- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Fastenal Stock Faces A Higher Bar As Tariffs Pressure Small Business Demand

Tariffs have shifted from headline politics to a real cost line for Main Street, and that ripple effect matters for your portfolio. Trump’s 2025 tariffs, higher input costs and rising small business pessimism are feeding into inflation pressures and uncertain demand. Some stocks tied closely to small business customers or imported goods now sit in the crosshairs of tighter margins and regulatory headaches. This article focuses on three stocks exposed to those tariff headwinds, all currently framed as potential negatives from the latest news, to help you evaluate which risks look acceptable and which might warrant extra caution before committing fresh capital.

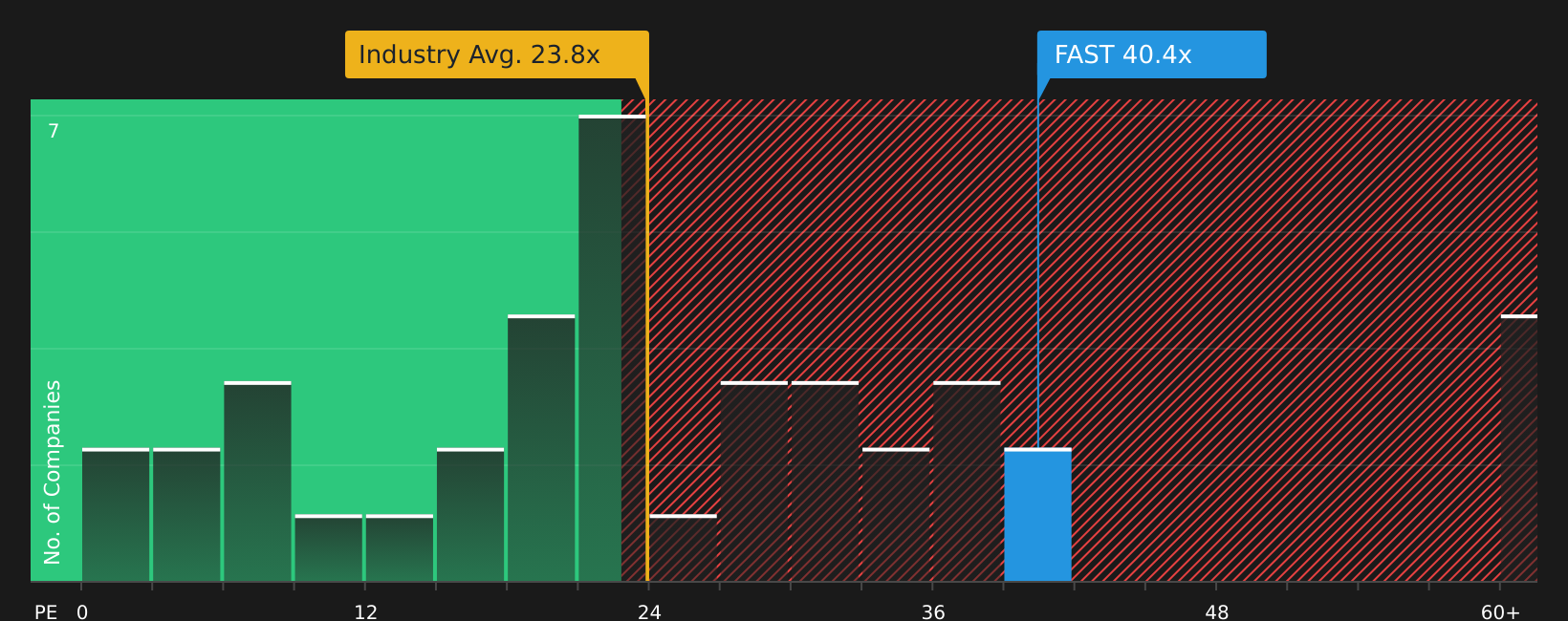

Fastenal (FAST)

Overview: Fastenal is a wholesale distributor of industrial and construction supplies, selling everything from bolts and screws to safety and maintenance products to manufacturers, contractors, and public sector customers across the US and overseas.

Operations: Fastenal generates about US$7.0b of its revenue from the United States, with additional contributions from Canada, Mexico, and other international markets.

Market Cap: US$53.3b

Investors looking at Fastenal may wish to weigh its high quality profile against growing tariff and valuation risks. The company serves many small manufacturers and contractors that are feeling the strain from Trump’s 2025 tariffs, and management has already discussed needing multiple pricing rounds to keep up with higher costs. This could test customer relationships and volumes. At the same time, Fastenal trades on a rich P/E multiple, and its dividend is not well covered by free cash flow, while the business leans on external funding. Strong returns on equity and solid governance keep Fastenal on the watchlist, but the combination of tariff driven margin pressure and an already full valuation creates a high bar for committing new capital.

Fastenal’s rich P/E, rising tariff costs and reliance on external funding suggest the story may be more fragile than it looks, so it is worth reading the 2 key rewards and 1 important warning sign

United Rentals (URI)

Overview: United Rentals is the largest equipment rental company in North America, supplying construction and industrial customers with everything from excavators and lifts to power, trench safety, storage and modular office solutions across the US and several international markets.

Operations: United Rentals generates about US$11.1b of revenue from its General Rentals segment and about US$5.3b from its Specialty segment.

Market Cap: US$68.6b

United Rentals is closely connected to small and mid sized contractors that are now dealing with higher equipment, parts and materials costs from Trump’s 2025 tariffs. The company itself faces fleet inflation and future parts price negotiations that could squeeze margins if higher costs are only partially passed through. Earnings quality is described as high, but profit margins have moved from 16.4% to 15.3%. The stock trades on a relatively high P/E compared with its 10.71% earnings and 7.1% revenue growth forecasts, and the combination of significant debt and persistent insider selling raises questions about how much optimism is already reflected in the share price. With analysts highlighting a bearish fair value that is well below the current share price, there is a risk that even solid execution may not be enough to support today’s expectations.

United Rentals’ optimism, rising fleet costs and tariff pressures may not fully line up with how much the stock already prices in. Before assuming the story holds, review the 1 key reward and 2 important warning signs

Intuit (INTU)

Overview: Intuit provides accounting, tax and marketing software that helps U.S. consumers and small businesses run their finances, from QuickBooks for bookkeeping and payroll to TurboTax for tax filing, Credit Karma for personal credit tools, and Mailchimp for customer campaigns.

Operations: Intuit generates about US$12.5b of reported revenue from Global Business Solutions, with segment adjustments of roughly US$8.5b, and most of its total revenue coming from the United States at about US$19.3b versus US$1.7b internationally.

Market Cap: US$75.2b

Intuit looks appealing on paper with strong profitability, high returns on equity and a P/E that sits well below many software peers. However, the tariff squeeze on U.S. small businesses, persistent worries about AI disruption to TurboTax and Mailchimp, and Credit Karma’s sensitivity to tighter credit conditions create more fragility than the headline quality suggests. Clients facing higher costs, heavier compliance workloads and a weaker customer base may push back on price rises or trim software seats just as Intuit leans into value based pricing and AI led services. In addition, mixed analyst sentiment, recent underperformance versus the U.S. software sector and reliance on external funding make Intuit a case where the business quality is clear, but the tariff driven pressure on its core customers could make that quality harder to fully rely on.

Intuit’s high quality story could be masking how tariff hit small businesses, AI pressure on TurboTax and Mailchimp, and Credit Karma’s credit sensitivity all fit together. Read the analysis report for Intuit

Take Control of Your Investment Journey

If United Rentals or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Opportunities Fly Past?

Fresh ideas move fast, and the best setups rarely stay quiet for long. Scan these themed shortlists before the next breakout gets caught by the crowd and consider your options.

- Review the 8 dividend fortresses to explore a curated set of high yield payers that may offer steadier income potential.

- Use the carefully filtered 32 robotics and automation stocks to look for early movers in automation and factory efficiency.

- Track the focused 34 power grid technology and infrastructure stocks to follow developments related to potential demand shifts in electrification.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com