- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Sally Martin’s Appointment Hint At A Strategic Shift In Viva Energy’s Risk Playbook (ASX:VEA)?

- Viva Energy Group has appointed Ms Sally Martin as an Independent Non-Executive Director, effective 1 September 2026, bringing extensive global refining, trading and health, safety and environment experience from her long career at Shell and current board roles at Sandfire Resources and Beach Energy.

- Her deep operational and governance background across energy and resources could influence how Viva Energy manages refining risk, safety standards and its broader transition within the traditional fuels sector.

- We’ll now examine how Sally Martin’s board appointment could influence Viva Energy’s existing investment narrative around refining, retail growth and risk management.

We've uncovered the 6 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Viva Energy Group Investment Narrative Recap

To own Viva Energy, you generally need to believe its mix of refining, retail fuels and convenience can recover from recent losses and support more stable cash flow over time. Sally Martin’s appointment looks incrementally positive for refining risk oversight and safety governance, but it is unlikely to change the key near term swing factor, which remains exposure to volatile refining margins and oil prices. The biggest current risk is that continued losses and high capital needs pressure the balance sheet and dividends.

The most relevant recent announcement alongside Martin’s appointment is the weak FY25 result, with a net loss of A$421.1 million and interest not well covered by earnings. Against this backdrop, a more experienced and energy focused board, including Martin and earlier additions such as Dr Sarah Ryan, could matter for decisions on capex, Geelong refinery risk and how hard Viva leans into the capital intensive convenience and mobility rollout.

Yet beneath the apparent progress, investors should be aware that Viva’s reliance on traditional fuels and a loss making base still leave it exposed to...

Read the full narrative on Viva Energy Group (it's free!)

Viva Energy Group's narrative projects A$31.9 billion revenue and A$304.8 million earnings by 2029. This requires 3.8% yearly revenue growth and an earnings increase of about A$726 million from -A$421.1 million today.

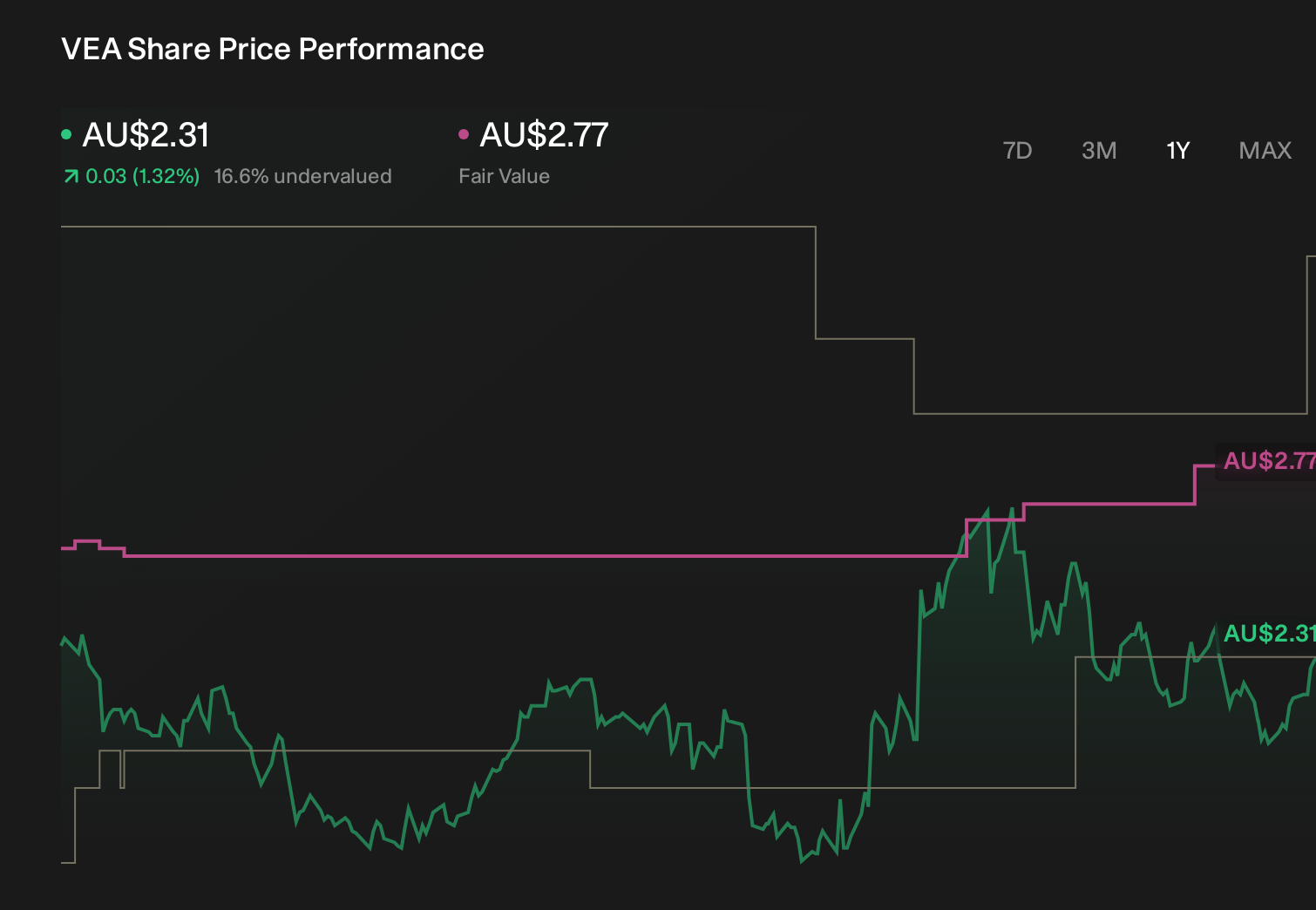

Uncover how Viva Energy Group's forecasts yield a A$2.77 fair value, a 19% upside to its current price.

Exploring Other Perspectives

The most bearish analysts were assuming Viva would only reach A$43.1 million in earnings on flat A$28.5 billion revenues by 2029, so compared with that more cautious view, Martin’s appointment could either ease concerns about refining risk or highlight how much still depends on execution and future policy shifts.

Explore 4 other fair value estimates on Viva Energy Group - why the stock might be worth just A$2.64!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Viva Energy Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Viva Energy Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viva Energy Group's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 59 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com