- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Undiscovered Gems in Global Markets for July 2026

As global markets navigate the complexities of Middle East tensions and volatile energy prices, major U.S. indices have shown mixed results with small-cap stocks facing particular challenges, as evidenced by the Russell 2000's recent decline. Amid these fluctuations, investors often seek out lesser-known opportunities that can offer potential growth despite broader market uncertainties. Identifying such undiscovered gems typically involves looking for stocks with strong fundamentals and innovative strategies that may thrive even in unpredictable economic climates.

Top 10 Undiscovered Gems With Strong Fundamentals Globally

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Base | NA | 11.66% | 17.63% | ★★★★★★ |

| GROUPE SFPI | 18.02% | 4.25% | -29.76% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Fourth Milling | NA | 8.33% | 16.85% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

China Banking (PSE:CBC)

Simply Wall St Value Rating: ★★★★★★

Overview: China Banking Corporation offers a range of banking and financial products and services to individuals and businesses in the Philippines, with a market capitalization of ₱152.20 billion.

Operations: China Banking Corporation generates revenue through its diverse range of banking and financial services offered to individuals and businesses in the Philippines. The company has a market capitalization of ₱152.20 billion.

China Banking Corporation, a promising player in the financial sector, shows solid performance with earnings growth of 11.2% over the past year, outpacing the industry average of 5.5%. The bank's total assets stand at ₱1,850.3 billion while its equity is valued at ₱192.2 billion. It maintains a sufficient allowance for bad loans at 109%, with non-performing loans comfortably low at 1.6%. Trading at nearly 32% below its estimated fair value suggests potential undervaluation compared to peers and industry standards, making it an interesting prospect for those exploring under-the-radar opportunities in banking stocks.

- Navigate through the intricacies of China Banking with our comprehensive health report here.

Examine China Banking's past performance report to understand how it has performed in the past.

Sunstone Development (SHSE:603612)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Sunstone Development Co., Ltd. is involved in the research, development, production, and sale of prebaked anodes, lithium battery anode materials, and film capacitors both in China and internationally with a market capitalization of CN¥7.67 billion.

Operations: Sunstone's revenue is primarily derived from the sale of prebaked anodes, lithium battery anode materials, and film capacitors. The company's net profit margin has shown fluctuations over recent periods.

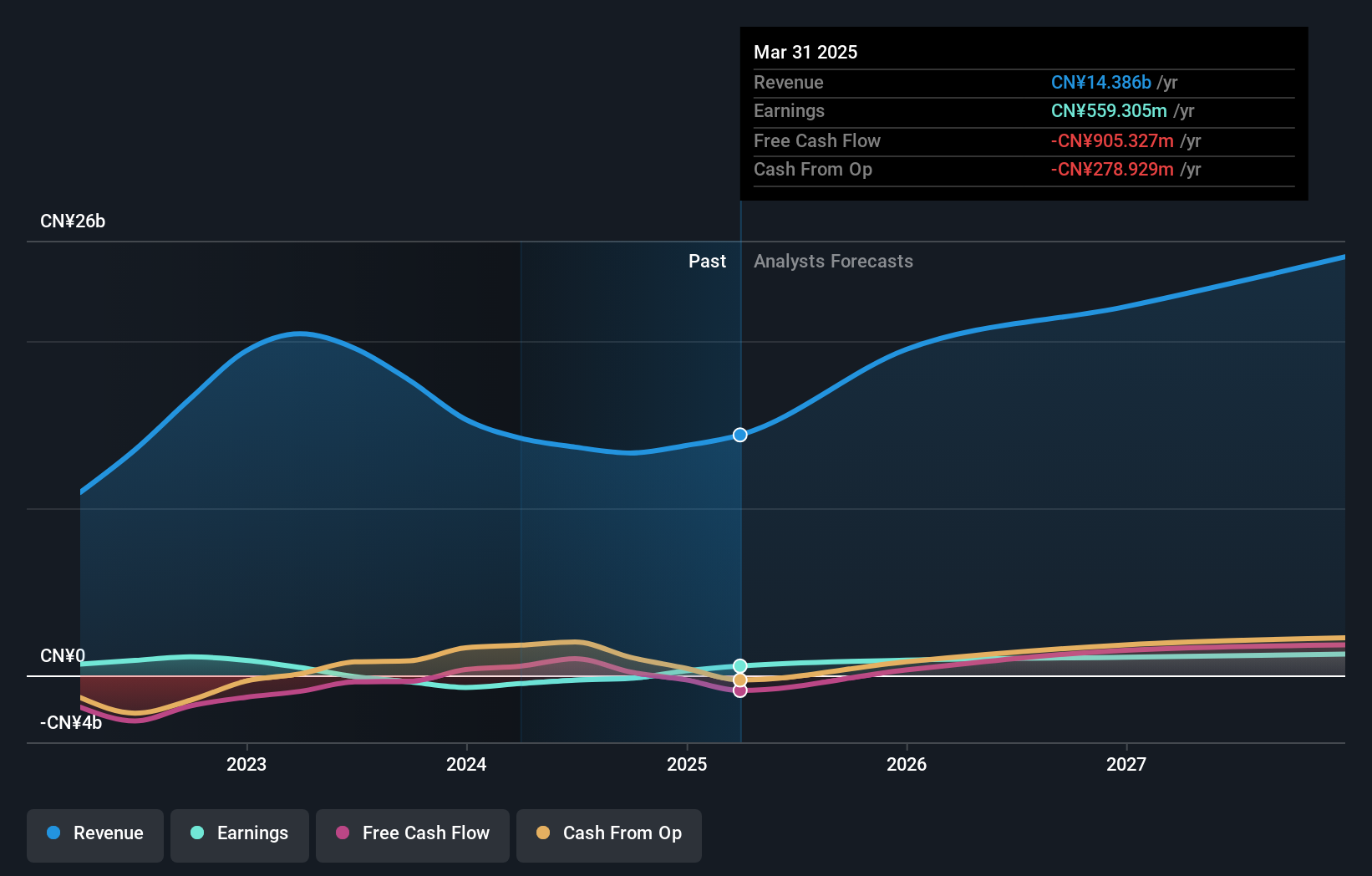

Sunstone Development, a notable player in the chemicals industry, has seen its earnings grow by 26.7% over the past year, surpassing the industry's 3.7% growth rate. Despite this positive trend, their debt to equity ratio has climbed from 86.6% to 131.3% over five years, indicating increased leverage and a net debt to equity ratio of 108.9%, which is high by typical standards. Their interest payments are well-covered with an EBIT coverage of 6.5 times; however, operating cash flow does not adequately cover their debt obligations currently making free cash flow negative despite trading at good value relative to peers and industry norms at present time.

- Click here to discover the nuances of Sunstone Development with our detailed analytical health report.

Assess Sunstone Development's past performance with our detailed historical performance reports.

Hokko Chemical Industry (TSE:4992)

Simply Wall St Value Rating: ★★★★★★

Overview: Hokko Chemical Industry Co., Ltd. operates in the manufacturing and sale of crop protection and fine chemicals products both in Japan and internationally, with a market capitalization of approximately ¥51.30 billion.

Operations: Hokko Chemical generates revenue primarily from the sale of crop protection and fine chemicals products. The company's financial performance is reflected in its market capitalization of approximately ¥51.30 billion.

Hokko Chemical Industry seems to be an intriguing player in the chemicals sector, with earnings growth of 16% over the past year, surpassing the industry's 11%. The company's debt-to-equity ratio has impressively shrunk from 8.7 to 1.8 over five years, indicating better financial management. Trading at a significant discount of 65% below estimated fair value suggests potential upside for investors. Hokko's recent announcement of a share repurchase program worth ¥2 billion aims to enhance shareholder returns and improve capital efficiency. With high-quality earnings and positive free cash flow, Hokko appears well-positioned for future growth prospects.

Summing It All Up

- Navigate through the entire inventory of 151 Global Undiscovered Gems With Strong Fundamentals here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com