- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

European Consumer Staples Stocks Investors May Revisit As Oil Prices Rise

Surging oil prices, a possible extra ECB rate hike and eurozone inflation near 3.2% are forcing investors to think carefully about where capital feels most resilient. European defensive consumer staples stocks, especially the larger groups with broad product portfolios, can sometimes act as a financial shock absorber when energy costs climb and growth worries build. This article looks at how that backdrop connects to our European Defensive Consumer Staples screener and highlights 3 stocks that appear positively exposed to the latest news. This may help you judge whether they merit a closer look or a spot on your watchlist.

Floridienne (ENXTBR:FLOB)

Overview: Floridienne is a Belgium based group that mixes specialty chemicals, gourmet food and life sciences, from plastic additives and battery recycling to snails, seafood products and plant based health and agriculture solutions. Through this mix of essential food items and niche industrial and bio based products, Floridienne serves both everyday consumers and specialist B2B customers across multiple industries.

Operations: Floridienne generates most of its €725.88 million revenue from the Life Sciences Division at about €538.27 million, with Food at €155.23 million and Recycling at €32.38 million, and sells mainly into the Americas at €362.49 million and wider Europe at €328.31 million including Belgium.

Market Cap: €577.47 million

Floridienne stands out in this screener because it combines everyday food staples with life sciences and recycling activities that can feel relatively steady when inflation and energy costs are in focus. Forecast earnings growth of 60.59% a year and revenue growth of 11.3% a year have caught attention, especially given the company’s exposure to agriculture, hygiene and health care products that can hold up when conditions are tougher. Set against that, margins are thin at a 1.1% net margin, interest costs are a concern and the stock trades on a very high P/E, well above both local peers and our DCF estimate of fair value. That tension between growth potential and financial strain is what makes Floridienne worth a closer look.

Floridienne’s mix of everyday staples and fast growing life sciences is attracting attention, but the real story sits in how that growth stacks up against its thin margins, interest costs and premium P/E in the DCF valuation analysis for Floridienne

Glanbia (ISE:GL9)

Overview: Glanbia is an Ireland headquartered nutrition group that produces sports and lifestyle nutrition brands like Optimum Nutrition and Isopure, as well as cheese, dairy and non dairy ingredients and vitamin and mineral premixes that feed into a wide range of everyday food and beverage products. It sells these through channels such as specialist retailers, gyms, supermarkets and e commerce platforms around the world.

Operations: Glanbia generates most of its revenue from Performance Nutrition at about $1.8b and Dairy Nutrition at about $1.6b, with Health & Nutrition contributing around $631 million and a small offset from inter segment revenue.

Market Cap: €5.61b

Glanbia attracts interest in a period of higher oil prices and inflation worries because it combines essential dairy and nutrition products with exposure to growing protein and health trends. At the same time, a recent $122.8 million one off loss, modest 4.6% net margins, a relatively high P/E and reliance on external borrowing underline that this is not a low risk utility style staple, especially with volatile input costs and competitive U.S. nutrition markets. How those positives and pressure points balance out, particularly given analyst targets and the stock’s past volatility, is where the deeper Glanbia story sits for investors willing to look closer.

Glanbia’s mix of everyday dairy and high profile sports nutrition could be masking a very different risk reward profile compared with what the headline P/E suggests. The full picture sits inside the 3 key rewards and 3 important warning signs

AGRANA Beteiligungs-Aktiengesellschaft (WBAG:AGR)

Overview: AGRANA Beteiligungs-Aktiengesellschaft is an Austria based producer of sugar, starch and fruit preparations that go into everyday foods and drinks, as well as ingredients for cosmetics, pharmaceuticals, animal feed, fertilizers, bioethanol and various industrial uses across Europe and internationally.

Operations: AGRANA generates most of its revenue from Food & Beverage Solutions at about €1.65b and ACS Starch at about €987.52m, with smaller contributions from Holding Co. & Other and segment adjustments.

Market Cap: €718.62m

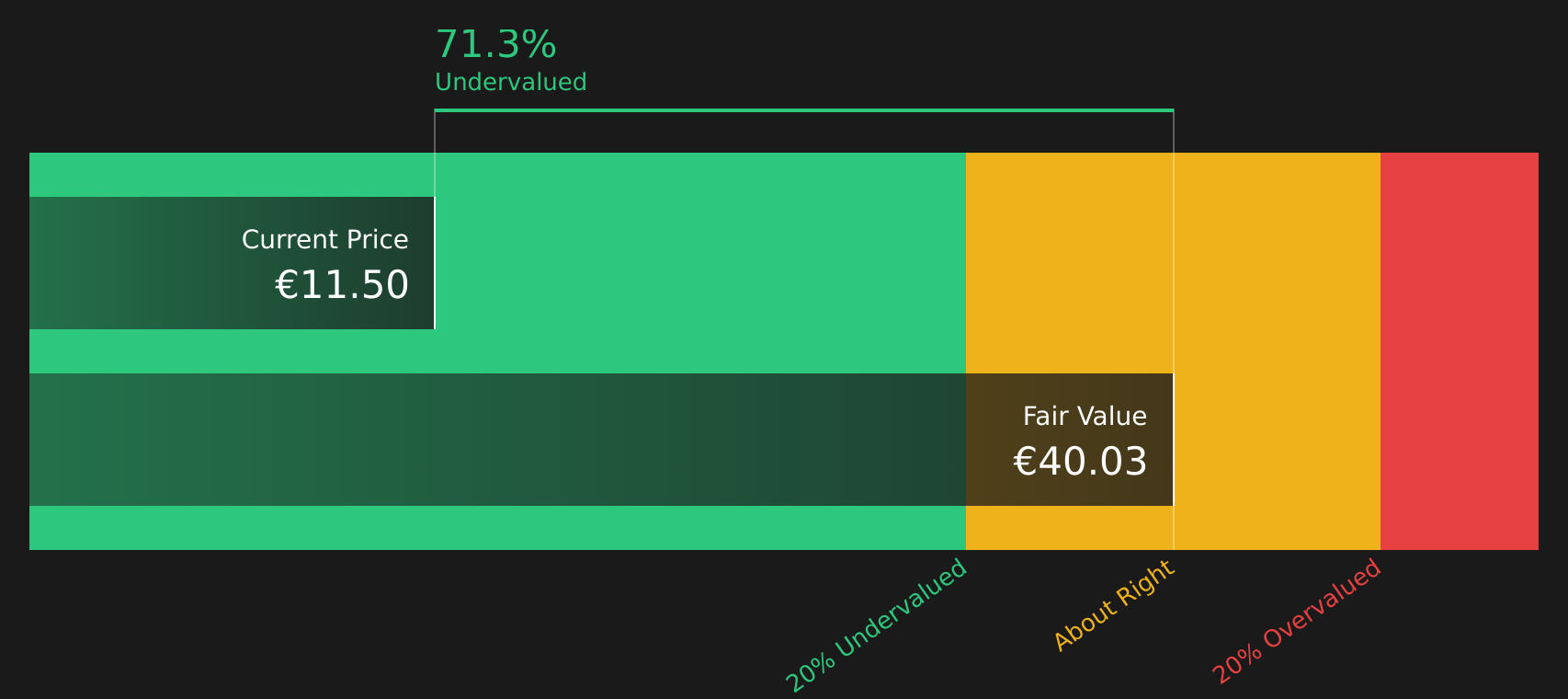

AGRANA Beteiligungs-Aktiengesellschaft offers characteristics many investors may focus on when energy prices and inflation concerns rise, including a core role in Europe’s food chain that is tied to sugar, starch and fruit ingredients consumers use every day. The stock is described as deeply discounted on Simply Wall St’s fair value assessment and a low P/S multiple. At the same time, the group is still working through recent losses, high borrowing and a dividend that is not well covered by earnings. Management has stated a target of much higher EBIT this year and has reported a move from loss to profit in Q1 2026. Together with its ethanol and bio-based exposure, AGRANA presents a mix of resilience and operational repair for investors who want to understand what is currently priced in.

AGRANA Beteiligungs-Aktiengesellschaft looks like a plain sugar and starch supplier on the surface, yet the mix of food staples, ethanol and a “deeply discounted” valuation hints at something more complex. To see how that potential value intersects with recent losses, high borrowing and the shift back to profit in Q1 2026, go through the analysis report for AGRANA Beteiligungs-Aktiengesellschaft

The three stocks here are a starting point, but the full European Defensive Consumer Staples screen has uncovered 7 more large companies with equally compelling stories sitting inside the European Defensive Consumer Staples screener. Use Simply Wall St to identify, filter and analyze the specific catalysts, balance sheet traits and geographic exposures discussed here so you can focus on the highest conviction opportunities for your own portfolio.

Take Control of Your Investment Journey

If AGRANA Beteiligungs-Aktiengesellschaft or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Staples?

Fresh ideas do not stay quiet for long. Catch breakout momentum, spot stocks flying under the radar for now and move before data goes stale, act now.

- Spot under-the-radar quality by scanning companies on the 503 high quality undiscovered gems curated to highlight strong fundamentals before the crowd catches on.

- Ride powerful income trends by reviewing the 464 dividend fortresses built to surface companies combining higher yields with balance sheets that aim to support those payouts.

- Target resilient compounding by filtering through the 298 resilient stocks with low risk scores that centers on companies with lower risk scores and steadier financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com