- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Nippon Yusen Kabushiki Kaisha (TSE:9101) Investor Day Puts Logistics Growth Valuation In Focus

Nippon Yusen Kabushiki Kaisha (TSE:9101) recently held an Analyst and Investor Day focused on the growth strategy for its logistics business and the status of acquired operations, giving shareholders fresh detail on management priorities.

See our latest analysis for Nippon Yusen Kabushiki Kaisha.

The recent Analyst and Investor Day comes after a mixed stretch for Nippon Yusen Kabushiki Kaisha, with the share price up 7.54% year to date but down 8.90% over 90 days. At the same time, longer term total shareholder returns of 87.67% over three years and a very large 5-year gain indicate momentum has been built over time.

If this update has you thinking more broadly about logistics, shipping, and infrastructure, it could be a useful moment to see what else is moving across 11 top founder-led companies

Nippon Yusen Kabushiki Kaisha appears to be a deep, diversified logistics and shipping business, and recent share moves have been mixed. Do those fundamentals line up with what investors are being asked to pay for the stock today?

Most Popular Narrative: 6.2% Undervalued

At a last close of ¥5,506 versus a narrative fair value of about ¥5,870, Nippon Yusen Kabushiki Kaisha is framed as modestly undervalued with a relatively detailed earnings roadmap behind that view.

The analysts have a consensus price target of ¥5,869.55 for Nippon Yusen Kabushiki Kaisha based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥7,400.0, and the most bearish reporting a price target of just ¥3,440.0.

Want to see what sits behind that valuation gap? Revenue pacing, margin compression and a higher future earnings multiple all play a part. The exact mix may surprise you.

Result: Fair Value of ¥5,869.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear risks to this undervalued narrative, including weaker freight markets in energy and logistics, as well as potential disruption from geopolitical tensions on key shipping routes.

Find out about the key risks to this Nippon Yusen Kabushiki Kaisha narrative.

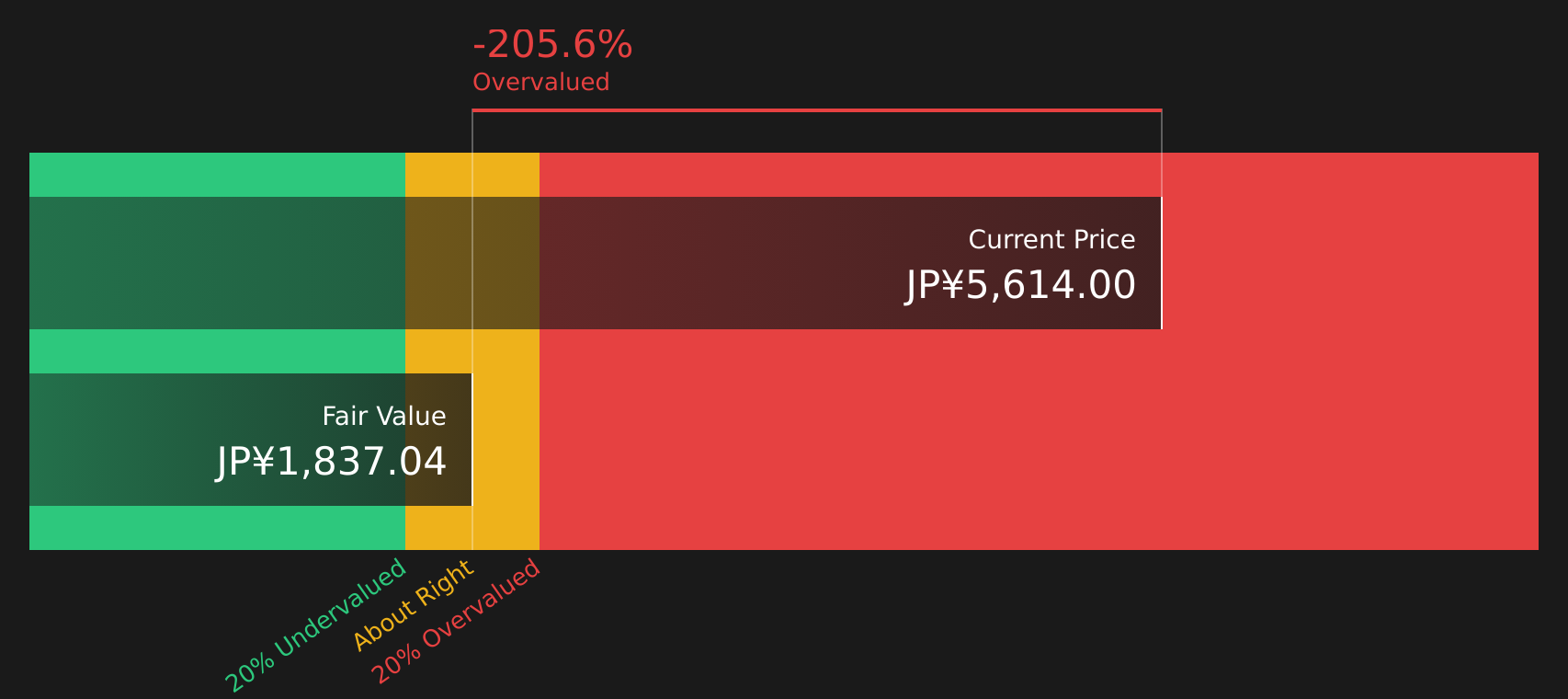

Another View: SWS DCF Model Points to Overvaluation

While analyst targets frame Nippon Yusen Kabushiki Kaisha as modestly undervalued, the SWS DCF model sends a very different message. On that approach, fair value is estimated at about ¥1,836 per share, well below the current ¥5,506, which implies the stock screens as materially overvalued. Which story do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nippon Yusen Kabushiki Kaisha for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 19 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Confused by the mix of optimism and caution around Nippon Yusen Kabushiki Kaisha? Take a closer look at the data, balance the potential upside against the flagged concerns, and see how the story of 1 key reward and 4 important warning signs fits with your own risk tolerance through 1 key reward and 4 important warning signs

Looking for more investment ideas beyond Nippon Yusen Kabushiki Kaisha?

If Nippon Yusen Kabushiki Kaisha has sharpened your focus, do not stop here. Broaden your watchlist with other clear, data backed ideas that fit your style.

- Target income potential by reviewing companies in the 44 dividend fortresses that aim to pair higher yields with solid underlying business profiles.

- Look for potential bargains by scanning the screener containing 58 high quality undiscovered gems before they attract wider market attention.

- Prioritise resilience by focusing on the 54 resilient stocks with low risk scores to see which stocks score well on Simply Wall Street's risk framework.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com