- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Rakuten Stock And 2 Japanese Growth Names With Strong Insider Alignment

With bond yields reacting to geopolitical tension, energy prices in focus, and inflation data shaping interest rate expectations across the US, Europe, and emerging markets, many investors are looking for companies that are still aiming for growth and where management has real skin in the game. The Fast Growing Stocks With High Insider Ownership screener focuses on businesses that analysts and company leadership view with optimism, which can help align management’s interests with shareholders. In this article, you will see 3 stocks from this screener that illustrate how this theme can fit into a growth focused portfolio approach.

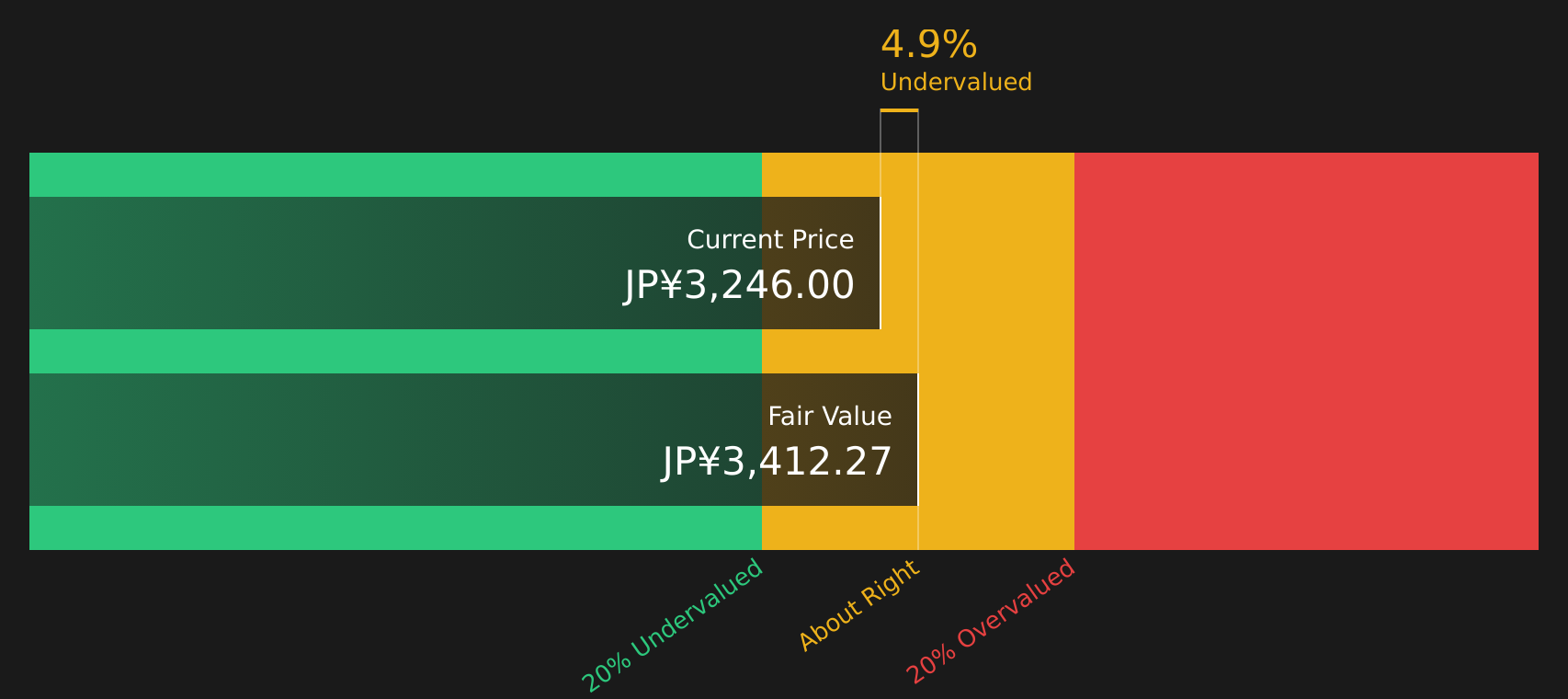

Capcom (TSE:9697)

Overview: Capcom is a Japanese video game company that creates and sells home console and mobile games such as action, fighting, and horror titles, and also operates and supplies amusement arcades, machines, and character based businesses across Japan, the United States, Europe, and other regions.

Operations: Capcom generates most of its revenue from Digital Content at ¥144,277 million, with additional contributions from Arcade Operations at ¥25,656 million, Amusement Equipment at ¥17,780 million, and Other activities at ¥7,650 million, and geographically earns across Japan (¥64,129 million), the United States (¥53,199 million), Europe (¥33,456 million), and other markets (¥44,579 million).

Market Cap: ¥1.39t

Capcom is included in this growth and insider ownership theme because it combines strong profitability with a deep catalog of globally recognised franchises that support earnings and cash flow. Reported net profit margins of around 27.9% and a high ROE of roughly 20% sit alongside analyst expectations for earnings and revenue that are ahead of the wider Japanese market. At the same time, the stock is described as trading slightly below one DCF based fair value estimate and analyst targets are reported to sit above the current price. A richer P/E versus peers, reliance on a few flagship series, and funding that leans on external borrowing mean investors still need to weigh valuation, concentration, and balance sheet risks carefully.

Capcom’s rich P/E, high margins, and globally recognised franchises suggest a story that many investors may only be seeing half of, so it is worth reviewing the 4 key rewards and 1 important major warning sign

Kasumigaseki CapitalLtd (TSE:3498)

Overview: Kasumigaseki CapitalLtd is a Tokyo based real estate consulting company that develops and operates solar power generation projects, logistics and warehousing facilities, and apartment hotels under its fav, FAV LUX, and seven x seven brands, while also providing healthcare facilities and running overseas operations.

Operations: Kasumigaseki CapitalLtd generates its revenue from the Real Estate Consulting Business, which contributed ¥134,428 million, all from Japan.

Market Cap: ¥166.62b

Kasumigaseki CapitalLtd catches attention because it ties high growth expectations to core real asset exposure in logistics, renewable energy, and hospitality. Earnings and revenue are both forecast to grow much faster than the broader Japanese market, and recent guidance points to sizeable targets for sales and profit in the coming years. At the same time, investors need to weigh that momentum against an elevated P/E versus peers, higher share price volatility, and a balance sheet where debt is not well covered by operating cash flow. Recent shareholder dilution and frequent board changes add governance questions that sit alongside an experienced management team. This makes it a stock where the headline growth story is only part of what matters.

Kasumigaseki CapitalLtd’s growth story looks powerful on the surface, but the real question is how those ambitions stack up against its valuation and balance sheet pressures. Before you decide how it fits into your portfolio, review the 3 key rewards and 3 important warning signs (1 is major!)

Rakuten Group (TSE:4755)

Overview: Rakuten Group is a Japanese digital services company that runs a large e-commerce marketplace, online travel and content platforms, and a broad fintech suite that includes credit cards, banking, securities, insurance, and payments, alongside a growing mobile telecom business and various advertising, energy, and sports related activities in Japan and overseas.

Operations: Rakuten Group generates revenue mainly from Internet Services at ¥1.38t, FinTech at ¥1.03t, and Mobile at ¥503.29b, partly offset by intercompany transactions of ¥335.38b.

Market Cap: ¥1.75t

Rakuten Group sits at the crossroads of e-commerce, finance, and telecom, with an ecosystem that ties shopping, payments, and mobile into a single loyalty driven platform and a P/S of 0.7x that suggests the market still has questions about how quickly this can translate into steady profits. Earnings are currently in loss territory and debt funded mobile investment is weighing on results. Analysts have outlined a potential path to profitability over the next few years, referencing improving margins, AI driven efficiencies, and tighter capital management. Long running partnerships such as the Golden State Warriors deal highlight how management is still investing in global brand awareness, so investors who understand both the funding risks and ecosystem potential may find this a story worth following closely.

Rakuten Group’s ecosystem story looks like it could be bigger than its current P/S of 0.7x suggests, so it may be worth reviewing the analyst forecasts for Rakuten Group to see what might be missing from the picture.

The three stocks in this article are only a starting point, as the full Fast Growing Stocks With High Insider Ownership screener on Simply Wall St surfaced 93 more companies with equally compelling growth and insider alignment stories through the Fast Growing Stocks With High Insider Ownership screener. Use the platform to analyze and filter these stocks by the specific catalysts, insider ownership levels, and analyst narratives that matter most to you, so you can identify the highest conviction ideas more efficiently.

Take Control of Your Investment Journey

If Kasumigaseki CapitalLtd or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh stock ideas can move from quiet to breakout quickly, and the strongest stories rarely stay under the radar for long. Use these screeners while it matters and act now.

- Spot companies where income momentum meets resilience by scanning a curated mix of high yielding stocks through the 44 dividend fortresses.

- Hunt for under the radar strength by checking a carefully filtered list of solid balance sheet and fundamentals (38 results) that may handle shocks better than the broader market.

- Position ahead of the next infrastructure wave by reviewing a focused set of 34 power grid technology and infrastructure stocks that could benefit if grid upgrades gain momentum.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com