- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

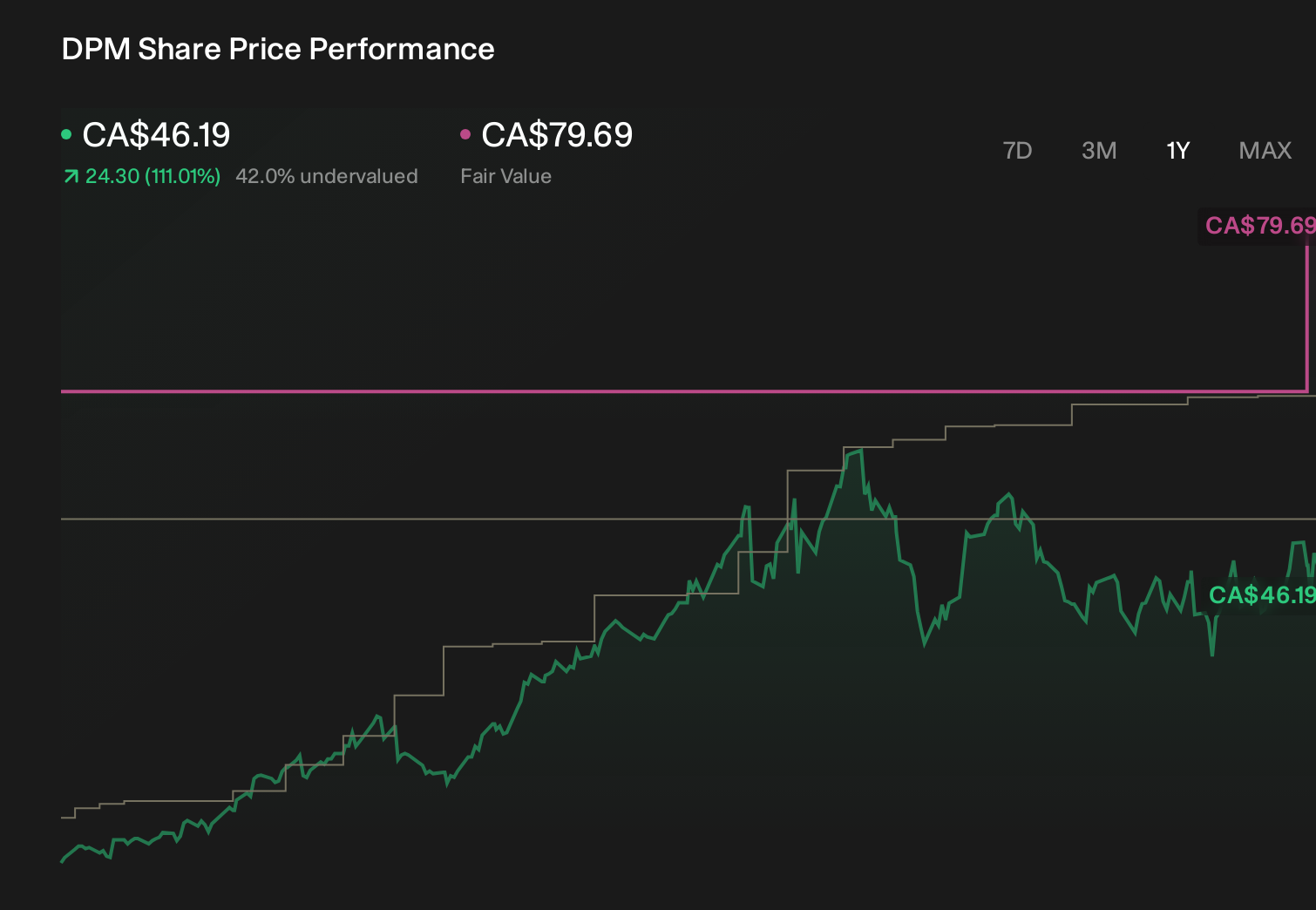

Will Q2 Output And Buybacks At DPM Metals (TSX:DPM) Change Its Growth-Focused Narrative

- DPM Metals Inc. has released preliminary operating results for the second quarter and first half of 2026, reporting ore processed of 884 Kt and 1,617 Kt respectively, along with gold equivalent production of 102 Koz in Q2 and 187 Koz year-to-date across its gold, silver, copper, zinc, and lead output.

- At the same time, the company completed a share repurchase of 1,442,548 shares for $49.4 million, trimming its share count by 0.65% and signaling continued use of its balance sheet to return capital to shareholders.

- We’ll now examine how this latest quarter’s 102 Koz of gold-equivalent production shapes DPM Metals’ previously outlined growth-focused investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

DPM Metals Investment Narrative Recap

To own DPM Metals, you need to believe in its ability to sustain multi‑asset production while replacing ounces lost as Ada Tepe winds down and projects like Coka Rakita progress. The latest 102 Koz of gold equivalent in Q2 2026 looks operationally steady and does not materially change the near term focus on offsetting future Ada Tepe closure risk and managing rising cost pressures.

The recent share repurchase of 1,442,548 shares for US$49.4 million, reducing the share count by 0.65%, is the announcement that ties most directly to this quarter’s update, as it reflects how current production and cash generation are supporting capital returns even while the company funds exploration at Chelopech/Brevene and advances longer dated projects like Coka Rakita.

But against this, investors should be aware that the planned Ada Tepe wind down could still leave a production gap if...

Read the full narrative on DPM Metals (it's free!)

DPM Metals’ narrative projects $1.3 billion revenue and $686.4 million earnings by 2029.

Uncover how DPM Metals' forecasts yield a CA$64.32 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who were modeling revenue of about US$1.5 billion and earnings near US$978.7 million by 2029, see Q2 production as a test of whether growth projects like Vareš can offset risks such as potential delays at Coka Rakita, reminding you that reasonable views on DPM Metals can differ widely and may shift as new data comes in.

Explore 4 other fair value estimates on DPM Metals - why the stock might be worth just CA$63.80!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your DPM Metals research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free DPM Metals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DPM Metals' overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 7 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com