- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Promising UK Penny Stocks To Consider In July 2026

The UK market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, impacting companies closely tied to its economic performance. In such a climate, investors may seek opportunities in lesser-known areas like penny stocks—an investment category that still holds potential for growth despite its somewhat outdated terminology. These stocks often represent smaller or newer companies that can offer growth prospects at lower price points when supported by strong financial health and solid fundamentals.

We're going to check out a few of the best picks from our screener tool.

BRCK Group (AIM:BRCK)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: BRCK Group plc, with a market cap of £167.13 million, distributes specialist products and services to the construction industry in the United Kingdom through its four segments: Bricks and Building Materials, Importing, Distribution, and Contracting.

Operations: BRCK Group generates its revenue through four segments: Bricks and Building Materials, Importing, Distribution, and Contracting, all focused on serving the construction industry in the United Kingdom.

Market Cap: £167.13M

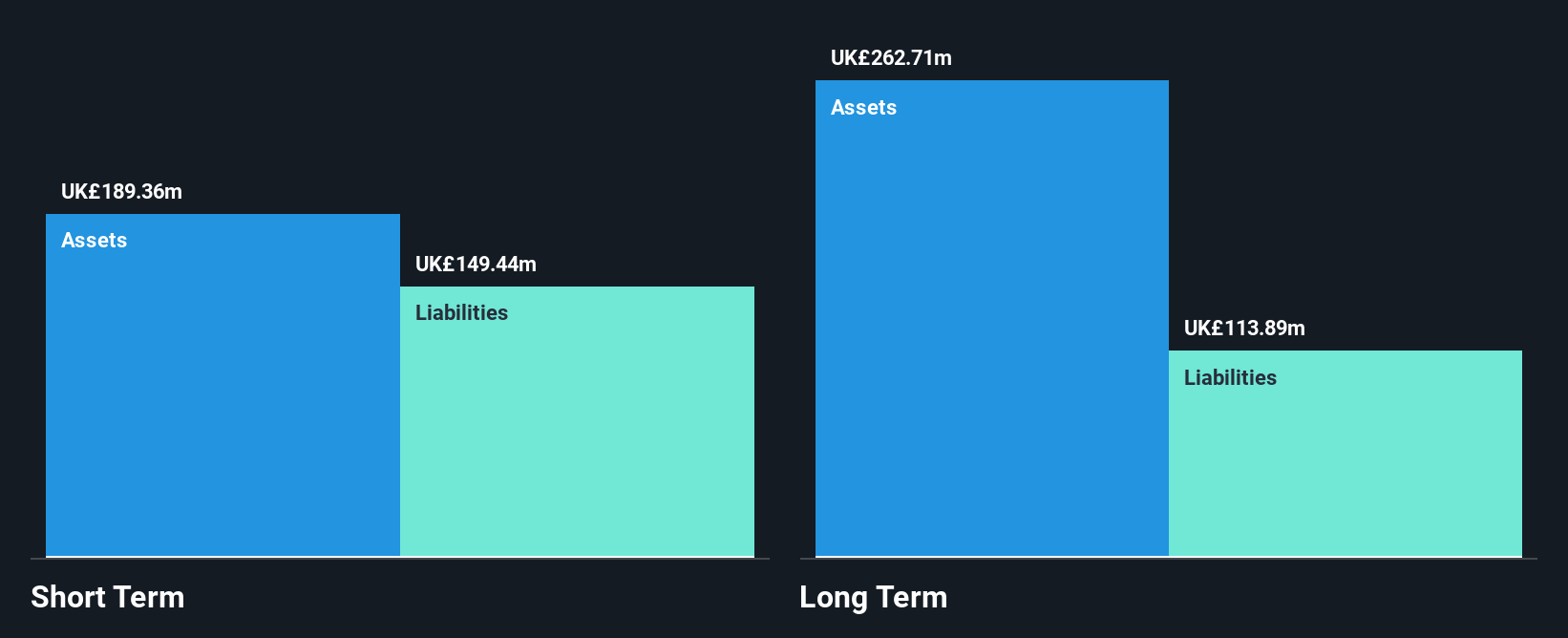

BRCK Group plc, with a market cap of £167.13 million, operates in the UK construction sector through four segments and recently reported a slight revenue increase to £645.36 million for the fiscal year ending March 31, 2026. Despite this growth, net income fell to £1.3 million from £6.53 million the previous year due to a significant one-off loss of £7.3M impacting results. The company maintains strong liquidity with short-term assets exceeding liabilities and its debt is well covered by operating cash flow (31.3%). However, management's low average tenure suggests an inexperienced team despite having an experienced board.

- Take a closer look at BRCK Group's potential here in our financial health report.

- Gain insights into BRCK Group's outlook and expected performance with our report on the company's earnings estimates.

Likewise Group (AIM:LIKE)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Likewise Group Plc, with a market cap of £84.73 million, wholesales and distributes floorcoverings, rugs, and matting products for domestic and commercial flooring markets in the United Kingdom and the rest of Europe.

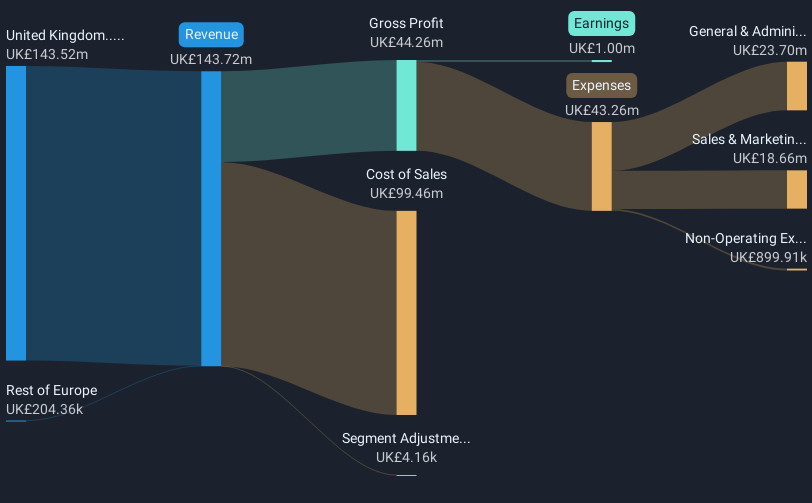

Operations: The company's revenue is primarily derived from its textile manufacturing segment, which generated £163.10 million.

Market Cap: £84.73M

Likewise Group Plc, with a market cap of £84.73 million, has shown promising growth in the UK floorcovering distribution sector. The company's revenue reached £163.1 million for the year ending December 31, 2025, with net income slightly increasing to £0.89 million despite a large one-off loss impacting results. Its short-term assets comfortably cover both short and long-term liabilities, and its debt level is satisfactory with operating cash flow covering 74.6% of debt. However, interest coverage is weak at 2.4x EBIT and Return on Equity remains low at 2%. Recent trading updates show sales growth momentum continuing into May 2026.

- Click to explore a detailed breakdown of our findings in Likewise Group's financial health report.

- Assess Likewise Group's previous results with our detailed historical performance reports.

Sabre Insurance Group (LSE:SBRE)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Sabre Insurance Group plc, with a market cap of £451.97 million, operates through its subsidiaries to provide general motor vehicle insurance in the United Kingdom.

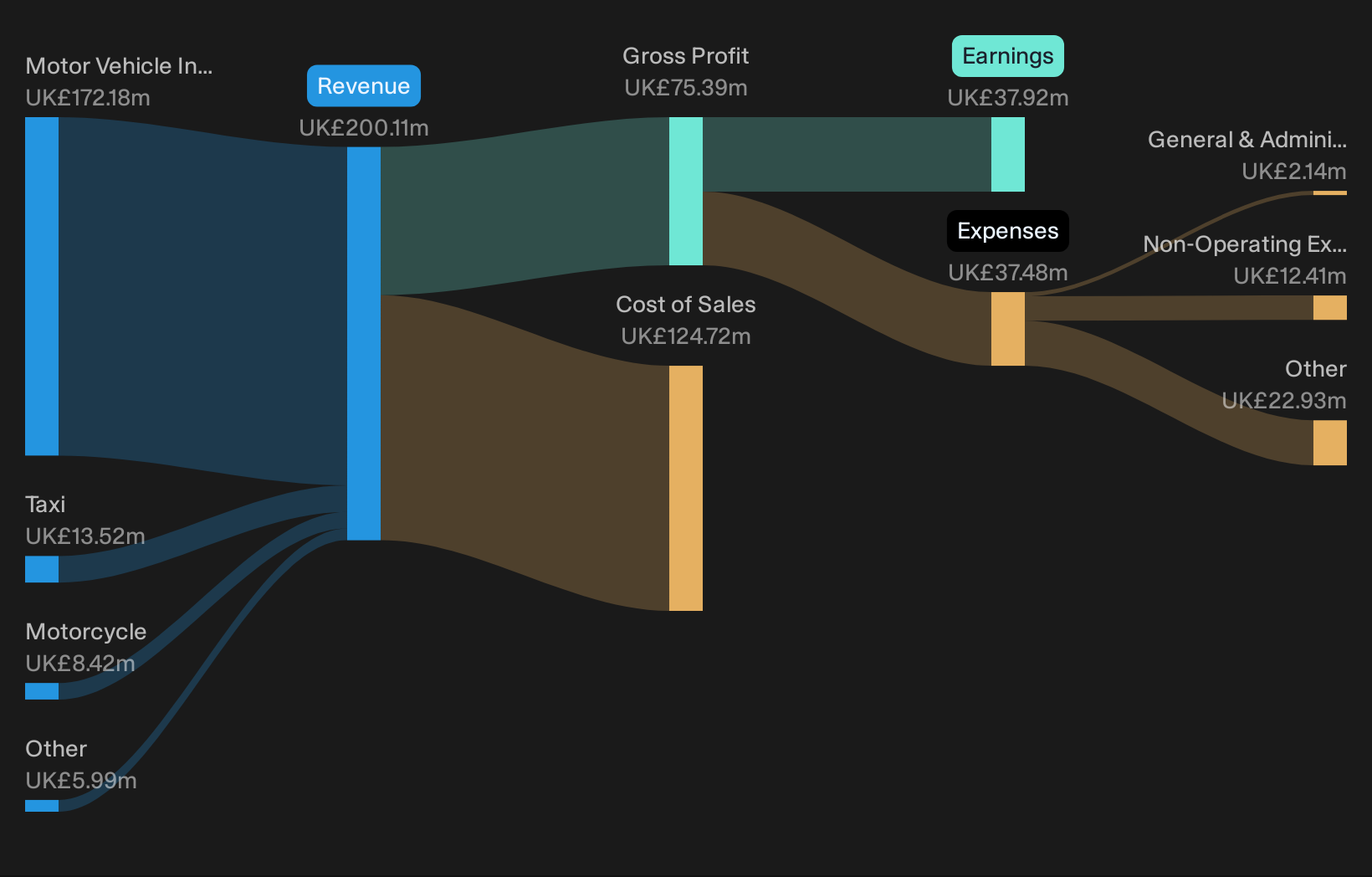

Operations: The company's revenue is primarily derived from its motor vehicle insurance segment, contributing £172.18 million, with additional income from taxi and motorcycle insurance segments at £13.52 million and £8.42 million respectively.

Market Cap: £451.97M

Sabre Insurance Group plc, with a market cap of £451.97 million, has demonstrated financial stability through its debt-free status for the past five years and high-quality earnings. However, its short-term assets (£242.9M) do not cover short-term liabilities (£467.7M), posing potential liquidity concerns. Despite trading at 47.4% below estimated fair value, the company's Return on Equity is considered low at 14.7%. Recent developments include a share repurchase program authorized to buy back up to 10% of issued shares and dividend increases approved in May 2026, reflecting efforts to enhance shareholder value amidst stable weekly volatility (4%).

- Jump into the full analysis health report here for a deeper understanding of Sabre Insurance Group.

- Examine Sabre Insurance Group's earnings growth report to understand how analysts expect it to perform.

Turning Ideas Into Actions

- Discover the full array of 275 UK Penny Stocks right here.

- Seeking Other Investments? Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com