- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

McDonalds Stock And Other Consumer Names Facing Inflation Pressure

Stubborn US inflation, fragile consumer sentiment, and questions around how price pressures are even measured are putting a spotlight on stocks most exposed to household budgets. With May CPI at 4.2% and PCE at 3.4%, many consumers still feel worse off than official data suggests, and that gap in perception can matter just as much as the numbers. This article breaks down 3 stocks from our Consumer Sentiment and Inflation Pressure Stocks to Watch screener that appear more at risk from strained wallets, helping you evaluate where inflation sensitive exposure may deserve extra caution.

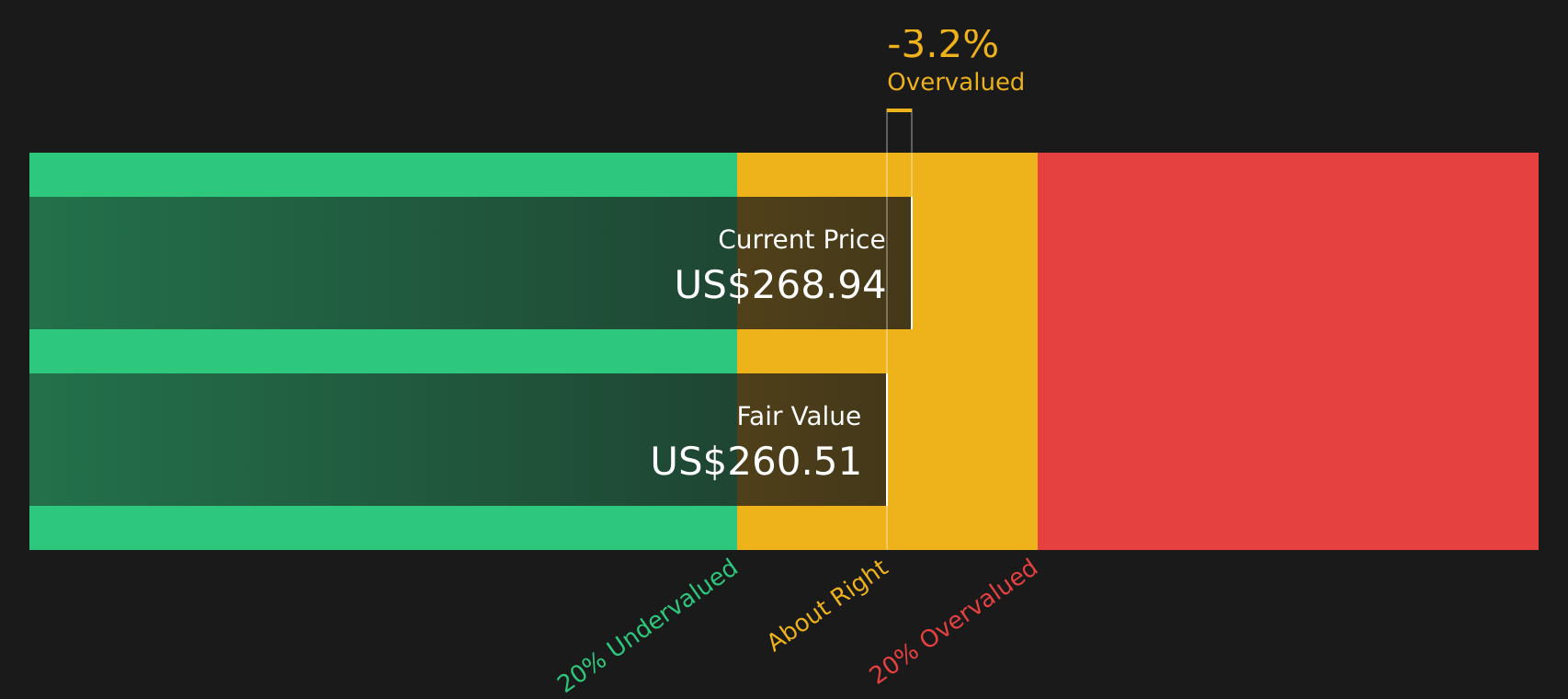

McDonald's (MCD)

Overview: McDonald's is a global fast food company that operates and franchises McDonald’s branded restaurants, serving burgers, chicken, fries, breakfast items, desserts, and beverages across the U.S. and international markets through a mix of company owned and franchise structures.

Operations: McDonald's generates most of its revenue from International Operated Markets at about US$14.0b, followed by the U.S. at roughly US$10.9b and around US$2.5b from International Developmental Licensed Markets & Corporate.

Market Cap: US$195.1b

McDonald's sits at the center of today’s inflation squeeze, leaning on value hungry customers just as real incomes for lower and middle income households are under strain and traffic pressures show up in industry data. Earnings and dividends appear dependable on paper, but the high debt load, heavy reliance on franchised operators coping with their own cost inflation, and a valuation that some detailed models suggest is rich leave limited room for disappointment if consumer sentiment weakens further. Management is focusing on Every Day Affordable Price menus and new beverage concepts to maintain visit levels, yet that may primarily defend market share rather than create significant growth. A key consideration for investors is how much risk may be overlooked in what many treat as a comfort stock.

McDonald's dependable image may be masking how much hinges on franchise resilience, debt and a full valuation if inflation keeps biting into traffic. Get the full picture with the 6 key rewards and 1 important warning sign

Target (TGT)

Overview: Target is a U.S. general merchandise retailer that sells a broad mix of apparel, beauty, household essentials, food, electronics, and home goods through its stores and digital channels, including Target.com, often supported by owned brands and periodic design partnerships.

Operations: Target generates all of its approximately US$106.4b in revenue from U.S. retail operations.

Market Cap: US$61.4b

Target sits in the middle of weak consumer sentiment and persistent inflation, with management flagging sustained pressure on discretionary categories and unit demand across the industry. Earnings recently declined and margins compressed to 3.2%. High debt, heavy competition from Walmart and Amazon, and continued investment needs in digital, supply chain and store remodels all put profitability under pressure if spending stays soft. At the same time, investors may focus on a 3.38% dividend, forecasts for improving return on equity, and growth in higher margin businesses such as retail media and marketplace fees. A key consideration is whether Target’s reset and assortment refresh can outpace pressure on consumer wallets before higher leverage and softer demand further affect returns.

Target’s margin reset, rising leverage and softer discretionary demand may be masking deeper pressure on future returns, and some investors might be missing how the full risk picture fits together, including the 4 key rewards and 2 important warning signs

Procter & Gamble (PG)

Overview: Procter & Gamble is a global consumer products company that sells everyday essentials such as detergents, diapers, razors, toothpaste, skincare and household cleaners under brands like Tide, Pampers, Gillette, Oral B, Olay and Febreze.

Operations: Procter & Gamble generates most of its revenue from Fabric & Home Care at about US$30.3b, followed by Baby, Feminine & Family Care at roughly US$20.4b, Beauty at about US$15.8b, Health Care at around US$12.4b, Grooming at roughly US$6.9b and about US$0.9b from Corporate activities.

Market Cap: US$342.4b

Procter & Gamble appears to be a relatively stable option at first glance, with a wide moat, high ROE and a dividend that has risen for 70 years. However, elevated inflation and weak sentiment increase the risk that shoppers continue trading down to cheaper brands. At the same time, tariffs, commodity costs and heavier promotion may erode margins. Management has already highlighted a volatile backdrop and is cutting up to 7,000 non manufacturing roles. The company also faces ongoing tariff and private label pressure. Forecasts indicate mid single digit earnings and revenue growth relative to the broader US market. For investors, a key consideration is whether paying a premium for perceived safety in Procter & Gamble could overlook the strain its premium brands might face if household budgets remain tight.

Procter & Gamble’s premium brands and rich safety premium may be masking how fragile loyalty becomes when budgets stay tight. Before assuming the moat holds, review the 3 key rewards and 1 important warning sign

Take Control of Your Investment Journey

If Procter & Gamble or any of these companies are making you feel more cautious, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Catch On?

Fresh opportunities rarely stay quiet for long. Spot potential breakouts and momentum shifts while they still fly under the radar. Before the crowd catches up, consider acting sooner rather than later.

- Capture potential turnaround stories by scanning curated companies on the 20 high quality undiscovered gems that still sit under the radar before momentum fully builds.

- Target dependable cash generators by running the list of solid balance sheet and fundamentals (47 results) so you focus on businesses with sturdier finances when it matters most.

- Ride longer-term infrastructure themes by screening the 34 power grid technology and infrastructure stocks and spot companies positioned around grid upgrades before attention fully shifts their way.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com