- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

China Telecommunication Union: Electricity consumption is expected to increase by 5%-6% year-on-year in 2026

The Zhitong Finance App learned that on July 14, the China Electric Power Enterprise Federation held a press conference to officially release the “China Electric Power Industry Annual Development Report 2026”. The report predicts that in 2026, the country's electricity supply and demand will show an overall balance trend, with some regions having a tight balance in summer. Taking into account various factors, the electricity consumption of the entire national society is expected to increase by 5%-6% year on year in 2026; new energy sources will continue to be put into operation on a large scale, and the installed capacity of new energy generation is expected to exceed 400 million kilowatts throughout the year; the scale of UHV investment will continue to increase, and cross-provincial and regional capabilities will be further improved.

The “Report” shows that in 2025, the country's electricity consumption exceeded 10 trillion kilowatt-hours for the first time, an increase of 5.0% over the previous year; during the “14th Five-Year Plan” period, the electricity consumption of the entire society increased by 6.6% per year, which strongly supported an average annual GDP growth of 5.4%. China's power investment doubled during the “14th Five-Year Plan” period. The country's major power companies completed a total investment of 465.8 billion yuan in power engineering construction, an increase of 163.6% over the “13th Five-Year Plan” period. Among them, wind power and solar energy investment accounted for 62.5% of the total investment in power sources, and new energy became the main direction of power investment. A unified national electricity market system was initially established, and the market transaction scale reached a new high. In 2025, the country completed a total of 6.6 trillion kilowatt-hours of electricity transactions in the market, an increase of 7.4% over the previous year, and an increase of more than 6 times in the past ten years.

The full text of the report is as follows:

“China Electric Power Industry Annual Development Report 2026”

(Press release)

2025 is the year the 14th Five-Year Plan comes to an end. Under the strong leadership of the CPC Central Committee with Comrade Xi Jinping at the core, the power industry earnestly studied and implemented the spirit of the 20th National Congress and the Second, Third, and Fourth Plenums of the 20th CPC Central Committee, thoroughly implemented the “Four Revolutions, One Cooperation” new energy security strategy, successfully completed the goals and tasks of the “14th Five-Year Plan”, took solid steps to promote high-quality electricity development, and provided a strong and reliable power guarantee for sustainable economic and social development and a better life for the people.

In 2025, the basic development situation of the power industry is as follows:

1. The country's entire society's electricity consumption exceeded 10 trillion kilowatt-hours for the first time

In 2025, the electricity consumption of the entire nation's society was 10.4 trillion kilowatt-hours [1], an increase of 5.0% over the previous year. The scale of electricity consumption is more than double the annual electricity consumption of the United States, which is equivalent to the sum of the United States, India, Russia, Japan, Brazil, and Canada, which rank second to seventh in the world. This means that China, as a supereconomy, has moved into an era of clean, low-carbon, convenient and intelligent electrification. In July and August of last year, the electricity consumption of the entire country's society continuously exceeded 1 trillion kilowatt-hours, surpassing the annual electricity consumption of Germany and France, setting the world record for the highest monthly electricity consumption in a single country, reflecting China's ability to guarantee reliable electricity supply and stable operation control in response to a huge concentration of cooling loads in hot weather.

During the “14th Five-Year Plan” period, the electricity consumption of the whole society grew at an average annual rate of 6.6%, which strongly supported an average annual GDP growth of 5.4%. It effectively confirmed the booming development of emerging industries characterized by high growth in electricity consumption, and provided a solid foundation for China to accelerate the cultivation of new quality productivity.

II. Industrial Upgrading and Electricity Consumption Structure Optimization

In 2025, the primary sector's electricity consumption was 149.3 billion kilowatt-hours, an increase of 9.9% over the previous year, accounting for 1.4% of the electricity consumption of the entire society, contributing 2.7% to the increase in electricity consumption. The electricity consumption of the secondary sector was 6.6 trillion kilowatt-hours, an increase of 3.7% over the previous year, accounting for 64.0% of the electricity consumption of the entire society, contributing 47.6% to the increase in electricity consumption. The tertiary sector's electricity consumption was 2.0 trillion kilowatt-hours, an increase of 8.2% over the previous year, accounting for 19.2% of the electricity consumption of the entire society, contributing 30.7% to the increase in electricity consumption. The daily electricity consumption of urban and rural residents was 1.6 trillion kilowatt-hours, an increase of 6.3% over the previous year, accounting for 15.3% of the electricity consumption of the entire society, contributing 19.0% to the increase in electricity consumption.

Looking at the industrial structure, the primary sector, the tertiary sector, and residents' electricity consumption are all growing at a higher rate than the average electricity consumption of the whole society, reflecting the good trend of continuous adjustment of China's industrial structure and continuous optimization of the electricity consumption structure. In the secondary sector, the growth rate of electricity consumption in the high-tech and equipment manufacturing industry reached 6.4%, which is higher than the overall growth rate of the manufacturing industry, demonstrating that the high-tech industry is a strong driving force for economic growth.

3. The low-carbon transformation of the installed power generation structure has achieved remarkable results

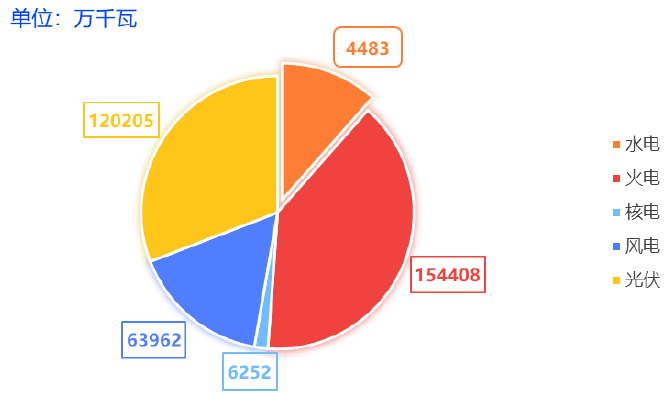

By the end of 2025, the country's installed capacity of full-caliber power generation was 3.9 billion kilowatts, an increase of 16.2% over the previous year. Among them, the installed capacity of non-fossil energy power generation was 2.40 billion kilowatts, an increase of 23.0% over the previous year, accounting for 61.6% of the total installed capacity. The installed capacity of wind power and solar power reached 1.84 billion kilowatts at the end of 2025, increasing from 25.7% at the end of 2020 to 47.3% at the end of 2025, surpassing thermal power for the first time.

Figure 1 National full-caliber power generation installed capacity structure as of the end of 2025

Looking at the new installed capacity, wind power generation accounts for about 80% of the new installed capacity. In 2025, the country added 550 million kilowatts of installed power generation capacity, an increase of 26.2% over the previous year. Of these, wind power and solar power generation added 440 million kilowatts in total, accounting for 79.7% of the total new installed capacity. In addition, the new energy storage capacity is about 62 million kilowatts/183 million kilowatt-hours, an increase of more than 40 times compared with the end of the 13th Five-Year Plan, and the flexible adjustment capacity of the power system has been further improved.

4. Further increase in the scale and quality of green electricity consumption

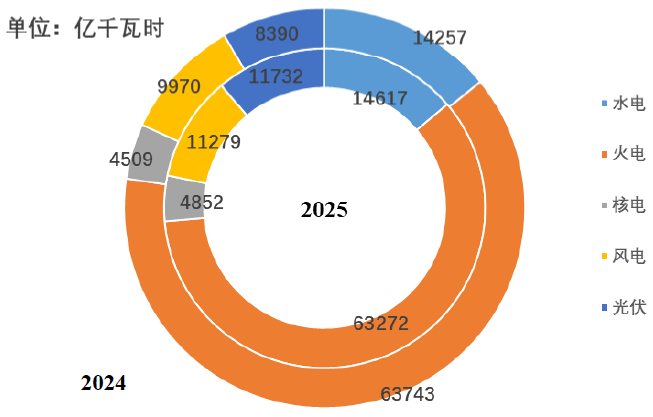

In 2025, the country's total power generation capacity was 10.6 trillion kilowatt-hours [2], an increase of 4.8% over the previous year. Among them, non-fossil energy generation reached 4.47 trillion kilowatt-hours, an increase of 14.0% over the previous year. The average annual growth rate during the “14th Five-Year Plan” period was 11.6%, accounting for 42.2% of the total power generation of full-caliber power generation. In 2025, the total solar power generation of wind power reached 2.3 trillion kilowatt-hours, accounting for 21.8%.

Figure 2 National power generation structure in 2025

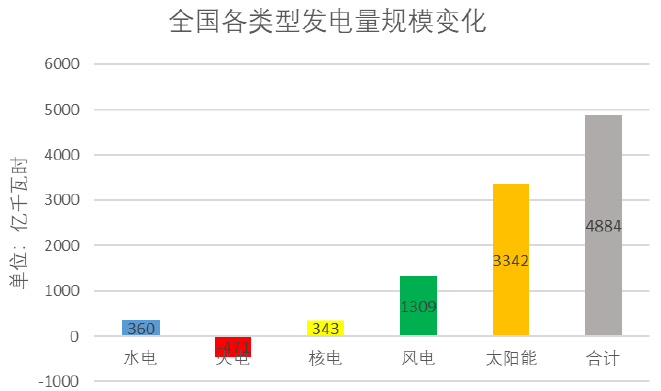

In 2025, the country's power generation capacity increased by 488.4 billion kilowatt-hours, of which new wind power and solar power generation accounted for 95.2% of the new electricity consumption of the whole society, reflecting the continuous increase in the ability of new energy sources to cover the increase in electricity consumption of the whole society, providing strong support for China's smooth “dual carbon” goal.

Figure 3 Structure chart of the country's new electricity generation capacity in 2025

5. The country's electricity transmission across provinces and regions accounts for 20.5% of the country's electricity consumption

By the end of 2025, the length of transmission lines of 35 kV and above in the national grid was 2.64 million kilometers, an increase of 8.0% over the previous year. Among them, transmission lines of 220 kV and above are 1.03 million kilometers long, an increase of 5.2% over the previous year. The capacity of substations of 35 kV and above in the national grid was 9.1 billion kilovolts, up 4.7% year on year. Of these, public substations of 220 kV and above had a capacity of 6.2 billion kVA, up 6.4% year on year. In 2025, the country completed transmission of 998.4 billion kilowatt-hours of electricity across regions, an increase of 8.0% over the previous year; the country completed 2.1 trillion kilowatt-hours of electricity transmission across provinces, an increase of 6.3% over the previous year. The country's electricity transmission across provinces and regions accounted for 20.5% of the country's electricity consumption, further showing the results of optimal utilization of national resources. At the end of the 14th Five-Year Plan period, the national AC substation capacity of 220 kV and above was 5.7 billion kilovolts, an increase of 25.0% over the end of the 13th Five-Year Plan period; the length of AC transmission lines of 220 kV and above was 970,000 kilometers, an increase of 26.4% over the end of the 13th Five-Year Plan period.

6. Overall balance of electricity supply and demand across the country

In 2025, with a number of guaranteed and supporting power supplies and multiple UHVDC transmission projects being put into operation one after another, China's power insurance and resource allocation capabilities were further enhanced. During the peak summer season, extreme heat was frequent across the country, and showed the characteristics of early, wide-ranging, and prolonged periods of time, driving the country's highest summer regulated load to 1,508 billion kilowatts, reaching a record high. Through measures such as improving power generation capacity, enhancing resource allocation, and strengthening load management, the power system successfully coped with multiple tests such as the average annual temperature reaching historic extreme values, the longest peak load duration, and frequent torrential rains and floods. The overall balance between electricity supply and demand. During the peak winter season, widespread cold weather drove the country's electricity load to rise rapidly, and short-term cold currents caused the load to rise. Relying on the successive commissioning of various supporting power supplies in 2025, and various regulatory measures such as market-based optimal allocation and mutual power support across provinces and regions, the overall balance between electricity supply and demand across the network was balanced.

7. China's power investment doubled during the “14th Five-Year Plan” period

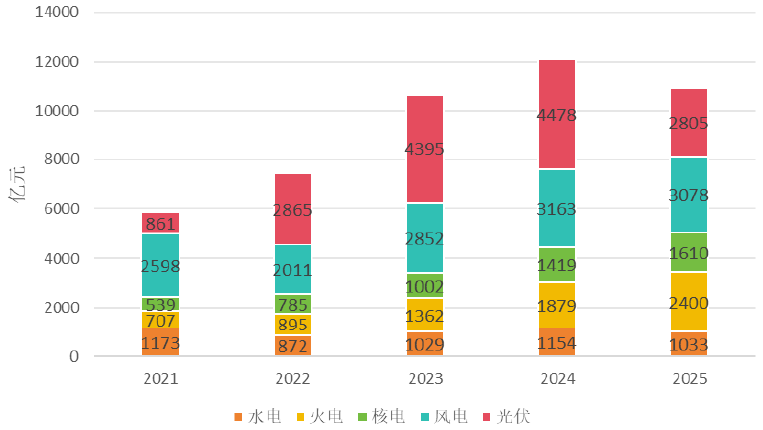

During the “14th Five-Year Plan” period, the country's major power companies completed a total investment of 4.7 trillion yuan in power engineering construction, an increase of 163.6% over the “13th Five-Year Plan” period, with an average annual investment of 931.6 billion yuan. Among them, the total investment in wind power and solar energy reached 2.9 trillion yuan, with an average annual investment of 582.1 billion yuan, accounting for 62.5% of the total investment in power supplies, reflecting the acceleration of the green and low-carbon transformation of China's energy structure during the “14th Five-Year Plan” period, and new energy sources have become the main direction of power investment.

Figure 4 Investment status of completed national power engineering construction during the “14th Five-Year Plan” period

8. The UHVDC project drives an increase in the growth rate of power grid investment, and the steady growth of investment in AC main networks and distribution networks

In 2025, the national power grid construction completed an investment of 639.5 billion yuan, an increase of 5.1% over the previous year. The DC project invested 59.9 billion yuan, an increase of 25.7% over the previous year. The investment in communication projects was 559.2 billion yuan, an increase of 3.4% over the previous year. Among them, 1000 kV grade power grids invested 14.4 billion yuan, a year-on-year decrease of 34.9%; 750 kV grade grids invested 32.8 billion yuan, up 40.8% year on year; 500 kV grade power grids invested 84.4 billion yuan, up 15.9% year on year; national 110 kV and below distribution grids invested 323.7 billion yuan, up 0.7% year on year, accounting for 50.6% of total completed grid project investment.

9. The intensity of carbon emissions per unit of electricity generation across the country continues to decline

In 2025, the country's carbon dioxide emissions per unit of electricity generation were 514 grams/kilowatt-hour, a year-on-year decrease of 2.6% and a decrease of 40.1% compared to 2005; carbon dioxide emissions per unit of thermal power generation were 823 grams/kilowatt-hour, the same as the previous year. The emission intensity of smoke, sulfur dioxide, and nitrogen oxide per unit of thermal power generation in the country was about 12 mg/kwh, 77 mg/kwh, and 125 mg/kwh, respectively, which was basically the same; the standard coal consumption for the country's 6,000 kilowatt and above thermal power plants was 301.9 g/kwh, a decrease of 0.6 g/kwh; the national grid line loss rate was 4.23%, a year-on-year decrease of 0.14 percentage points.

10. The annual quota turnover of the national carbon emissions trading market is 235 million tons, and the average transaction price is 62.36 yuan/ton

In 2025, the national carbon emissions trading market (power generation industry) operated for a total of 243 trading days, with an annual quota turnover of 235 million tons, an increase of about 24% over the previous year, with a turnover of 14.630 billion yuan. The average transaction price for the whole year was 62.36 yuan/ton. Among them, the bulk agreement transaction model is the main one, accounting for about two-thirds. Since the opening of the national carbon emissions trading market until December 31, 2025, the cumulative turnover of quota (CEA) was 865 million tons, with a cumulative turnover of 57.663 billion yuan.

As of December 31, 2025, the National Greenhouse Gas Voluntary Emission Reduction Trading Market has registered 33 voluntary emission reduction projects, reducing emissions by 17.7637 million tons. The cumulative turnover of certified voluntary emission reductions was 9.2194 million tons, with a turnover of 650 million yuan. The average transaction price for the whole year was 70.76 yuan/ton. A total of 6106 accounts have been opened in the registration system, covering legal entities such as project owners, key emission units, and financial institutions.

11. The average power supply reliability rate for power supply system users across the country is 99.931%

In 2025, the equivalent availability coefficient of all types of generator sets in the country exceeded 91.7%, of which hydropower was 93.71%, down 0.07 percentage points; coal power was 92.14%, up 0.10 percentage points year on year; gas power was 91.74%, down 0.56 percentage points year on year; nuclear power was 92.77%, up 1.98 percentage points year on year; wind power was 98.93%, up 0.48 percentage points year on year; photovoltaic power generation was 99.89%, up 0.05 percentage points year on year. In terms of power transmission and transformation, the usability coefficient of Class 11 transmission and transformation facilities with a voltage rating of 220 kV and above included in electricity reliability statistics remained above 97.5%, with transformers 99.345%, down 0.069 percentage points from year on year; circuit breakers were 99.742%, down 0.027 percentage points year on year; and overhead lines were 99.629%, down 0.048 percentage points year on year. In terms of DC transmission, the number of DC transmission systems included in electricity reliability statistics and in operation throughout the year was 51. The total energy availability rate was 97.395%, up 1.593 percentage points from the previous year; the energy utilization rate was 51.75%, an increase of 3.00 percentage points over the previous year. In terms of power supply, the average power supply reliability rate for power supply system users across the country was 99.931%, an increase of 0.007 percentage points over the previous year; the average power outage time for users was 6.04 hours/household, a decrease of 0.67 hours/household over the previous year.

12. Accelerate the forging of national strategic scientific and technological strength in the field of energy and electricity

In 2025, the power industry will vigorously implement innovation-driven development strategies, actively undertake major national scientific research tasks, accelerate research on original technology, and compete for scientific and technological innovation achievements. In the field of power generation, the world's largest 26 megawatt offshore wind turbine was successfully connected to the grid, setting two records for the world's stand-alone capacity and impeller diameter for grid-connected fans; the world's largest 5,000 square meter high-altitude wind power umbrella successfully opened, marking a solid step in the engineering application of China's high-altitude wind power generation technology. In the field of power grids, the world's first ±800 kV/8 million kW controllable commutation converter valve (CLCC) has successfully passed all tests and verifications, marking that China has taken the lead in overcoming the “commutation failure” problem that has plagued the UHV/UHVDC transmission field for more than half a century. In the field of energy storage, China's largest all-vanadium liquid flow battery energy storage power plant has been put into operation at full capacity, marking an important breakthrough in the application of high-capacity, long-term energy storage technology in China. In 2025, major power companies invested 19.08 billion yuan in technology, authorized 60,000 domestic and foreign patents, published 44,000 papers, and drafted a total of 4,314 technical standards.

13. The integration of artificial intelligence and digitalization promotes the construction of new power systems

In 2025, the power industry will closely follow the implementation requirements of the national “Artificial Intelligence +” strategy, and will use the construction of new power systems and the cultivation of new quality productivity as a starting point to further promote the digitalization and intelligent upgrading of the entire industry chain. The power supply sector continues to deepen digital transformation, using digital technology to seize strategic opportunities for energy transformation, target breaking down industry development bottlenecks, and provide hard core technical support for scientific research and judgment of projects, market-based electricity transactions, and intelligent operation and maintenance of the entire life cycle of the unit. The power grid field is based on the construction of new power systems and the cultivation of new quality productivity, using artificial intelligence as an important gripper for the intelligent transformation of power grids, deepening the systematic layout, accelerating large-scale application of artificial intelligence in planning, equipment, marketing, etc., and promoting the intelligent transformation and upgrading of power grids. In 2025, major power companies invested 42.94 billion yuan in digitalization, and the number of patents, software copyrights, and awards in the field of power digitalization was more than 9900, 7300, and 2,300, respectively.

14. A unified national electricity market system was initially established, and the scale of market transactions reached a new high

In 2025, the country completed a total of 6.6 trillion kilowatt-hours of electricity transactions, an increase of 7.4% over the previous year, and an increase of more than 6 times in the past ten years; market transactions accounted for 64.0% of the electricity consumption of the whole society, and the market-based rate achieved positive growth for 10 consecutive years. More than 60% of the country's electricity traded across provinces and regions was allocated through market-based transactions; the country's market-traded electricity volume across provinces and regions was close to 1.6 trillion kilowatt-hours, an increase of 11.6% over the previous year. The role of market optimization in implementing electricity resource allocation on a wider scale continues to be prominent; the country's green power trade volume is 328.5 billion kilowatt-hours, which is a year-on-year increase of 38.3%. 18 times that of 2022.

The construction of provincial markets has been accelerated across the board, and the electricity spot market has basically achieved nationwide coverage. In 2025, the electric power spot markets in Mengxi, Hubei, and Zhejiang were officially put into operation one after another. In addition to the Tibet region, electricity spot market transactions have covered 28 provinces (districts and cities) across the country. The southern regional electricity market took the lead in continuous operation, and optimized allocation of electricity resources in the five southern provinces and regions was achieved by unifying the entire region. Cross-grid business area transactions have achieved historic breakthroughs, and for the first time, “Three North Scenery Illuminates the Greater Bay Area” and “Southwest Green Power Delivery to the Yangtze River Delta” has been achieved.

The power business revenue of the 15 and 5 major power generation groups declined slightly

In 2025, the total main business revenue of the three power grid companies was 4.95 trillion yuan, up 1.6% year on year; total profit was 155 billion yuan, up 14.5% year on year. The electricity business revenue of the five major power generation groups was 1.57 trillion yuan, a year-on-year decrease of 1.0%; the total profit from the power business was 177 billion yuan. In 2025, coal-fired power plants across the country received a total of 10.6 billion yuan in electricity costs, and the discounted electricity price was 30.1 yuan/megawatt-hour.

16. New energy projects have an absolute advantage in foreign investment

By the end of 2025, China's major power companies had 57 OFDI projects, with a total investment amount of US$2,976 billion. The investment sector covers a wide range of energy tracks such as solar power generation, wind power, energy storage, hydropower, gas power, etc., and the investment structure continues to lean towards clean and low-carbon fields. Judging from the scale of investment, there is a clear division of investment in various fields. The highest investment amount for solar power generation was US$1,310 million, wind power was US$805 million, energy storage was US$486 million, and hydropower was US$279 million. In terms of the number of projects, new energy projects have an absolute advantage. There are a total of 40 projects, accounting for about 76.5% of the total. Of these, solar photovoltaic power generation accounts for 49% and wind power accounts for 21%.

17. The scale and market share of foreign-contracted engineering business reached a new high

By the end of 2025, the total amount of overseas project contracts for major Chinese power companies had exceeded 470 billion US dollars. In 2025, China's major power companies signed 194 new engineering contract projects a year, with a total contract amount of US$36.510 billion, an increase of 12.45% over the previous year. Major Chinese power companies signed a total of 147 large-scale overseas projects with a contract value of 50 million US dollars or more, an increase of 45 over 2024. The total contract amount was 35.839 billion US dollars, an increase of 14.27% over the previous year.

In 2026, the country's electricity supply and demand showed an overall balance trend, and the balance was tight in some regions in summer. Taking into account the outline of the 15th Five-Year Plan for National Economic and Social Development, the country's macro-control policies and measures, and China's current economic growth situation, it is estimated that in 2026, the electricity consumption of the entire country will increase by 5% to 6% year on year, adding about 400 million kilowatts of new power generation. New energy will still be the main source of new power installations, adding about 100 million kilowatts of conventional power, which is basically the same as the maximum load increase.

The scale of UHV investment continues to increase. It is expected that multiple UHV AC projects will be put into operation within 2026, and cross-provincial and regional capabilities will be further enhanced. Taking into account the growth in demand, the commissioning of power grids, and the primary energy situation, it is estimated that in 2026, the balance between electricity supply and demand will be tight in some provinces during the peak summer season. If widespread extreme weather or primary energy supply is tight, the electricity supply and demand situation in some regions is tight during certain periods. Both supply and demand sides need to work together to make good use of the remaining gaps between provinces and regions to ensure the safe and stable operation of the system and the reliable and orderly supply of electricity.

Note:

[1] In addition to power generation data, other electricity data is obtained from the China Telecommunication Union's 2025 statistics (“Annual Report Data” for short). Some of the data are not equal to the total sum of the items due to rounding.

[2] The power generation data comes from the “Statistical Bulletin on National Economic and Social Development 2025 of the People's Republic of China”.