- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

3 Global Growth Stocks With Strong Insider Confidence

Amidst a backdrop of geopolitical tensions and market volatility, global growth stocks have shown resilience, with the Nasdaq Composite and S&P 500 indices making gains despite challenges such as rising oil prices and renewed U.S.-Iran hostilities. In this environment, companies with high insider ownership can signal strong internal confidence in their growth prospects, making them appealing options for investors seeking to navigate uncertain times.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Shanghai Biren Technology (SEHK:6082) | 11% | 116.9% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| Meitu (SEHK:1357) | 22.8% | 31.4% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| KebNi (OM:KEBNI B) | 11.8% | 90.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| CD Projekt (WSE:CDR) | 35.2% | 29.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

Let's uncover some gems from our specialized screener.

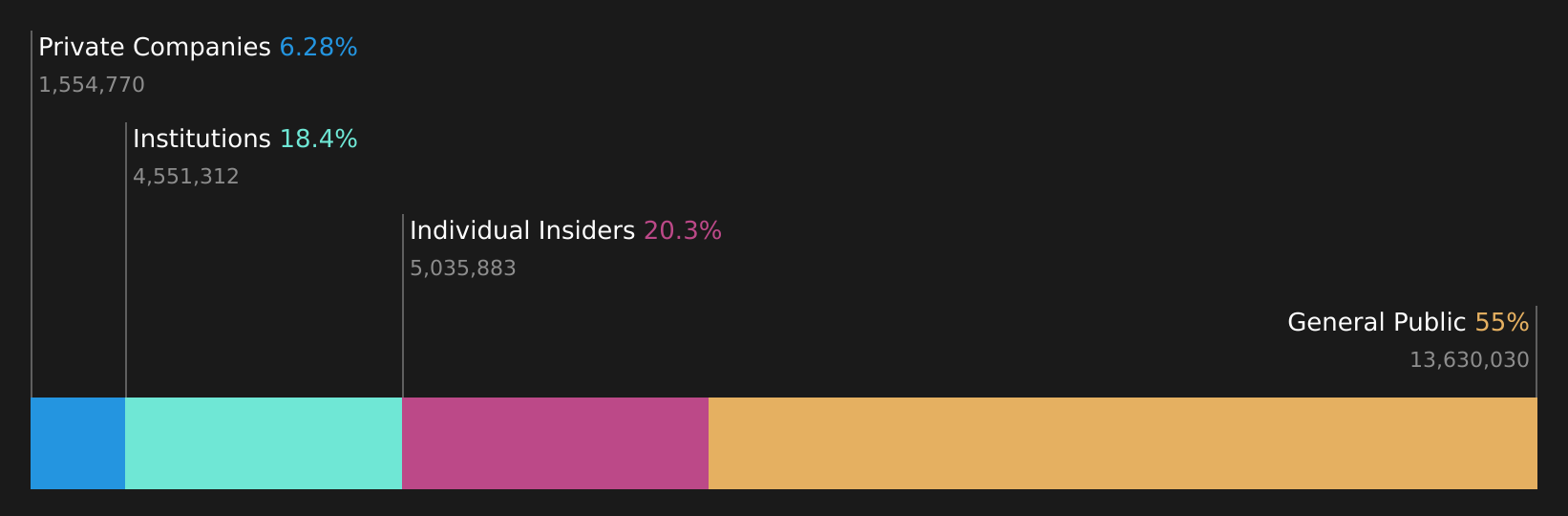

VM (KOSDAQ:A089970)

Simply Wall St Growth Rating: ★★★★★☆

Overview: VM Inc. manufactures and sells dry etcher systems for semiconductor production processes in South Korea and internationally, with a market cap of ₩2.39 trillion.

Operations: The company's revenue is primarily derived from its Semiconductor Equipment and Services segment, which generated ₩215.40 billion.

Insider Ownership: 20.3%

Revenue Growth Forecast: 25.6% p.a.

VM Inc. demonstrates strong growth potential with revenue expected to increase by 25.6% annually, outpacing the Korean market's average. Despite high share price volatility, its earnings grew significantly by a very large percentage over the past year and are forecasted to grow at 31.1% per year moving forward. Recent earnings reports showed a substantial rise in net income to KRW 25,581.71 million from KRW 1,565.22 million a year ago, indicating robust profitability improvements without recent insider trading activity influencing stock dynamics.

- Dive into the specifics of VM here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that VM is priced higher than what may be justified by its financials.

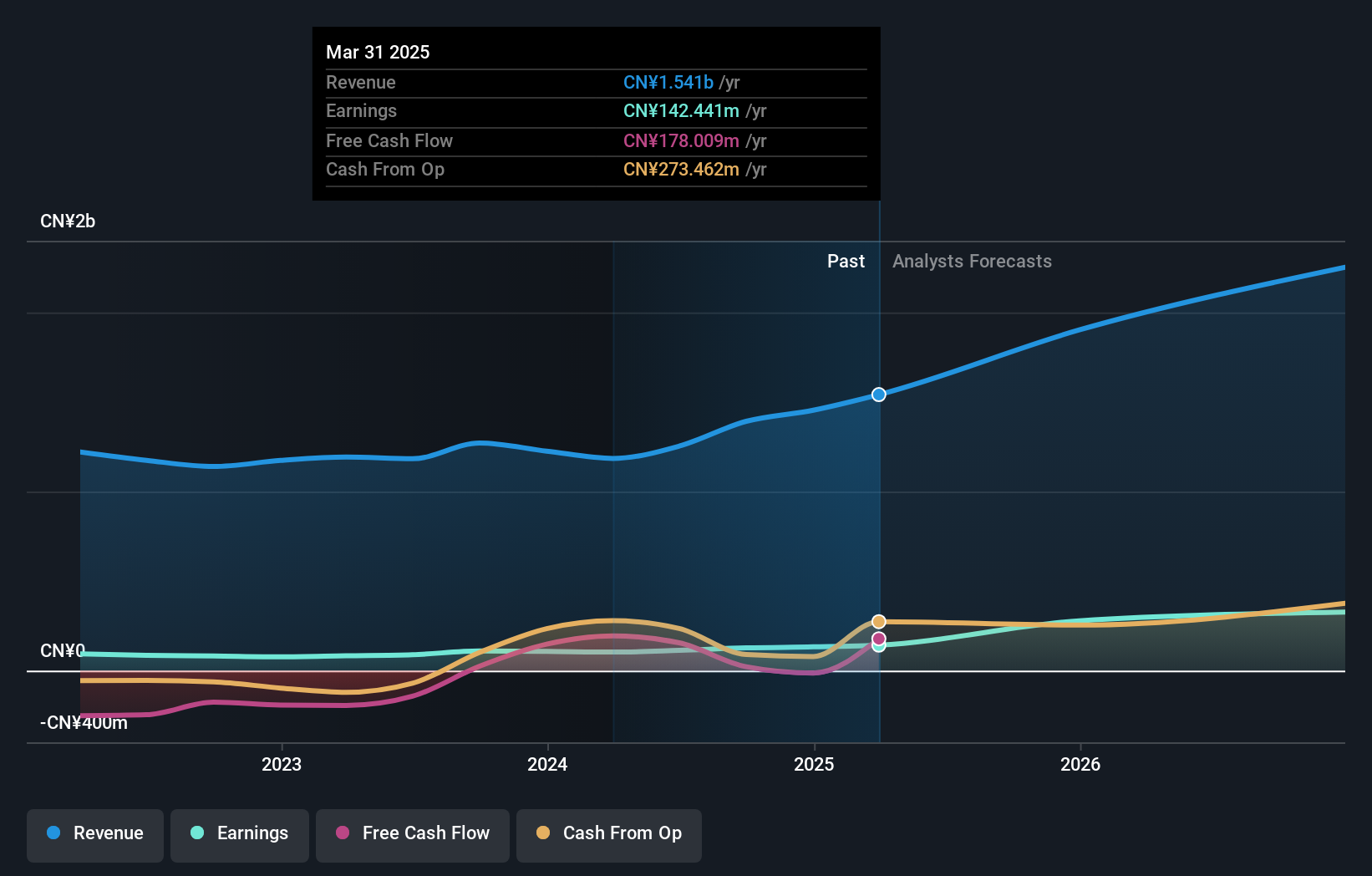

Shenzhen JPT Opto-Electronics (SHSE:688025)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen JPT Opto-Electronics Co., Ltd. focuses on the research, development, production, and sales of lasers for precision testing of integrated circuits and semiconductor optoelectronic devices, with a market cap of CN¥37.30 billion.

Operations: The company's revenue primarily comes from its Computer Communications and Other Electronic Equipment segment, which generated CN¥2.39 billion.

Insider Ownership: 24.7%

Revenue Growth Forecast: 28.3% p.a.

Shenzhen JPT Opto-Electronics is experiencing rapid growth, with first-quarter revenue rising to CNY 660.86 million from CNY 342.86 million a year ago and net income reaching CNY 97.68 million from CNY 36.05 million, reflecting strong profitability gains. The company's earnings are projected to grow significantly at 36.53% annually, surpassing the Chinese market average of 27.3%. Despite high share price volatility and low forecasted return on equity, insider activity remains stable with no significant recent trading events impacting stock behavior.

- Unlock comprehensive insights into our analysis of Shenzhen JPT Opto-Electronics stock in this growth report.

- In light of our recent valuation report, it seems possible that Shenzhen JPT Opto-Electronics is trading beyond its estimated value.

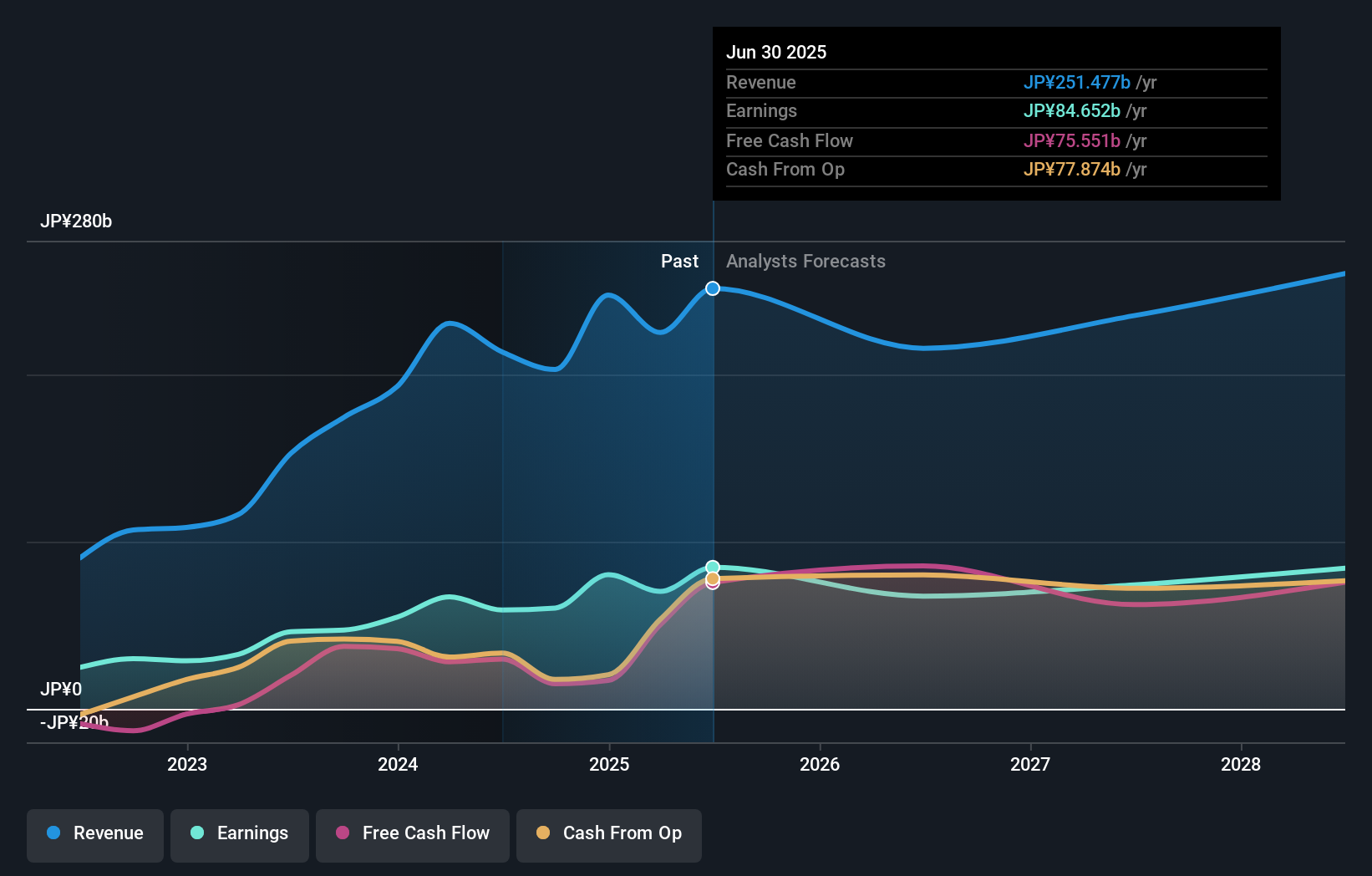

Lasertec (TSE:6920)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lasertec Corporation designs, manufactures, and sells inspection and measurement equipment across Japan, South Korea, Taiwan, other parts of Asia, and the United States with a market cap of ¥4.01 trillion.

Operations: The company's revenue is derived entirely from its inspection and measurement equipment segment, totaling ¥252.18 billion.

Insider Ownership: 11.1%

Revenue Growth Forecast: 16.1% p.a.

Lasertec Corporation's earnings for the nine months ended March 31, 2026, show a net income increase to JPY 56.82 billion from JPY 52.69 billion year-over-year, with basic earnings per share rising to JPY 632.49. Revenue growth is forecast at 16.1% annually, outpacing the Japanese market average of 6.5%. Earnings are expected to grow at a rate of 16.87%, exceeding the market's projected growth of 10.1%. Despite high share price volatility, insider trading activity remains stable without substantial recent transactions impacting stock behavior.

- Delve into the full analysis future growth report here for a deeper understanding of Lasertec.

- The valuation report we've compiled suggests that Lasertec's current price could be inflated.

Where To Now?

- Dive into all 705 of the Fast Growing Global Companies With High Insider Ownership we have identified here.

- Ready For A Different Approach? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com