporting multi-year revenue growth.

Want to see what kind of revenue curve, margin lift, and future earnings multiple are incorporated into that fair value for Camtek? The narrative relies on steep earnings expansion, higher profitability and a re rated P/E that still reflects growth. The exact mix of these levers may surprise you.

Result: Fair Value of $187.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Camtek’s heavy revenue exposure to Asia and reliance on a relatively concentrated group of high bandwidth memory and advanced packaging customers could quickly challenge this upbeat narrative if spending or access patterns change.

Find out about the key risks to this Camtek narrative.

Another Look at Camtek’s Valuation

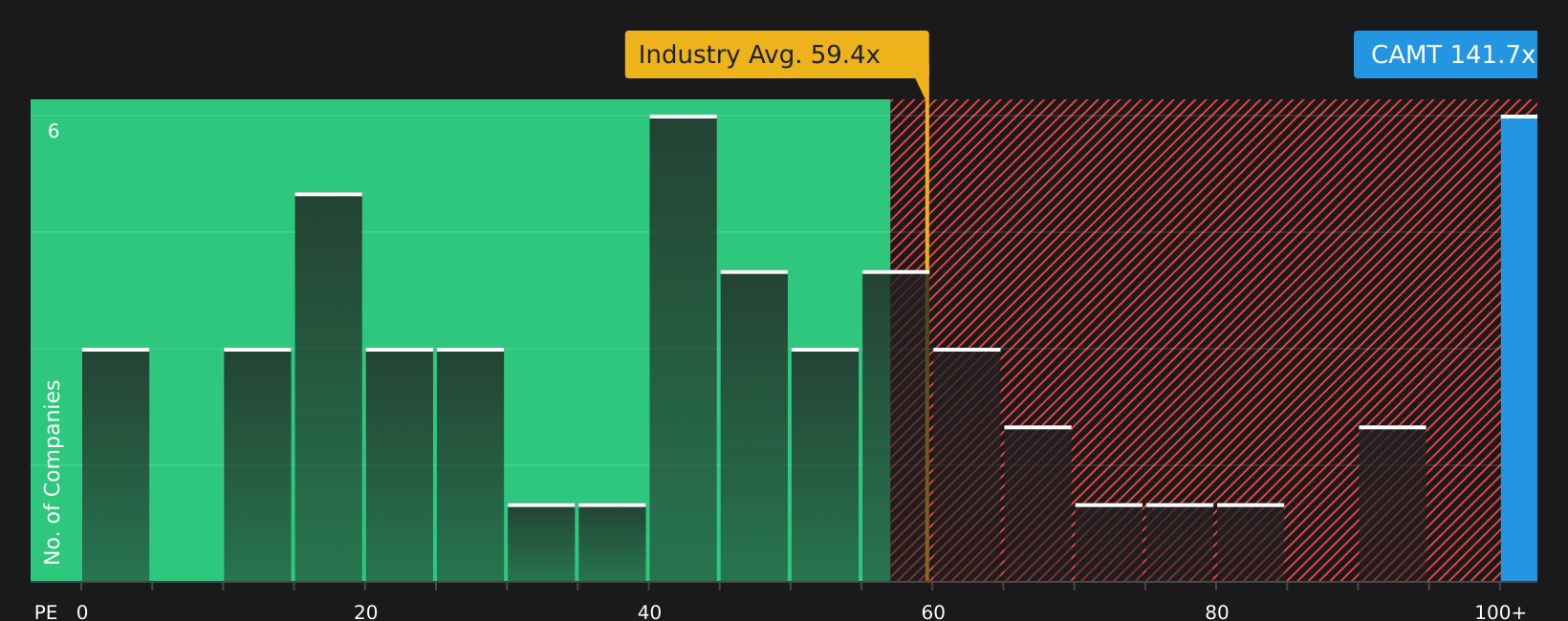

The analyst narrative points to Camtek as 21.3% undervalued using future earnings assumptions, but the current P/E of 141.1x tells a different story. That multiple is more than double the US Semiconductor industry at 63.4x, well above peers at 90.3x, and far ahead of a fair ratio of 63.9x. This spread suggests the market could move toward a lower multiple over time. For investors, that gap raises a simple question: is this optimistic pricing a margin of safety or a valuation risk if growth expectations ease?

To see how the current pricing stacks up against the numbers in more detail, have a look at the valuation breakdown built around this earnings multiple, including the fair ratio and peer comparisons, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With Camtek priced for strong expectations and the story clearly split between potential risks and rewards, this is a good time to move quickly, review the underlying data, and arrive at your own stance using the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Camtek?

If Camtek has sharpened your focus on where valuations and fundamentals meet, do not stop here, the Simply Wall Street screener can surface other compelling setups.

- Spot potential bargains early by reviewing screener containing 20 high quality undiscovered gems that pair strong fundamentals with lower market attention.

- Strengthen your core holdings by checking solid balance sheet and fundamentals stocks screener (48 results) built around companies with cleaner finances and resilient profiles.

- Dial down portfolio stress by scanning 78 resilient stocks with low risk scores that screens for stocks with lower risk scores and steadier characteristics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com