- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Asian Growth Companies With High Insider Ownership July 2026

As geopolitical tensions and energy market volatility dominate global headlines, Asian markets are navigating a complex economic landscape. Amid these challenges, growth companies with high insider ownership can offer unique insights into potential resilience and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| HUMAN MADE (TSE:456A) | 23.9% | 23.4% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

We'll examine a selection from our screener results.

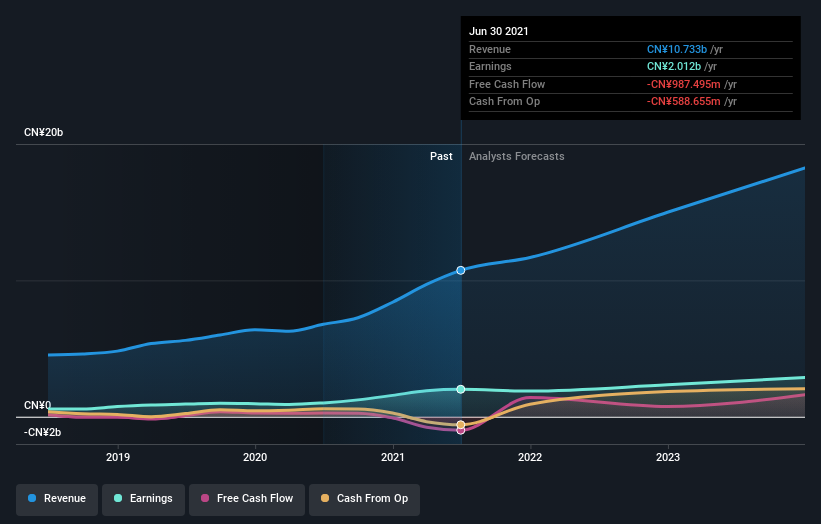

Hangzhou First Applied Material (SHSE:603806)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hangzhou First Applied Material Co., Ltd. operates in the research, development, production, and sales of new materials both in China and internationally, with a market capitalization of approximately CN¥38.44 billion.

Operations: The company generates revenue through its involvement in the research, development, production, and sales of innovative materials within China and on a global scale.

Insider Ownership: 13.5%

Earnings Growth Forecast: 40% p.a.

Hangzhou First Applied Material is positioned as a growth company in Asia, with earnings forecast to grow significantly at 40% annually, surpassing the CN market's average. Despite lower profit margins than last year and reduced first-quarter revenue (CNY 3.37 billion), it trades at good value relative to peers with a P/E ratio of 56.5x against the industry average of 132.5x. No substantial insider trading was recorded recently, but its unstable dividend track record remains a concern.

- Dive into the specifics of Hangzhou First Applied Material here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential undervaluation of Hangzhou First Applied Material shares in the market.

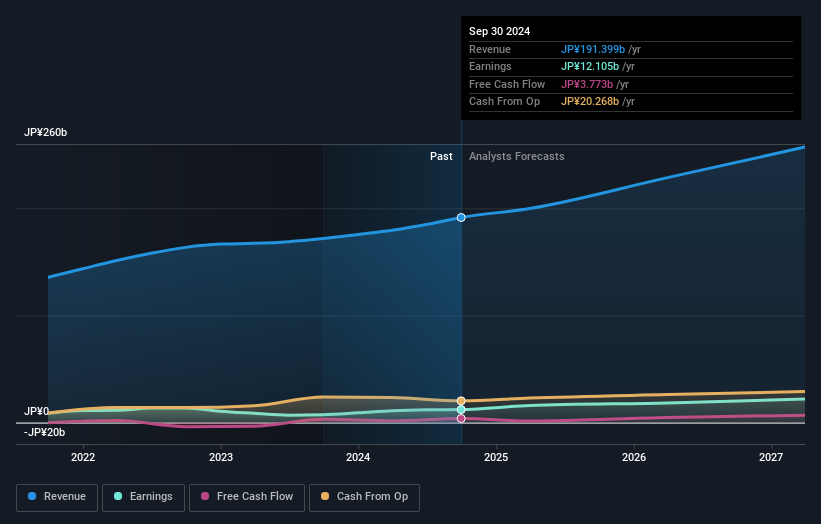

Meiko Electronics (TSE:6787)

Simply Wall St Growth Rating: ★★★★★★

Overview: Meiko Electronics Co., Ltd. designs, manufactures, and sells printed circuit boards (PCBs) and auxiliary electronics across Japan, China, Vietnam, the rest of Asia, North America, Europe, and internationally with a market cap of ¥691.20 billion.

Operations: Revenue Segments (in millions of ¥): Printed Circuit Boards: ¥77,500; Auxiliary Electronics: ¥15,300.

Insider Ownership: 19.2%

Earnings Growth Forecast: 27.6% p.a.

Meiko Electronics is experiencing robust growth, with earnings forecasted to increase by 27.6% annually, surpassing the Japanese market's average. Revenue is also expected to grow at 21.4% per year, outpacing the market's 6.5%. Despite high debt levels and recent share price volatility, Meiko's inclusion in the S&P Japan 500 and a significant dividend increase highlight its strong performance. No substantial insider trading was noted recently, but high non-cash earnings are present.

- Unlock comprehensive insights into our analysis of Meiko Electronics stock in this growth report.

- In light of our recent valuation report, it seems possible that Meiko Electronics is trading beyond its estimated value.

Kinik (TWSE:1560)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kinik Company manufactures and distributes a range of abrasives, cutting tools, and reclaimed wafers both in Taiwan and internationally, with a market cap of NT$110.50 billion.

Operations: The company's revenue is derived from two main segments: the Electronics Sector, contributing NT$3.89 billion, and the Traditional Sectors, accounting for NT$4.78 billion.

Insider Ownership: 15.7%

Earnings Growth Forecast: 26% p.a.

Kinik's earnings are forecast to grow significantly at 26% annually, outpacing the Taiwan market. The recent Q1 results showed a strong performance, with net income rising to TWD 436.36 million from TWD 285.82 million year-over-year. Despite revenue growth being slightly below market expectations, Kinik maintains high return on equity forecasts and has shown substantial past profit growth of 42%. No major insider trading activity was reported in the last three months.

- Get an in-depth perspective on Kinik's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, Kinik's share price might be too optimistic.

Key Takeaways

- Embark on your investment journey to our 475 Fast Growing Asian Companies With High Insider Ownership selection here.

- Contemplating Other Strategies? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com