- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Top European Dividend Stocks To Consider

Amidst geopolitical tensions and energy market volatility, the European stock market has faced challenges, with the pan-European STOXX Europe 600 Index recently experiencing a decline. Despite these uncertainties, dividend stocks remain an attractive option for investors seeking steady income streams in fluctuating markets. A strong dividend stock typically combines reliable payouts with a resilient business model that can withstand economic pressures and adapt to changing conditions.

Top 10 Dividend Stocks In Europe

| Name | Dividend Yield | Dividend Rating |

| Zurich Insurance Group (SWX:ZURN) | 4.09% | ★★★★★★ |

| Teleperformance (ENXTPA:TEP) | 8.42% | ★★★★★★ |

| Telekom Austria (WBAG:TKA) | 4.17% | ★★★★★★ |

| Swiss Re (SWX:SREN) | 4.76% | ★★★★★★ |

| Rubis (ENXTPA:RUI) | 6.47% | ★★★★★★ |

| Logista Integral (BME:LOG) | 5.94% | ★★★★★★ |

| Hannover Rück (XTRA:HNR1) | 4.94% | ★★★★★★ |

| Edel SE KGaA (XTRA:EDL) | 6.20% | ★★★★★★ |

| DKSH Holding (SWX:DKSH) | 3.70% | ★★★★★★ |

| Cembra Money Bank (SWX:CMBN) | 4.57% | ★★★★★★ |

Click here to see the full list of 212 stocks from our Top European Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

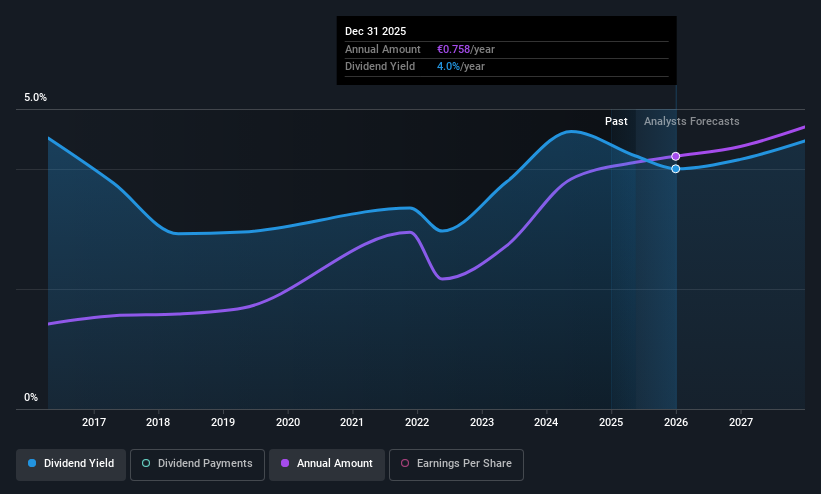

FinecoBank Banca Fineco (BIT:FBK)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: FinecoBank Banca Fineco S.p.A. offers banking, credit, trading, and investment services in Italy with a market cap of €14.29 billion.

Operations: FinecoBank Banca Fineco S.p.A. generates its revenue primarily from its banking segment, which accounts for €1.32 billion.

Dividend Yield: 3.4%

FinecoBank Banca Fineco's dividend prospects show a mixed picture. The bank has increased its dividends over the past decade, yet payments have been volatile with significant annual drops. Its payout ratio is currently 74.6%, indicating dividends are covered by earnings, and this coverage is expected to remain stable in three years at 76.7%. However, the dividend yield of 3.38% lags behind Italy's top payers, and recent earnings slightly decreased to €162.19 million for Q1 2026 from €164.19 million last year.

- Take a closer look at FinecoBank Banca Fineco's potential here in our dividend report.

- Our valuation report here indicates FinecoBank Banca Fineco may be overvalued.

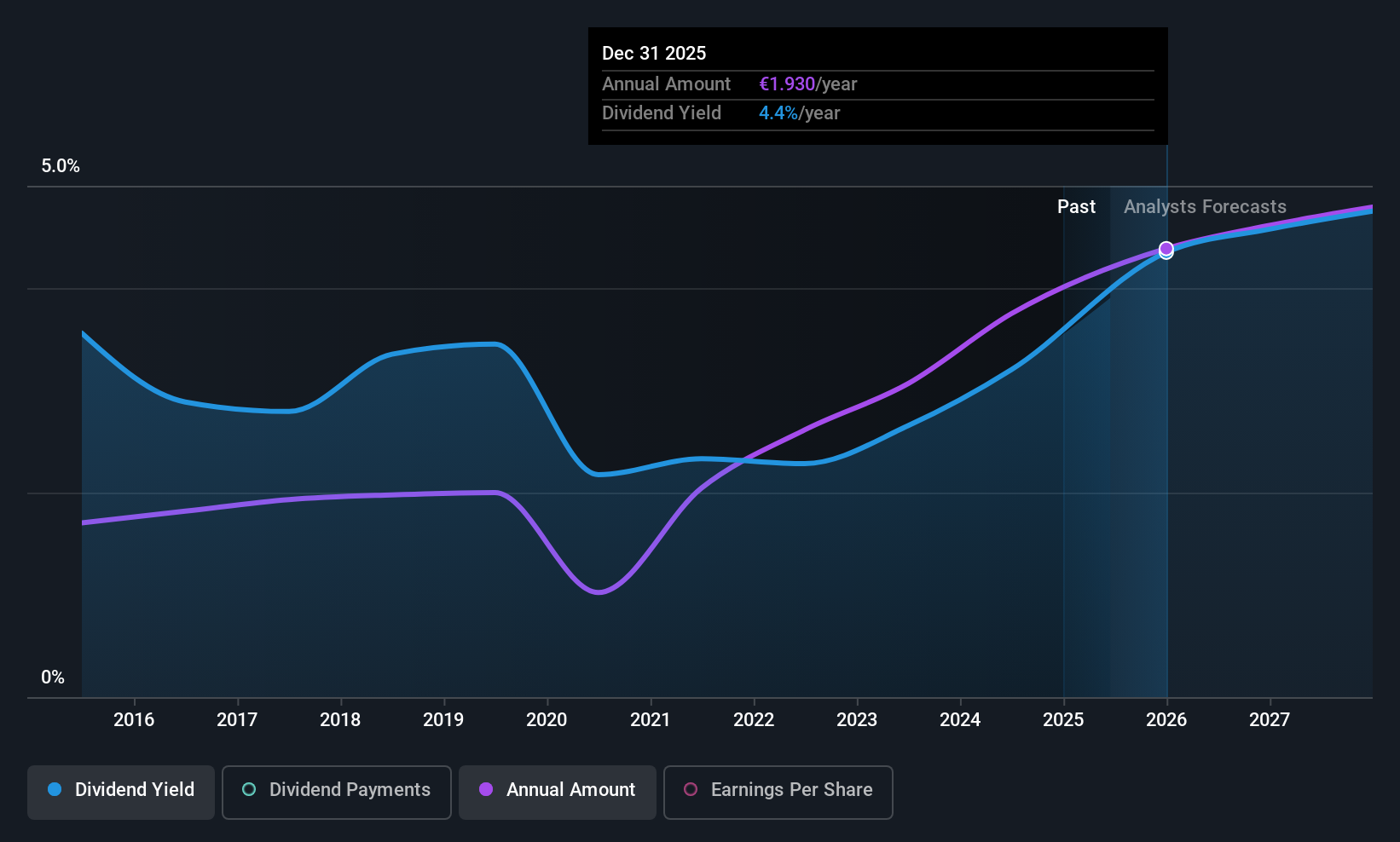

Ipsos (ENXTPA:IPS)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Ipsos SA, with a market cap of €1.51 billion, operates through its subsidiaries to offer survey-based research services for companies and institutions across Europe, the Middle East, Africa, the Americas, and the Asia-Pacific.

Operations: Ipsos SA generates its revenue primarily from survey-based research services, amounting to €2.52 billion.

Dividend Yield: 5.7%

Ipsos offers a compelling dividend yield of 5.66%, ranking in the top 25% among French dividend payers. Despite this, its dividend history is marked by volatility, with payments experiencing significant annual drops over the past decade. However, dividends are well-covered by both earnings and cash flows, with payout ratios at 46.2% and 39.1%, respectively. Recent leadership changes aim to support strategic growth and stability amidst a slight revenue decline to €554.9 million in Q1 2026.

- Click here to discover the nuances of Ipsos with our detailed analytical dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Ipsos shares in the market.

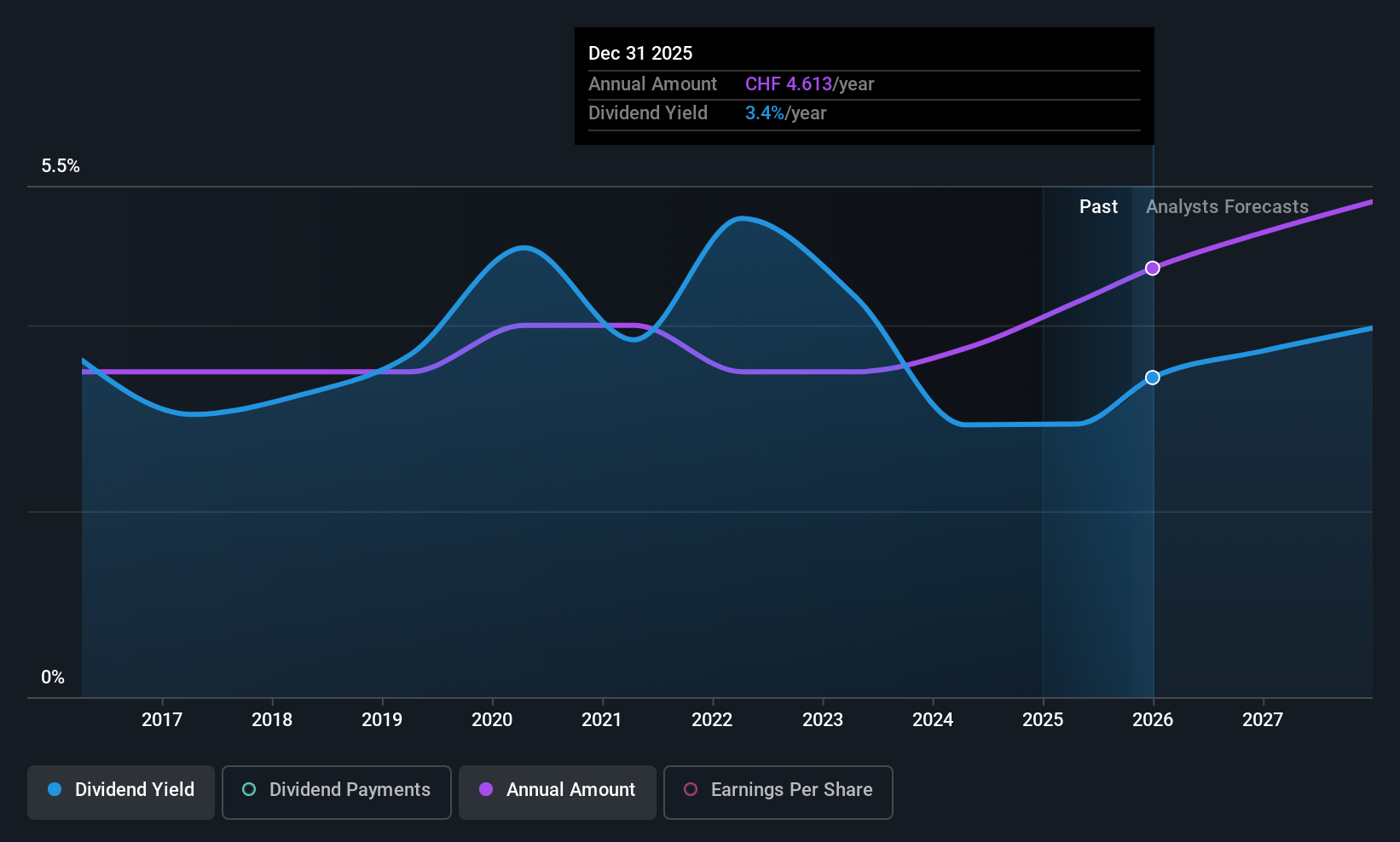

Sulzer (SWX:SUN)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Sulzer AG specializes in developing and selling products and services for fluid engineering and chemical processing applications globally, with a market cap of CHF4.79 billion.

Operations: Sulzer AG generates revenue through its key segments: Flow at CHF1.55 billion, Chemtech at CHF691.30 million, and Services at CHF1.31 billion.

Dividend Yield: 3.3%

Sulzer's dividends have been reliable and stable over the past decade, with payments covered by earnings (54.7% payout ratio) and cash flows (76.1% cash payout ratio). Although its 3.35% dividend yield is below the top quartile in Switzerland, it trades at a significant discount to its estimated fair value. Recent earnings growth of 11.8% supports sustainability, while ongoing presentations at international conferences highlight its strategic focus on industry engagement and innovation.

- Delve into the full analysis dividend report here for a deeper understanding of Sulzer.

- Our expertly prepared valuation report Sulzer implies its share price may be lower than expected.

Key Takeaways

- Click here to access our complete index of 212 Top European Dividend Stocks.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com