- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

July 2026's Undervalued Small Caps With Insider Action Across Regions

Over the last 7 days, the United States market has remained flat, yet it has experienced a robust 20% increase over the past year with earnings forecasted to grow by 18% annually. In this environment, identifying small-cap stocks that are perceived as undervalued and show insider activity can offer intriguing opportunities for investors seeking potential growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Peoples Bancorp | 12.2x | 3.2x | 40.35% | ★★★★★☆ |

| Appian | 2088.7x | 2.4x | 33.03% | ★★★★★☆ |

| First Bancorp | 10.5x | 4.0x | 21.05% | ★★★★☆☆ |

| Bank of Marin Bancorp | NA | 12.8x | 28.29% | ★★★★☆☆ |

| Kingstone Companies | 9.3x | 1.3x | 36.37% | ★★★★☆☆ |

| Modiv Industrial | NA | 3.9x | 49.02% | ★★★★☆☆ |

| AVITA Medical | NA | 1.7x | 18.39% | ★★★★☆☆ |

| German American Bancorp | 13.1x | 4.8x | 39.54% | ★★★☆☆☆ |

| Union Bankshares | 9.9x | 2.1x | 16.11% | ★★★☆☆☆ |

| Angel Studios | NA | 2.0x | 10.24% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

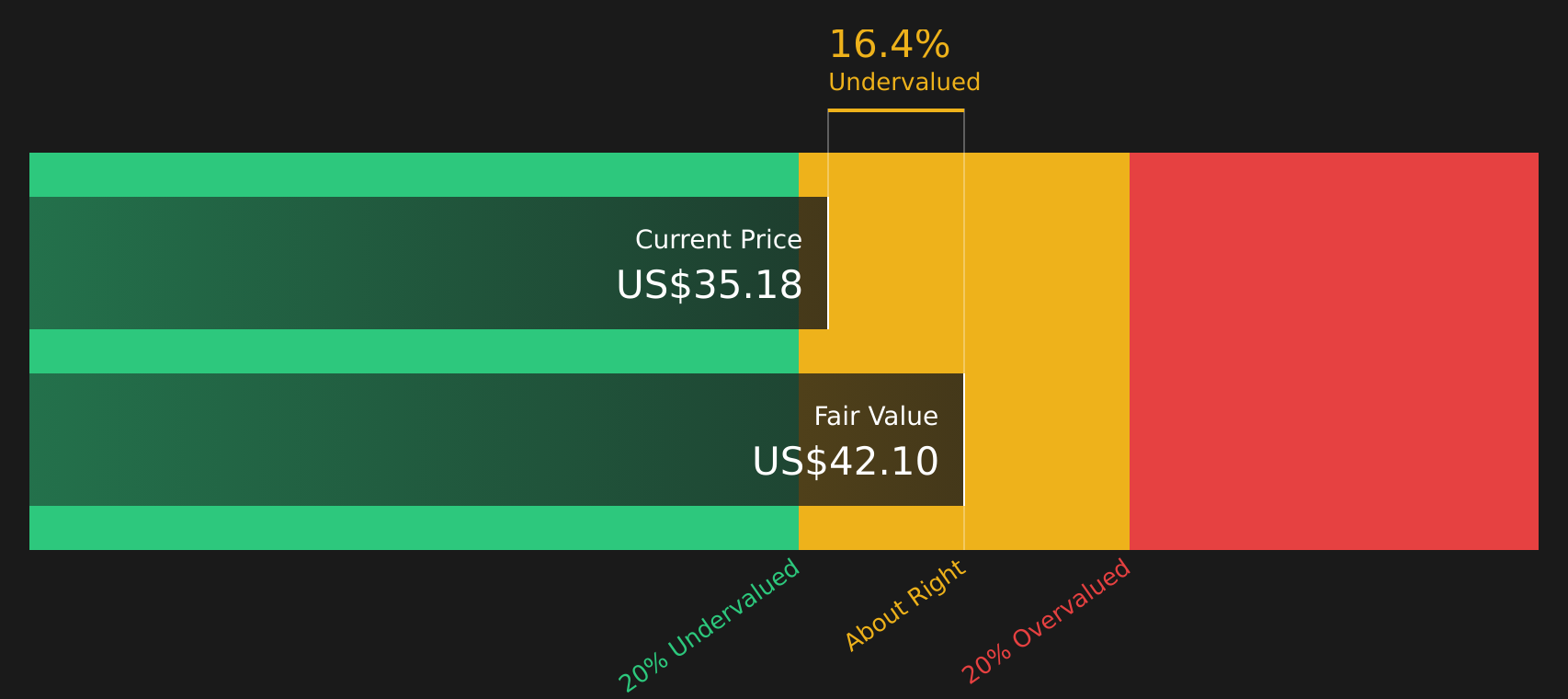

Value Line (VALU)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Value Line is a company that provides investment research and financial information services, with operations primarily in publishing, and has a market capitalization of approximately $0.47 billion.

Operations: The company generates revenue primarily from publishing, with recent figures indicating $33.83 million. Its cost structure includes key expenses such as cost of goods sold (COGS) and operating expenses, which were $6.04 million and $22.95 million respectively in the latest period. The net income margin has shown an upward trend, reaching 65.05% recently, reflecting a strong profitability position despite fluctuations in gross profit margin over time.

PE: 16.7x

Value Line, a company with a focus on financial analytics, has seen its earnings decline by 2.5% annually over the last five years. Despite this, they recently increased their quarterly dividend to US$0.35 per share, marking the twelfth consecutive annual increase—a sign of insider confidence. However, recent exclusion from multiple Russell indices may raise concerns about market perception and liquidity risks due to reliance on external borrowing for funding.

- Click to explore a detailed breakdown of our findings in Value Line's valuation report.

Review our historical performance report to gain insights into Value Line's's past performance.

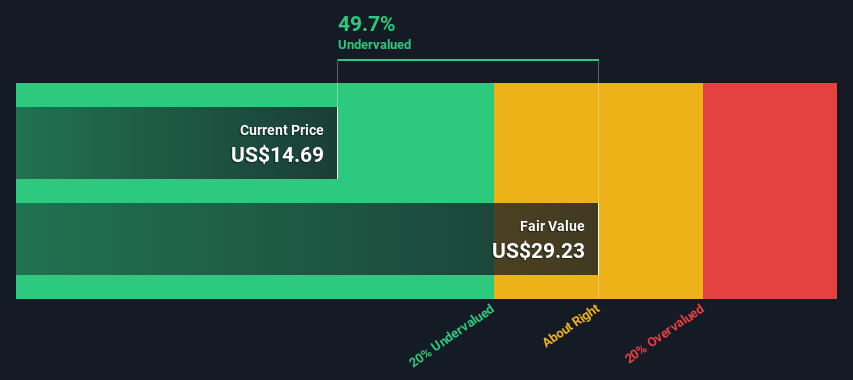

Colony Bankcorp (CBAN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Colony Bankcorp operates as a financial holding company providing a range of banking services through its divisions, with a market cap of approximately $0.13 billion.

Operations: The company's revenue is primarily driven by its Banking Division, with additional contributions from the Mortgage Banking and Small Business Specialty Lending Divisions. Operating expenses are a significant component of costs, including general and administrative expenses. Notably, the net income margin has shown variability over time, reaching 22.73% as of September 2025.

PE: 14.5x

Colony Bankcorp, a smaller player in the financial sector, showcases potential with its recent earnings report highlighting net interest income of US$29.2 million for Q1 2026, up from US$20.95 million the previous year. Insider confidence is evident as they increased their holdings over the past months. The company repurchased 89,109 shares for US$1.76 million between January and March 2026, reflecting strategic capital management amidst ongoing merger discussions as of June 25, 2026.

- Delve into the full analysis valuation report here for a deeper understanding of Colony Bankcorp.

Evaluate Colony Bankcorp's historical performance by accessing our past performance report.

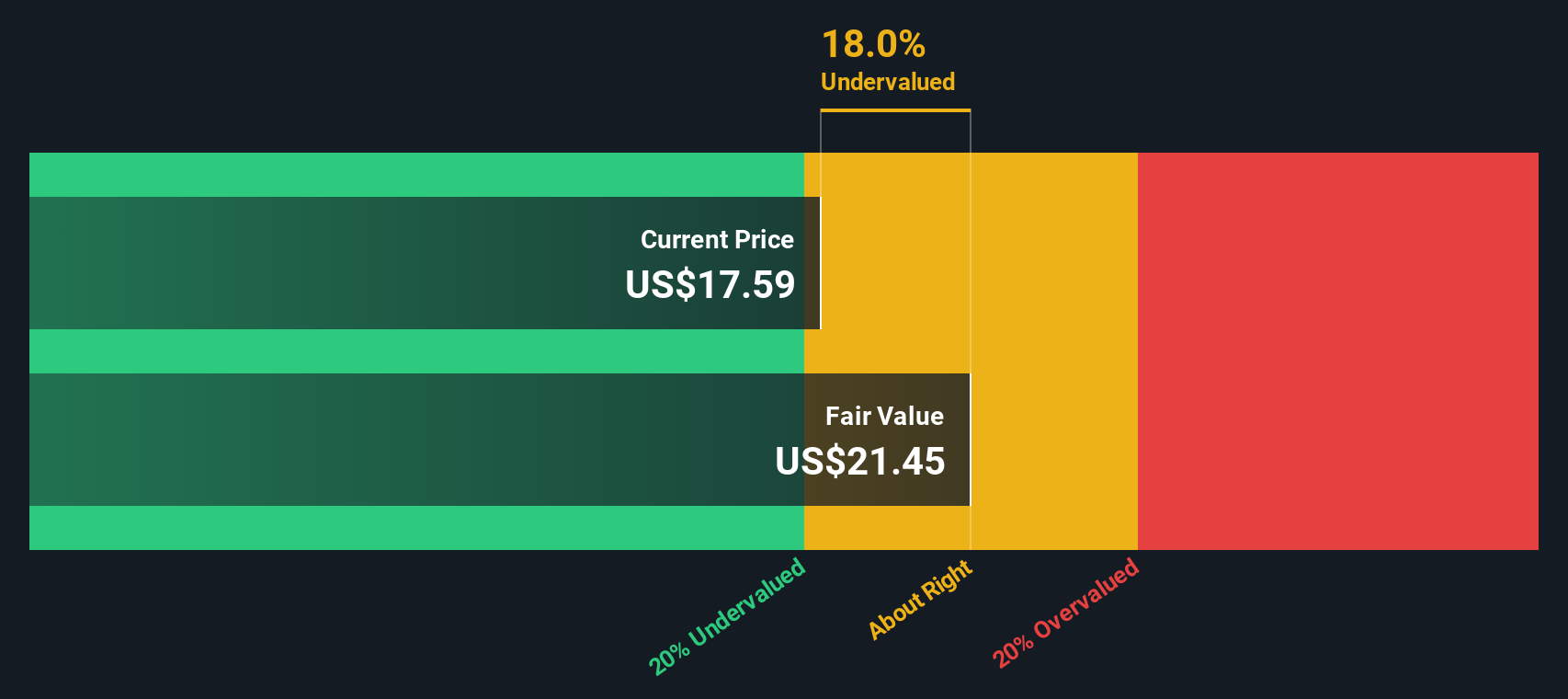

Northpointe Bancshares (NPB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Northpointe Bancshares operates in the financial sector, focusing on retail banking and mortgage warehouse services, with a market capitalization of $1.25 billion.

Operations: Retail Banking and Mortgage Warehouse (MPP) are the primary revenue streams, contributing significantly to total revenue. The company's net income margin has shown an upward trend from 5.32% in December 2022 to 31.12% by July 2026, indicating improved profitability over time. Operating expenses have generally increased but at a slower rate compared to revenue growth, supporting the rising net income margin.

PE: 8.2x

Northpointe Bancshares, a small company with significant growth potential, anticipates earnings to rise by 15.89% annually. Despite a modest allowance for bad loans at 11%, the firm shows financial resilience. Recent inclusion in the Russell 2000 Value-Defensive Index underscores its defensive appeal. For Q1 2026, net interest income climbed to US$41 million from US$30 million year-over-year, and net income rose to US$22 million from US$17 million. A dividend of $0.025 per share reflects stable shareholder returns.

Turning Ideas Into Actions

- Dive into all 62 of the Undervalued US Small Caps With Insider Buying we have identified here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com