- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

China Index Research Institute: Graduates' rental demand concentrated release. Average residential rents in 50 cities rose slightly month-on-month in June

The Zhitong Finance App learned that the China Index Research Institute released the ranking of the size of housing rental enterprises in China for June 2026. In June 2026, the average residential rent in 50 cities rose slightly month-on-month due to the concentrated release of mid-year leasing demand from mid-year graduates. According to the China Index 50 City Residential Rental Price Index, the average residential rent in the country's 50 cities was 33.97 yuan/square meter/month, up 0.08% month-on-month. In May, it fell 0.11% month-on-month; it fell 2.82% year on year, and the decline was 0.35 percentage points narrower than in May.

Judging from the opening scale list, according to statistics from the China Index Research Institute, in June 2026, the total number of properties opened by TOP30 centralized long-term rental apartment companies was 1.448,000. Specifically, the scale of local state-owned enterprises has maintained steady growth, and their share in the TOP30 has risen to 29%. The opening scale of “Comfort Inn” increased a lot this month, mainly due to the integration and integration of the “Indulgent Home” business. Judging from the management scale list, according to statistics from the China Index Research Institute, in June 2026, TOP30 centralized long-term rental apartment companies managed a total of 1.94 million units. This month, Wuhan Anju Group was newly added to the list.

Market operation

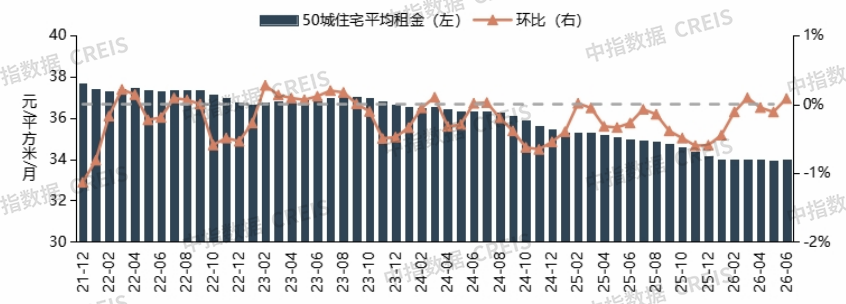

1. Overall rent: In June, the average residential rent in 50 cities rose 0.08% month-on-month and fell 2.82% year-on-year

In June 2026, the average residential rent in 50 cities rose slightly month-on-month due to the concentrated release of mid-year leasing demand from mid-year graduates. According to the China Index 50 City Residential Rental Price Index, the average residential rent in the country's 50 cities was 33.97 yuan/square meter/month, up 0.08% from month to month, down 0.11% in May; down 2.82% year on year, down 0.35 percentage points from May.

Figure: Average residential rent and month-on-month rise and fall in 50 cities from December 2021 to June 2026

Data source: China Index Data CREIS Rental Edition

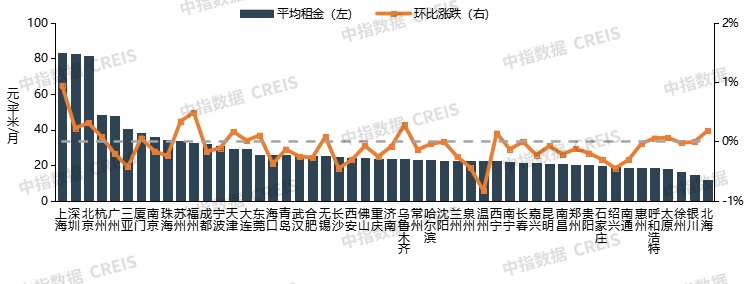

2. Rents in key cities: Increased rent increases in core cities such as Beijing, Shanghai, and Shenzhen

In June 2026, the number of cities where average residential rents rose month-on-month was 16, an increase of 5 over May. Specifically, Shanghai had the biggest month-on-month increase of 0.95%; Fuzhou, Suzhou, and Beijing rose between 0.3%-0.5%; six cities, including Urumqi and Shenzhen, rose between 0.1% and 0.3%; and six cities, including Wuxi and Hangzhou, rose within 0.1%. In June, the average residential rent in Changchun remained flat month-on-month, and the number increased by 1 compared to May.

In June 2026, the number of cities where average residential rents fell month-on-month was 33, 6 fewer than in May. Specifically, Wenzhou had the biggest month-on-month decline of 0.84%; 8 cities including Changsha and Shaoxing fell between 0.3% (inclusive) -0.5%; 16 cities including Hefei and Lanzhou fell between 0.1% and 0.3%; and 8 cities, including Jinan and Foshan, fell within 0.1%.

Figure: Average residential rent and month-on-month rise and fall in 50 cities in June 2026

Data source: China Index Data CREIS Rental Edition

Points of interest

Average residential rents in the 50 cities turned month-on-month in June, and the increase in northbound Shenzhen further expanded

Rental demand concentrated on the market during college graduation season in June, driving a marked increase in housing rental market activity in key cities, and owners' listing price expectations have also recovered. According to the China Index of Housing Rental Prices in 50 Cities, the average residential rent in the 50 cities stopped falling and turned up in June after two consecutive months of slight adjustments, with an increase of 0.08%. After price adjustments over the past few years, the bottom rent support in key cities has gradually been consolidated, and market recovery flexibility has increased.

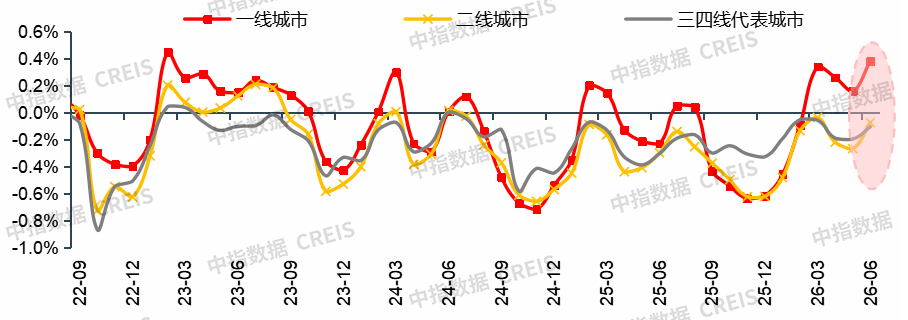

Looking at each echelon, residential rents in all tier cities showed positive month-on-month performance in June. According to monitoring by the Central Index Institute, in June, the average rent for ordinary housing in first-tier cities continued the repair trend, increasing by 0.22 percentage points to 0.38% over the previous month. Although the average rent ratio of second-tier and third-tier and fourth-tier representative cities was still adjusted, the adjustment was narrower than in May; among them, the average residential rent decline in second-tier cities narrowed 0.2 percentage points to 0.07% month-on-month, while those representing third- and fourth-tier cities narrowed 0.1 percentage points to 0.10%.

Figure: The trend of monthly month-on-month rise and fall in average residential rents in each tier of cities

Data source: Middle Index Data CREIS

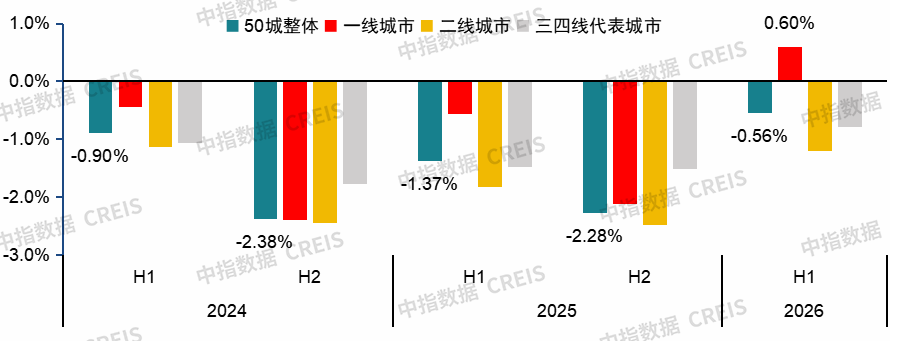

Looking at the cumulative increase and decrease in rents in each tier of cities during the year, first-tier cities showed the most obvious signs of restoration. According to the 50-city residential rental price index, in the first half of 2026, the average rent in first-tier cities rose slightly by 0.60%, ending the previous two consecutive years of adjustment. Average residential rents in second-tier and third-tier and fourth-tier cities fell by a cumulative total of 1.20% and 0.79%, respectively. The declines were all more than 0.6 percentage points narrower than the same period last year. Key cities, especially first-tier cities, are gradually showing a trend of bottoming out residential rents.

Figure: Comparison between the cumulative rise and fall in the 50 cities as a whole and the average residential rents in each tier of cities

Data source: Middle Index Data CREIS

July is a critical window for concentrated release of rental demand during the graduation season. The large-scale entry of graduates into the market will become the core driving force supporting rents in key cities, and the rent repair trend in key cities is expected to strengthen. Among them, cities with concentrated industries and outstanding population absorption capacity, such as Beijing, Shanghai, Shenzhen, Tianjin, and Hangzhou, will take on a large number of recent job search and rental needs, and rents are expected to continue to rise moderately.

2.In June, there were many breakthroughs in the REITs market in the rental housing sector, and the industry's multi-level securitization system accelerated

In the first half of the year, key progress was made in the securitization of market-based long-term rental apartment assets. In terms of public REITs, Cathay Pacific Haitong China Construction Rental Housing REIT has received feedback from the Shanghai Stock Exchange. Its underlying assets are long-term rental apartments operated on a pure market-based basis. If successfully implemented, it will become the first simple market-based public rental housing REIT in the entire market.

At the same time, inter-agency REITs are also entering the market at an accelerated pace. In June, the CICC-Borin Interagency REITs were successfully issued, making it the first market-based long-term rental housing interagency REIT in the country and opening up a new exit path for pure market-based projects. At the same time, REITs-like products ushered in innovation and implementation. In June, Cathay Pacific Haitong-Pukai Group's Huizhi Rental REIT was launched on the Shanghai Stock Exchange, with a product scale of 3.65 billion yuan. This is the first green guaranteed housing REIT in the country, and it is also the largest REIT project in Shanghai so far.

As the exit channels for housing rental assets continue to expand, the current industry has gradually formed a full-life cycle securitization system covering “pre-REITs, like REITs, inter-agency REITs, and public REITs”, which can be adapted to long-term rental projects with different asset sizes and different income characteristics to meet the differentiated allocation needs of various types of institutional investors.