- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Oracle (ORCL) Stock May Trade At A Discount On Earnings But A Premium On AI Spending

Oracle stock has fallen sharply in recent months even as many analysts still see it screening as undervalued relative to peers, which puts the recent price weakness and the current valuation picture directly at odds.

- Over the past 5 years, Oracle has returned about 61.8%, which suggests that longer term holders are still ahead despite the recent pullback.

- Heavy investment in AI cloud capacity and data centers can support long term growth expectations, but it also raises questions about capital intensity and profitability if those projects do not generate the anticipated cash flows.

- On Simply Wall St's checks, Oracle scores 5 out of 6, which means the broader valuation framework leans toward the stock looking cheap rather than fully priced.

The stock's next move may depend on whether the recent sell off has already absorbed the key risks around AI spending and balance sheet pressure, or if investors are still overpaying for Oracle's growth story.

Find out why Oracle's -42.0% return over the last year is lagging behind its peers.

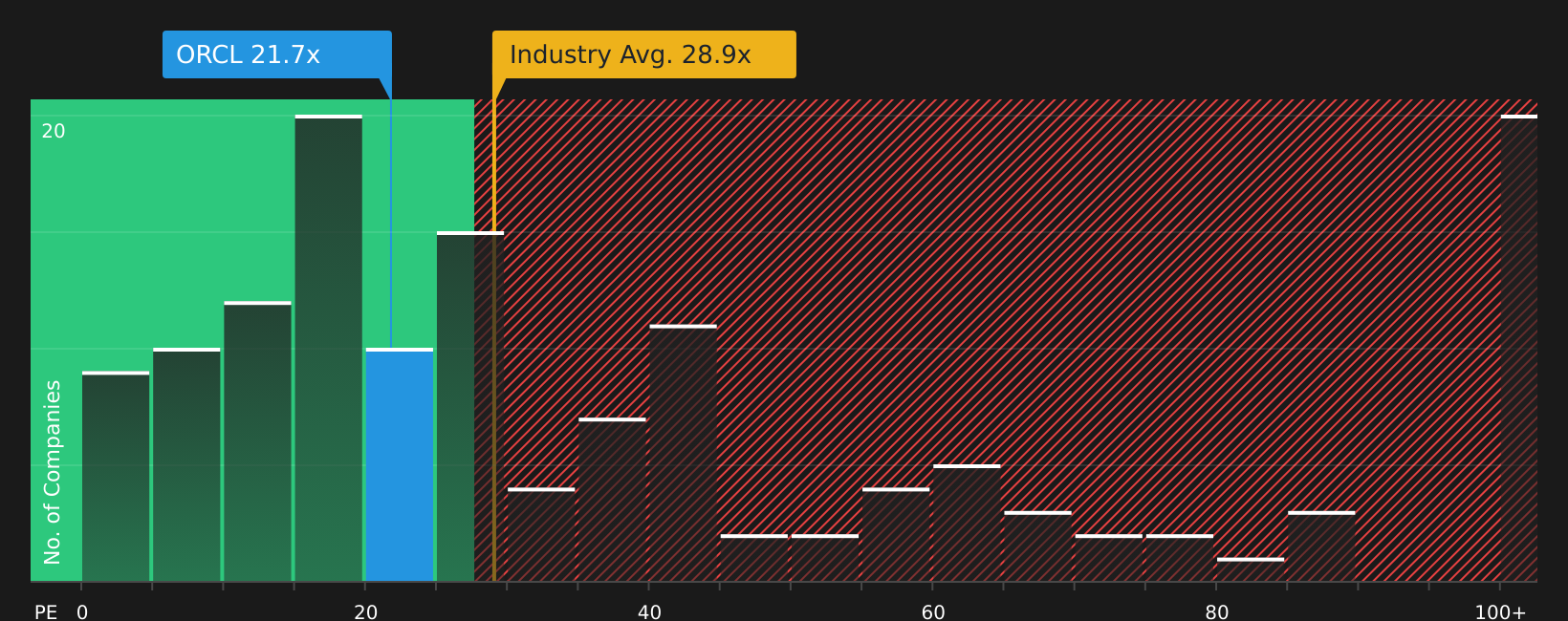

Is Oracle a Bargain on Earnings?

The P/E multiple is a useful yardstick for Oracle because earnings remain a central focus for investors in mature software and cloud companies. Oracle trades on a P/E of 22.3x, which sits below both the broader software industry average of 28.8x and the peer group average of 41.2x. On a simple comparison, the stock is priced at a discount to what many similar software and cloud businesses currently command.

Simply Wall St's fair P/E ratio for Oracle is 54.7x, based on its specific mix of growth drivers, margins, scale and risk profile. That is more than double the current 22.3x, suggesting the market is applying a sizable discount relative to what this framework would imply. Despite recent headlines around heavy AI data center spending and cautious sentiment toward hyperscalers, Oracle still trades below both sector benchmarks and this tailored fair multiple.

On earnings, Oracle stock appears undervalued on this measure, with its current P/E sitting well under both sector norms and the fair ratio implied by its business profile.

See what the numbers say about this price — find out in our valuation breakdown.

The Oracle Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where Oracle's valuation puzzle leaves off by explaining which combinations of future growth, margins and earnings would need to hold for the stock to be worth materially more or materially less than its current price. Rather than stopping at a single output from a ratio or model, they map the underlying assumptions so you can monitor whether Oracle's actual progress continues to align with that implied future on the Community page.

The community is split on Oracle, with one camp leaning into an aggressive AI buildout story and the other questioning how much of that is already reflected in expectations.

Bull case: 66% undervalued

"Oracle’s story is one of a rapid, aggressive transition from enterprise stalwart to AI infrastructure leader, where the OpenAI partnership validated the underlying technology..."

Read the full Bull Case to see why Oracle could be undervalued

Bear case: 10% overvalued

"That’s where Oracle Corporation may quietly be one of the biggest beneficiaries of the AI boom, the market still largely sees Oracle as a legacy database company..."

Read the full Bear Case to see why Oracle could be overvalued

Do you think there's more to the story for Oracle? Head over to our Community to see what others are saying!

The Bottom Line

For investors looking at Oracle today, the key point is that the stock still screens as undervalued on earnings, with its current P/E sitting below sector and peer benchmarks as well as the tailored fair ratio discussed above. That discount only matters if Oracle’s AI and cloud buildout can translate into sustainable earnings that justify a higher multiple. The crux of the debate is whether current AI infrastructure spending ultimately supports durable profitability, or whether the lower multiple is the market’s way of pricing in execution and balance sheet risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com